As a Canadian business owner, you understand the importance of managing your finances effectively, especially when it comes to cross-border transactions. Navigating the complexities of foreign exchange (FX) conversion can be a daunting task, but with the right strategies and tools, you can save money and optimize your financial operations.

In this article, we’ll dive into the world of FX conversion, focusing specifically on how to save on conversions between Canadian dollars (CAD) and United States dollars (USD). By the end of this guide, you’ll be equipped with the knowledge and strategies to make informed decisions and minimize costs associated with currency exchange.

What is FX Conversion?

FX conversion is the process of exchanging one currency for another, such as Canadian dollars (CAD) to United States dollars (USD). Understanding the foreign exchange process is crucial for businesses engaging in cross-border transactions.

How to Save on FX Conversion Between CAD and USD

Explore strategies to minimize costs: Researching and implementing effective strategies can significantly reduce the financial impact of currency exchange on your business.

Optimize transactions: By optimizing your cross-border transactions, you can minimize fees and maximize savings.

1. Understand Currency Conversion Fees

Familiarize yourself with typical fees: Banks and brokers often charge various fees for currency conversion. Understanding these fees is the first step in saving money.

Compare providers: By comparing different providers, you can identify those that offer the most competitive rates and save on conversion fees.

2. Seek Competitive Exchange Rates

Monitor the market: Keeping a close eye on exchange rates can help you identify favorable times to convert your currency.

Utilize rate comparison platforms: Platforms that offer real-time rate comparisons can help you find the best deals and save money on conversions.

3. Use Norbert’s Gambit for Large Transactions

Implement Norbert’s Gambit: This strategy involves buying dual-listed stocks to transfer between CAD and USD, effectively minimizing conversion costs.

Understand the steps: To execute Norbert’s Gambit effectively, it’s essential to familiarize yourself with the process and follow the steps carefully.

4. Consider a Corporate Card for USD Transactions

Use a corporate card for USD: A corporate card for USD transactions can help minimize conversion fees for business expenses.

Benefits of a specialized corporate card: Corporate cards designed for cross-border transactions often offer competitive rates and additional features to streamline your financial operations.

Tips on Reducing FX Costs

1. Plan Transactions Strategically

Timing is crucial: By planning your conversions when exchange rates are favorable, you can maximize savings and minimize costs.

2. Utilize Financial Tools

Leverage financial software: Specialized financial software can help you track and optimize your currency exchanges, ensuring you’re always getting the best rates.

Frequently Asked Questions

What is the cheapest way to convert CAD to USD?

Use cost-effective methods: Strategies like Norbert’s Gambit or platforms with low conversion fees can be the most cost-effective ways to convert CAD to USD.

How can I avoid high fees when converting currency?

Compare and use specific strategies: Comparing providers and using strategies like Norbert’s Gambit for large sums can help you avoid high conversion fees.

What are the best strategies for saving on FX conversion?

Monitor, use corporate cards, and apply Norbert’s Gambit: By monitoring exchange rates, using corporate cards designed for cross-border transactions, and applying Norbert’s Gambit when appropriate, you can effectively save on FX conversion.

How does Norbert’s Gambit work for CAD to USD conversion?

Buy dual-listed stocks and journal them: Norbert’s Gambit involves buying dual-listed stocks and journaling them to exchange currencies at minimal cost.

Conclusion

By implementing these strategies and staying informed about the latest trends in FX conversion, you can significantly reduce costs and optimize your cross-border transactions. At Float, we understand the unique challenges faced by Canadian businesses, and we’re here to help you navigate the complexities of foreign exchange. Get started for free today and discover how our innovative solutions can help you save on FX conversion between CAD and USD.

Electronic payments have become commonplace in modern business transactions, but it can be tough to figure out which method is best. Are you wondering about ACH vs EFT? What about wire transfers? And does it even matter?

Spoiler: Oh, it matters.

Your chosen payment method can impact every area of your accounts payable process: cash flow, transaction costs and operational efficiency. What does the right choice mean for you? You can confidently pay your employees on time, suppliers receive what’s owed and customers experience seamless transactions.

Since growing businesses need reliable online payment options, most have embraced some form of EFT payment. Just over 60% of Canadian businesses surveyed accept EFTs.

Let’s take a closer look at the options available. In the past, payment options for Canadian businesses were relatively straightforward: Electronic Funds Transfers (EFTs) for domestic transactions, Automated Clearing House (ACH) payments for U.S. transactions, and wire transfers for cross-border payments.

However, with the rise of modern financial providers, some Canadian businesses now have more flexibility, including the ability to send ACH payments depending on their bank or payment provider. You may have heard of Wise, a payment platform handling online payment processing in the U.S. Now Canadians can also explore a variety of options to streamline their accounts payable processes.

In this guide, we’ll review your options to help you understand these payment methods and determine what’s best for your business.

What is an EFT payment?

Electronic Funds Transfer (EFT) is a broad term that covers all digital payments that move money from one bank account to another. Traditionally, EFT was the standard for Canadian businesses, used for payroll, vendor payments and online bill payments.

While this remains true, some modern financial providers now allow businesses to send payments across borders using EFT-like methods, making it essential to check with your financial institution to understand your options. It may be time to weigh EFT vs ACH to see how the comparison checks out.

Unlike traditional cheques or cash transactions, EFTs leverage digital networks to facilitate transfers quickly and securely. Depending on the payment type (see common types below), processing times for EFT payments can range from one to four business days.

Online payments have been trending upward, with EFT payment values in Canada growing 40% in the past five years. EFTs are widely used across Canada, enabling businesses to send and receive payments without visiting a physical branch or filling out paperwork like it’s 1925.

It makes sense. Most of us aren’t carrying around a lot of cash, because we find it faster, easier and more secure to pay online for everything from coffee to home renos. Online payments help your business do the same thing.

So, what is an EFT payment exactly?

Common types of EFT payments include:

Direct deposits: Used for payroll processing and vendor payments.

Debit card transactions: Funds are withdrawn electronically at the point of sale.

ACH payments: Cross-border transactions that use a batch processing system with predictable timing.

Wire transfers: Typically used for large payments (both domestic and international wire transfers).

Online bill payments: Automated payments for utilities, leases and subscriptions.

Interac e-transfer: Commonly used for quick peer-to-peer and business transactions.

EFTs provide a secure way to manage cash flow with automation options that reduce administrative overhead—and ease frustration. Since transactions occur electronically, there is also a lower risk of errors and fraud compared to traditional paper-based payments.

Verify recipient details Always double-check recipient information, including bank account numbers and names, to prevent payment errors and delays.

Use secure banking platforms Ensure you use a secure banking portal or trusted payment provider to minimize fraud risks.

Schedule payments in advance Set up EFT payments ahead of time to ensure timely processing and avoid unexpected delays.

What is an ACH payment?

Automated Clearing House payments, or ACH payments, are a specific type of EFT that processes transactions in batches through an Automated Clearing House payment network. Unlike other types of EFTs that process transactions individually, ACH transactions are grouped together and processed at set intervals throughout the day.

Historically, ACH was exclusive to the U.S., with Canadian businesses relying on EFT for domestic transactions. However, some modern financial providers (like Float) now offer ACH payment capabilities for Canadian businesses, enabling cross-border payments without relying solely on wire transfers.

If your bank or payment provider supports ACH, it could be a cost-effective way to send funds to U.S. businesses. For Canadian SMBs with a U.S. entity, this is good news.

So, a smart first step is an exploratory check-in with your financial institution and alternative providers to evaluate the options available.

What is an ACH payment’s key benefit?

ACH payments get a gold star for cost-effectiveness. Since they are processed in bulk, businesses can reduce transaction fees compared to wire transfers or credit card payments. ACH transactions are also reliable and predictable, making them ideal for regular payments where timing consistency is crucial (e.g. anything that makes payroll easier is a big win-win).

However, because ACH payments process in batches, they may take longer than individual EFT transactions. Timeframes can vary, but most ACH payments are completed within one to three business days, with some financial institutions offering expedited processing options. This means ACH is best suited for payments that do not require immediate settlement but benefit from lower costs.

Best practices for using ACH payments

Here are a few tips to keep in mind when sending ACH payments.

Ensure proper authorization

Obtain written or electronic authorization from payees before initiating ACH payments to comply with banking regulations.

Monitor transactions regularly

Keep an eye on ACH payments to quickly identify and address any errors or failed transactions.

What is a wire transfer?

A wire transfer is a fast and secure method of electronically transferring funds between financial institutions, both domestically and internationally. Unlike ACH and EFT payments, wire transfers are processed in real time, ensuring that funds are available to the recipient the same day they are sent.

In Canada, domestic wire transfers are processed through Lynx, the country’s electronic wire payment system.

When are wire transfers used?

Wire transfers are commonly used for high-value transactions, urgent payments or cross-border transfers where real-time settlement is required. Businesses often choose wire transfers for:

Large supplier or vendor payments that require immediate clearing

International transactions where ACH or EFT is not an option

Time-sensitive financial obligations

What you should know about wire transfers

Once sent, wire transfers cannot be reversed. However, while wire transfers offer the advantage of speed and certainty, they also tend to be more expensive than other payment methods. Fees can vary widely between banks, and are often much steeper per transaction than other options, with additional costs for currency conversion if sending funds internationally.

To avoid delays, businesses must ensure that recipient details, including banking information and currency specifications, are accurate before initiating a transfer.

ACH vs EFT vs wire transfers: Understanding your payment options

While both EFT and ACH payments offer efficiency and security, the differences in cost, processing time and transaction flexibility can significantly impact your financial workflow. Understanding these differences is one key accounts payable strategy that can help you manage your financial workflow.

Below, we break down each method’s advantages and drawbacks to help you decide which is best, whether you need to manage payroll or pay a U.S. invoice.

As outlined, traditionally, Canadian businesses have used EFT for domestic transactions, while ACH was reserved for U.S. bank transfers. Wire transfers were the primary solution for cross-border payments. However, newer financial providers now offer Canadian businesses access to ACH payments, meaning the landscape is evolving.

Step 1: Check what your financial institution offers

Before deciding between EFT and ACH, the first step is understanding what’s available to you. Not all banks in Canada offer ACH payments, meaning your options may be determined by your financial provider.

If your bank only supports EFT: You’ll use EFT for domestic payments and wire transfers for cross-border transactions.

If your bank or payment provider supports ACH: You may have the ability to use ACH for payments to U.S. businesses, potentially reducing costs compared to traditional wire transfers.

If neither option is available: You may want to explore modern financial providers that enable cross-border ACH or EFT payments as an alternative to expensive wire transfers.

Step 2: Compare costs and processing times

Once you know your available options, compare fees (we’ve got an international money transfer calculator for that!), speed and transaction processes to determine the best method for your business needs.

EFT: Best for Canadian transactions, typically low-cost, with convenient processing times.

ACH: A cost-effective option for paying U.S. vendors, but processing times can vary depending on batch processing schedules.

Wire Transfers: Typically the fastest cross-border option but comes with much higher fees.

Step 3: Consider a modern payment provider

If your current bank doesn’t offer ACH, but you want to explore alternatives, newer financial providers offer ACH and EFT options beyond traditional banking. These providers may offer lower fees than wire transfers, but it’s important to check for additional costs, including currency exchange fees.

By following these steps, you can determine whether you should continue using EFT, explore ACH, or seek modern payment solutions that align with your business needs.

Learn more with Float: Modern business expense management and corporate cards

While EFT, ACH and wire transfers each still serve specific roles, the online payment landscape in Canada is evolving. Many businesses still rely on traditional EFT payments made through their AP software or directly with a bank, but those working with alternate payment providers such as Float may have access to ACH for U.S. transactions, offering a potentially more affordable alternative to wire transfers.

Both EFT and ACH payments provide businesses with efficient ways to send and receive money, but their differences make them suitable for different use cases. EFT may be the better option if speed and versatility are your priority. However, if cost savings and predictable recurring payments are more important, ACH is likely the best fit.

Understanding the options available and the key differences between them allows business owners to make informed decisions that optimize cash flow, reduce transaction costs and improve financial management.

Make EFT Payments with Float

Canada’s best-in-class EFT, ACH, and Global Wires payments platform — plus average savings of 7%.

Managing business expenses can quickly become chaotic without the right systems. From vendor invoices to employee reimbursements, keeping track of payments is a critical part of maintaining healthy cash flow.

This is where accounts payable (AP) comes in—the core of your company’s financial operations. But traditional AP processes are often slow, error-prone and a major headache for finance teams. So, how can you streamline your AP process and free up time for what really matters?

In this guide, we’ll break down everything you need to know about accounts payable: what it is, how it works and how modern automation tools like Float can transform your AP workflow. Whether you’re a finance leader aiming to eliminate gruntwork or a business owner seeking better visibility into company spending, we’ve got you covered.

What is Accounts Payable (AP)?

Accounts payable (AP) refers to the money a company owes to its vendors for goods or services received but not yet paid for. It’s recorded as a liability on the balance sheet and includes payments such as supplier invoices, contractor fees and utility bills.

Examples of accounts payable:

Invoices for supplies and equipment (e.g. office supplies, computer hardware, raw materials, etc.)

The way your business manages accounts payable can make or break its cash flow, vendor relationships and bottom line. In fact, 65% of SMBs report long processing times for financial transactions, which ties directly to cash flow problems and missed opportunities for growth.

Imagine a missed invoice leads to a late fee and a frustrated vendor who pauses your deliveries. Or maybe your finance team is scrambling to fix a double payment, wasting hours chasing down refunds. Meanwhile, slow approvals stall an important purchase, putting a critical project on hold. There are just a few ways inefficient AP processes can cost you time, money and trust.

Accounts payable vs. accounts receivable

While accounts payable tracks what your business owes, accounts receivable (AR) tracks what others owe you. AP is a liability, whereas AR is an asset. Both are important for understanding cash flow and maintaining financial stability.ment fees.

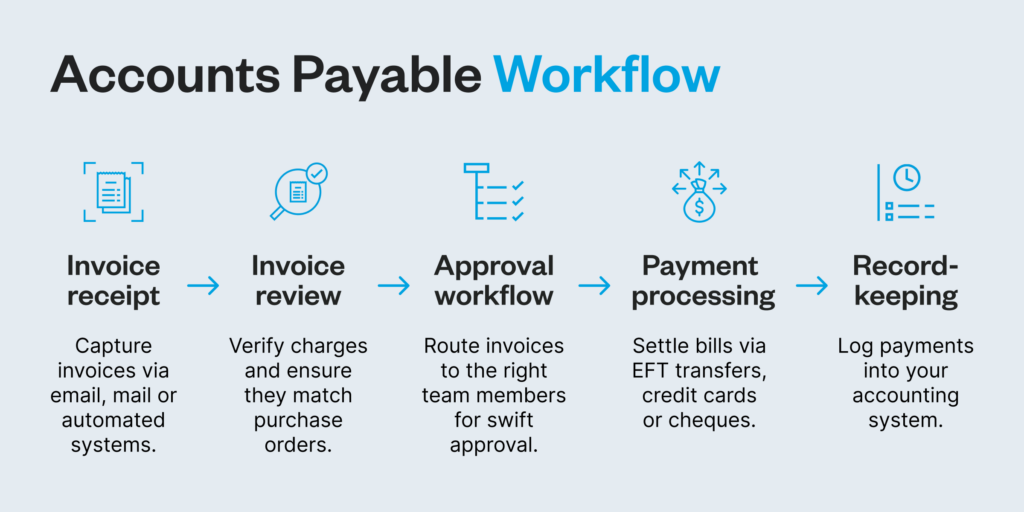

What is the accounts payable process?

Accounts payable management involves outlining the journey from invoice to payment, offering a clear framework for how to pay an invoice efficiently and accurately.

Here’s how it typically flows:

Invoice receipt: Capture invoices via email, mail or automated systems.

Invoice review: Verify charges and ensure they match purchase orders.

Approval workflow: Route invoices to the right team members for swift approval.

Payment processing: Settle bills via EFT transfers, credit cards, or cheques.

Record-keeping: Log payments into your accounting system.

When your AP process runs smoothly, payments are on time, vendors stay happy and your cash flow stays clear.

6 common challenges in traditional AP management

Traditional accounts payable processes can feel like a time sink—slowing operations, frustrating finance teams, and leaving room for costly mistakes. Without modern tools, businesses face a range of issues that can quickly snowball into bigger problems.

1. Manual workflows

First, there’s the chaos of manual workflows. Paper invoices, spreadsheets and email chains create confusion, waste time and make it easy for documents to slip through the cracks. Finance teams end up chasing receipts instead of focusing on strategic work.

2. Approval bottlenecks

Then come the approval bottlenecks. Payments stall when they’re stuck in endless sign-off loops. The longer the delay, the greater the risk of late fees—or worse, strained vendor relationships.

3. Frequent errors

On top of that, errors run rampant with manual processes. It’s easy to enter the wrong numbers, pay the same invoice twice or miss a payment altogether.

4. Poor visibility

There’s also the issue of poor visibility into spending. Without a centralized view, finance teams are left in the dark, scrambling to piece together where money is going and struggling to catch unwanted expenses in real time.

5. Decentralized tools

Compounding these problems is that many businesses still rely on disconnected tools to manage the AP process—55% of SMBs say financial tools that don’t integrate well with each other are a top inefficiency driver. Often, this looks like using one system for bill intake, another for approvals, an accounting platform to track unpaid bills and a separate bank portal to process payments.

When integrations between tools break, it causes delays and wastes time on troubleshooting. Even if you’re processing high volumes of payments every month, this patchwork approach can waste time rather than save it.

6. Fraud

What’s worse, all of these challenges compound to increase your fraud risk. Loose controls and outdated systems can leave the door open for unauthorized payments or fake invoices to slip through unnoticed, costing your business money and damaging trust.

When these challenges pile up, they can have real-world consequences. But with a modern, automated accounts payable process, you can gain the visibility and control you need to make payments simpler.

Benefits of automating accounts payable management

From speeding up payments to improving visibility, accounting automation helps your business move faster, smarter, and more securely.

Here’s how:

Faster invoice processing Manual invoice processing is slow and clunky, often dragging payments out for days or even weeks. Automation can capture invoice data instantly and route approvals with a click. Payments that once took days can be completed in minutes, keeping your vendors happy and your operations running smoothly.

Reduced errors and fraud risk Manual data entry is a breeding ground for costly mistakes: duplicate payments, missed invoices and misfiled records. Automated accounts payable systems use built-in validations to catch errors before they happen, reducing the risk of costly slip-ups. With proper controls and approval workflows in place, you’ll minimize the chance of fraudulent activity or unauthorized spending.

Improved cash flow management With automation, you get real-time insights into every outgoing payment—what’s due, what’s paid and what’s pending. Clear visibility into your liabilities helps you forecast expenses, avoid late fees and take advantage of early payment discounts.

Increased visibility and control No more chasing down receipts or wondering where an invoice stands. Automation centralizes your AP data into one dashboard, giving you a complete, real-time view of every transaction. You can track approvals, spot spending patterns and enforce policies, all without digging through email threads or spreadsheets.

Modern accounts payable strategies

Focus on these accounts payable strategies to reduce delays, eliminate errors, and gain better control over your AP processes.

1. Automate invoice processing

Manual data entry is a productivity killer that leads to errors and slows down your entire AP workflow. Automating invoice processing is one of the fastest ways to make your AP process more efficient and accurate.

Here’s how to do it right:

Digitize invoices with OCR technology. Optical character recognition (OCR) technology scans and converts paper invoices into digital records. This eliminates manual data entry, reduces errors, and speeds up processing—especially if you’re dealing with high volumes of invoices.

Automate invoice-to-PO matching. Set up rules to automatically match invoices to purchase orders (POs). With automated matching, any discrepancies like price differences or unexpected charges are flagged for review. This helps catch errors early and prevents overpayments.

Schedule recurring payments. For vendors with regular billing cycles, such as utilities or monthly service providers, automate recurring payments. This ensures that predictable bills are paid on time without the risk of missed deadlines or late fees.

2. Optimize approval workflows

Bottlenecks in the approval process slow down payments, frustrate vendors, and create unnecessary delays. Streamlining your approval workflows keeps payments moving and eliminates confusion.

Here’s how to do it:

Establish clear approval hierarchies. Define who needs to approve invoices based on payment amounts, vendor types, or departments. With clear guidelines, everyone knows their role, and invoices don’t get stuck waiting for the right sign-off.

Set spending limits for team members. Create thresholds for automatic approvals to reduce unnecessary reviews. For example, purchases under $250 can be pre-approved, while anything above requires manager review. This keeps small expenses moving without bottlenecks.

Route approvals digitally. Use an automated system to assign invoices to the right approvers, notify them instantly, and track every step of the process. Real-time updates and digital records eliminate back-and-forth emails and make it easy to follow the status of each invoice.

3. Transition to electronic payments

Paper cheques are slow, costly and prone to error. Switching to electronic payment methods speeds up your accounts payable process and reduces administrative headaches.

Here’s how to make the shift:

Prioritize virtual cards for all online payments. Virtual cards are single-use or limited-use payment numbers tied to your corporate account. They’re easy to track, help prevent fraud and are perfect for one-off payments or online purchases (especially software trials). Many vendors prefer virtual cards because they process instantly and don’t require banking details.

Use electronic transfers for domestic payments. For all other domestic transactions,EFT (Electronic Funds Transfer) payments are faster, more secure and often cheaper than traditional cheques in Canada. An EFT payment is ideal for recurring payments and bulk transfers, cutting out mailing delays and lowering processing costs.

💡 Pro tip: Understand the difference between ACH vs EFT. Automated clearing house payment (ACH) is a specific type of EFT used primarily for domestic payments within the US. Some more modern providers do offer cross-border ACH payments, but you’ll need to check with your bank. Or, try making international payments with Float.

New to digital payments? Start by learning how to make an EFT payment, from setting up vendors to scheduling transfers.

Looking to pay invoices from Canada to other countries?

While this may seem overwhelming at first, modern tools have come a long way. Solutions (like Float) will allow you to implement all of these strategies in one place.

Accounts Payable Metrics to Track

Days Payable Outstanding (DPO): measures the average time it takes to pay vendors

Invoice processing time: tracks the efficiency of the AP process from invoice receipt to payment

Early payment discount capture rate: shows the percentage of available discounts captured

Electronic invoice adoption rate: indicates the level of automation in the AP process

Vendor satisfaction score: assesses the strength of vendor relationships based on timely payments and communication

Tips for choosing the right accounts payable software

Start with automation. Capabilities like invoice capture and approval workflows will save your team time and reduce errors. Look for features like OCR technology to digitize invoices and automatic matching to purchase orders to streamline your process.

Next, prioritize integration. Your software should connect seamlessly with your accounting system, keeping your records accurate without extra manual work.

Visibility matters, too. Real-time dashboards and easy-to-read reports help you track spending, catch errors and make smarter financial decisions.

Don’t forget security. Built-in safeguards like multi-factor authentication and role-based permissions protect your payments from fraud and unauthorized access.

Last, choose software that grows with you. Look for a solution that can handle increasing transaction volumes, add users easily and adapt to your changing needs, all while offering responsive support.

Why Float fits the bill

Float offers fast automation, real-time insights and secure, seamless integrations—everything you need to manage your accounts payable process without the headaches. With built-in tools like bill pay to automate invoice payments, you can process transactions faster and reduce manual work. Plus, it’s built to scale with your business, supporting your growth every step of the way.

Simplify business spending with Float’s smart AP & corporate cards

“Float’s Bill Pay has become our main AP solution for Canadian business expenses. They built a product that is better than anything else on the market in Canada.”

Thomas Kwon Head of Finance & Operations

Accounts payable management doesn’t have to be complicated or costly. Float brings everything you need into one easy-to-use platform, helping you automate your AP workflows, track spending in real time, and process payments faster—all while keeping complete control over your finances.

With Float, you get a smarter way to manage every dollar your business spends.

Issue corporate cards instantly

Automate bill payments from one place

Close your books up to 8x faster with seamless accounting integrations

Earn 4% interest on your Float balance

Get 1% cashback on card spend

Float is trusted by thousands of Canadian businesses to simplify their spending, from approvals to payments—all with no hidden fees and fast, friendly support when you need it. Whether you’re eliminating approval bottlenecks or gaining better control over your cash flow, Float helps your business spend smarter and scale faster.

Ready to take control of your business spending?

Get started with Float today and experience faster payments, fewer errors, and complete visibility.

Float is Canada’s Only All-in-one AP Solution

Automate bill intake, approvals, accounting sync, and pay anyone in the world with Float’s Bill Pay — plus unlock 7% savings on your spend.

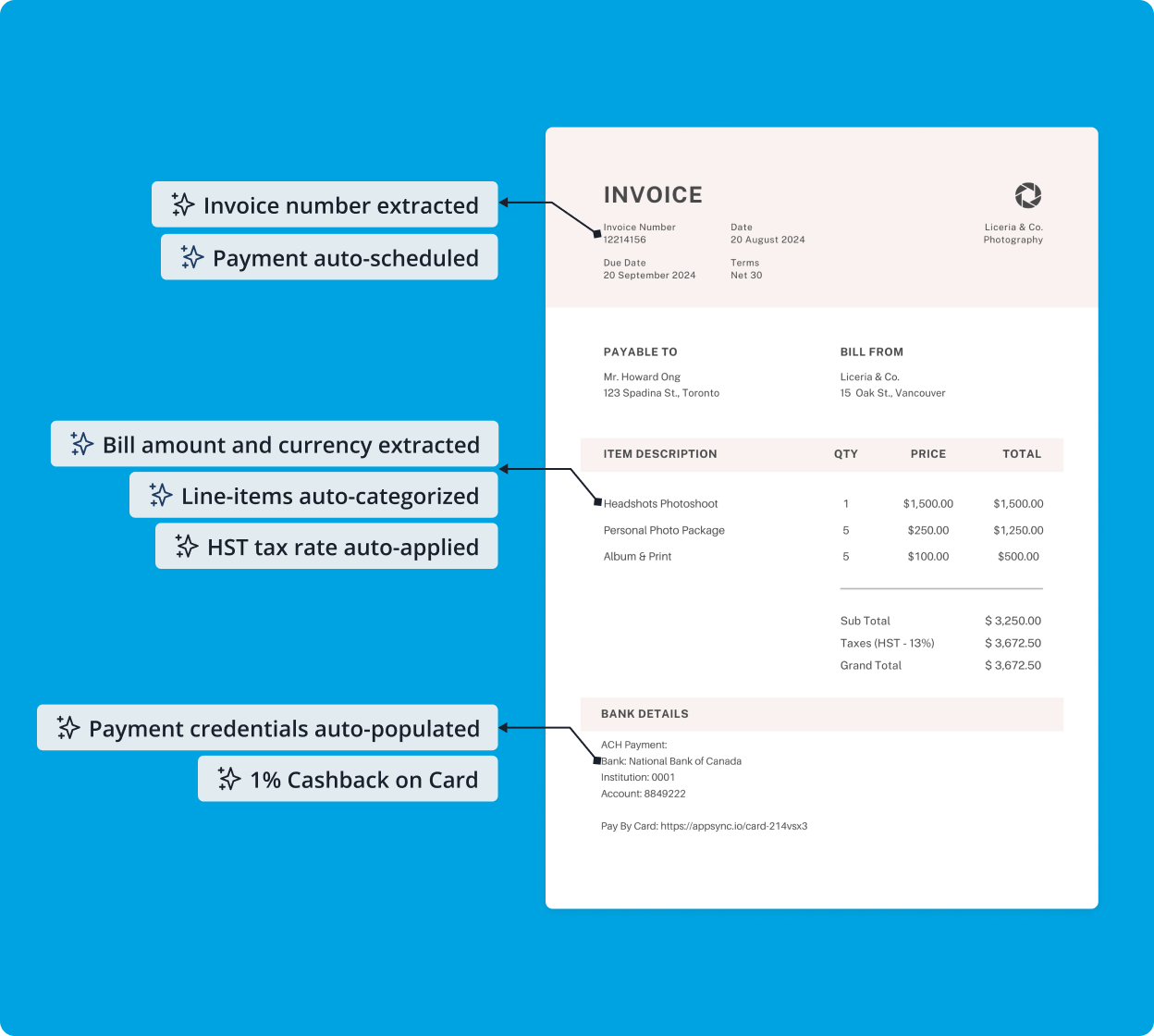

Automate intake with Float’s AI powered OCR and inbox integrations

Streamline approvals with flexible workflows and policies

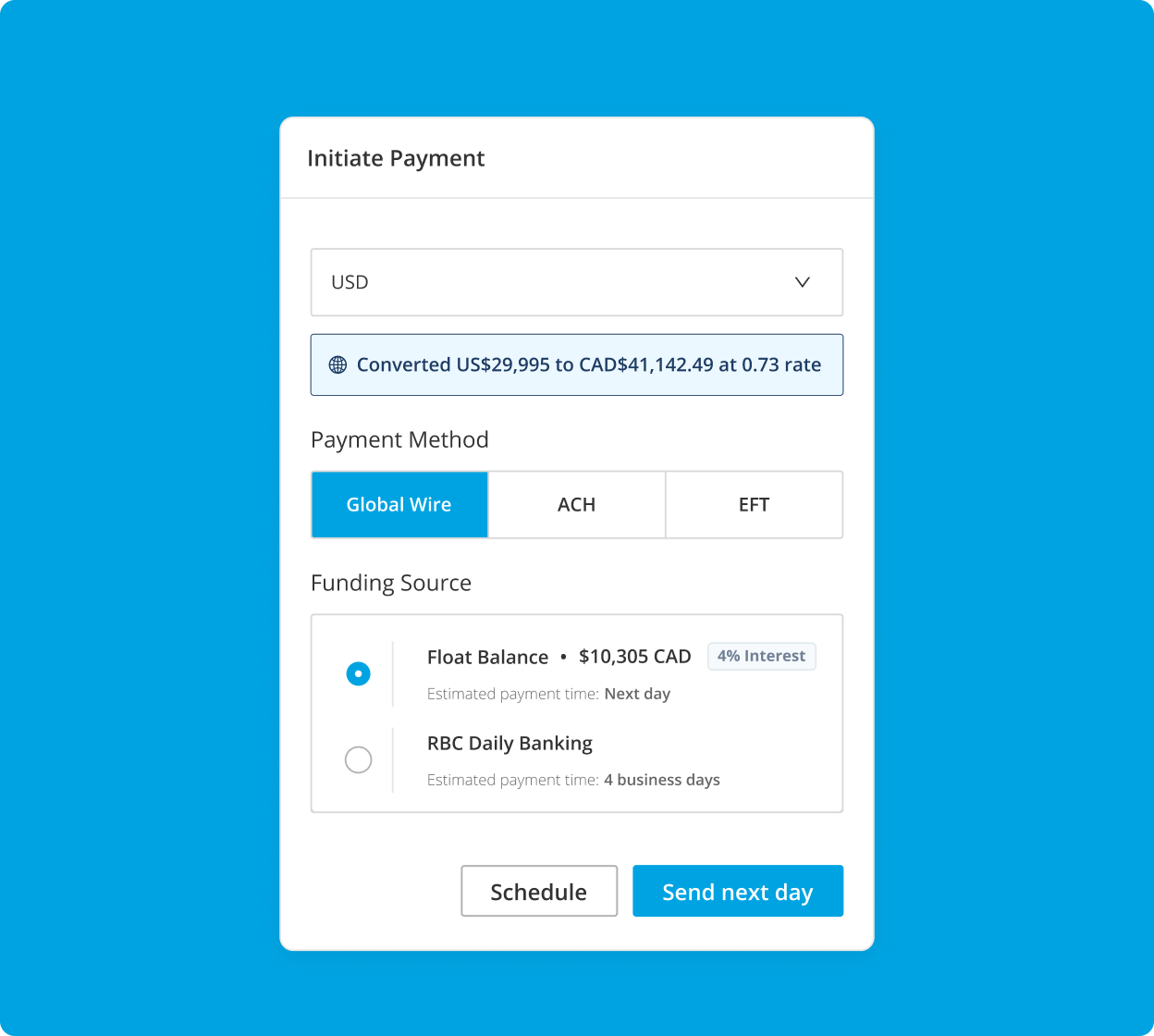

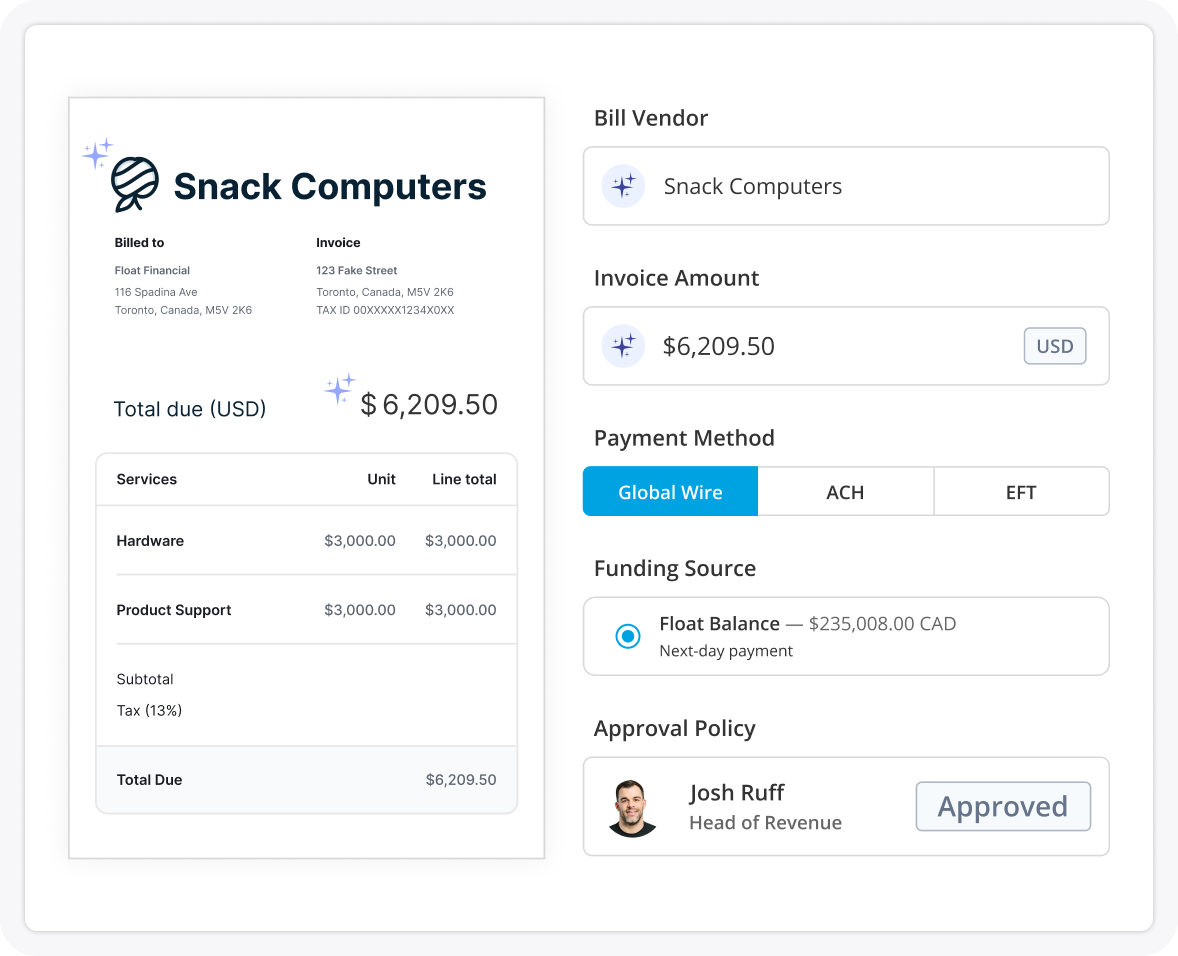

Pay via Global Wires, EFT, or ACH with Float’s next day payments

Rising costs at gas pumps nationwide can make operating vehicles in your business both challenging and expensive. In addition to maintenance, fuel accounts for a major portion of operational spend for companies that use vehicles to provide services. The good news? Finding the best fuel card or fleet card for your business can save you money and give you control over the cost of getting from A to B.

In this guide, we’ll go over how businesses benefit from providing fleet cards to employees and introduce some of the best fleet fuel cards Canada has on offer—plus a few alternatives.

What is a fleet card?

Fleet cards, also known as fuel cards, enable employees to pay for the costs associated with operating a vehicle—including gas, maintenance and repairs—and forward the charge to their company as a business expense. Fleet cards can only be used for vehicle-related expenses, whereas other corporate cards can be used for purchases like office supplies, software subscriptions, or meals.

Fleet cards are for businesses of all sizes with employees who drive a vehicle as part of their job. This includes companies that manage field workers or contractors who commute to different job sites (think plumbers, landscapers and telecommunications techs). Fleet cards are a must for long-haul trucking and last-mile delivery companies that need a way for drivers to pay for fuel and maintenance while they’re on the road.

How does a fleet card work?

If you’re looking into business cards, you might be wondering: What is a fleet card used for? Can’t a corporate card do the same thing?

There are definitely similarities. Employees can use fleet cards to make fuel and vehicle maintenance purchases on the company’s tab the same way they’d pay with a company debit or credit card. Many fleet cards are a type of credit card or charge card that accumulate a balance the employer needs to pay down on a regular basis. Some providers, like Float, also offer prepaid business credit cards for fuel.

Unlike general-use business credit cards, fleet cards enable employers to set strict spending limits and restrict the types of transactions employees make—and even where they can make them.

There are two types of fleet cards:

Closed-loop fleet cards are offered by fuel retailers and can only be used within their fuel networks. One of the major downsides is that drivers have to go out of their way to use them at specific gas stations and truck stops.

Open-loop fleet cards are offered by financial institutions or corporate card providers and can be used anywhere the card’s brand is accepted. Open-loop cards are often Visas or Mastercards.

You can assign a fleet card to an employee or to a vehicle, which makes it easier to track total cost of ownership (TCO) and identify any gas-guzzling lemons in your fleet. The cards also offer security features like flagging unauthorized transactions and allowing you to suspend or cancel non-compliant cards.

Benefits of fleet cards

1) Eliminate the reimbursement rigamarole

With a fleet card, employees don’t have to worry about gathering receipts to submit for approval or wait for reimbursement. In turn, your accounting team doesn’t have to spend time hunting down receipts or juggling payouts, making it easier to control cash flow.

2) Give drivers autonomy without compromising on control

Using a fleet card keeps the budget under control without causing roadblocks for drivers. Fleet cards give you the best of both worlds: the ability to set spend limits and track usage while also allowing your team to fuel up when it’s convenient for them.

3) Get better insights and analytics

Top-performing fleet cards can be integrated with bookkeeping or expense management software to automatically log details like fuel grade, fuel price, and location. This enables you to measure fuel efficiency and maintenance costs so you can spot opportunities for improvement.

4) Take advantage of savings and rewards

Many closed-loop fleet cards offer rebates or discounts on fuel, car washes, tires and mechanic services. Some also offer cash back or points programs. At Float, our corporate cards offer a stack of rewards including 1% cashback and 4% interest on yield account balances—without the restrictions that come with closed-loop cards.

Best fleet fuel cards in Canada

The best fuel card will offer employees flexibility and convenience when they need to fuel up while giving you greater visibility and control around your vehicle expenses. If your employees are driving out-of-province or into the U.S., you need to consider cards that work across borders.

To help you find the card that fits your business, here’s an overview of some of the best fleet fuel cards Canada has to offer:

Closed-loop fleet cards

Shell Fleet Plus: One of the leading fuel cards for trucking companies in Canada. Offers discounts at Shell stations and Jiffy Lube, plus Air Miles. Includes purchase controls and reporting.

Esso and Mobil Business Card and Premier Plus Business Card: Another leader with a wide network offering fuel cards for trucking companies in Canada. Provides volume discounts and, at the Premier Plus level, advanced performance reporting.

Co-op Fleet Cards: A popular option for transport and agriculture companies. Can only be used at Co-op, Tempo and Western Nations Gas Bars in Western Canada.

Open-loop fleet cards

Shell Fleet Navigator: An open-loop Mastercard that has all the benefits of Shell Fleet Plus along with additional chip and PIN security and universal acceptance.

BMO Fleet Card: BMO offers the Mastercard Corporate Fleet Card that can be used everywhere, including Mastercard ATMs. Offers spend controls and reporting.

Foss National Leasing Fuel Card: This open-loop-ish card is accepted at 98% of Canadian fuel retailers. The program includes tire services from Foss, which also offers vehicle leasing.

Corporate cards for vehicle expenses from modern business finance providers

Float: Flexible open-loop corporate card solutions, including fuel cards for small businesses in Canada. Provides built-in expense management and spend limit features and offers 7% total average savings. Built for Canadian businesses.

Keep: General-use corporate card with higher credit limits. Offers basic spend controls and expense tracking. Not available in Québec.

Loop: General-use corporate card with no FX fees. Offers points rewards on purchases. Expense management through a single pane of glass.

Vault: General-use corporate cards that offer 1% cashback on purchases and no FX. Provides multi-currency accounts. Not available in Québec.

Grow Your Business With Float

Canada’s only finance & corporate cards platform that helps businesses save 7% on their spend.

Fuel cards should give you tools to track fuel efficiency and maintenance costs to better understand TCO so you can invest wisely in new vehicles moving forward.

Fleet cards that integrate seamlessly with your tax and accounting or business intelligence software make it easy to stay compliant and measure success.

The best fuel cards for trucking companies in Canada offer expense management solutions that integrate with telematics and electronic logging device (ELD) software for a holistic view of vehicle costs.

Bear in mind that some cards require you to buy a certain volume of fuel each month to qualify for benefits like discounts and rebates. If fuel purchases aren’t a major cost for your business, choosing a general-use corporate card allows you to have the same level of control over employee purchasing, without limitations around what types of expenses they can pay for with their card.

How to apply for fleet cards

Unlike business credit cards, many fleet cards on the market are provided by fuel retailers or corporate card providers, not traditional financial institutions. If you’ve looked into how to get a business credit card before, you might be wondering, what is a fleet card application process like?

You’re in luck. Applying for a fleet card is typically quick and easy. Here’s how.

1) Get your business info together

Applications require information like your company name, location, type, industry, registration documents and your GST/HST number.

2) Gather fleet information

You’ll need to report details like the size of your fleet, your monthly fuel and maintenance costs and your monthly fuel use.

3) Gather financial documents and check your credit score

Some providers may need to look at financial statements, proof of income and your credit score to determine the credit limits you’re eligible for. Some also require a personal guarantee or other collateral.

4) Complete your application

Many closed-loop cards and cards that are available through banks require you to speak directly to a representative about your needs. Open-loop cards, especially those offered by fintechs, typically have fast online application processes. At Float, it takes just 10 minutes to apply for your corporate cards.

5) Get approved and issue your cards

With Float, you can get a 24-hour turnaround on approval. Some providers have longer approval timelines. Once you’ve been approved, you can put rubber to the road and start assigning cards to your drivers.

Managing fuel expenses in your business

According to the American Transport Research Institute (ATRI), fuel accounts for almost a quarter of trucking company operating expenses and costs an average of $22.23 USD per hour, per vehicle in 2023.

Saving on fuel frees up cash in your business. Reducing fuel costs also goes hand-in-hand with lower emissions, which can help you meet climate action targets.

Here’s how you can control your fuel costs in addition to using a fleet card.

Optimize routes and loads

Use telematics solutions to find faster routes and enable drivers to proactively navigate around traffic and construction. Ensure your drivers are only carrying what’s required—i.e., don’t let employees lug their hockey bags around in the company car—as fuel consumption increases by about 1% for every 25 kg in mid-sized cars.

Habits like repeatedly hitting the breaks and speeding up can increase fuel use by up to 33%. Coasting rather than using the accelerator and brakes can also save gas. Proactively coach drivers on techniques to reduce fuel use and minimize wear-and-tear on your vehicles.

Perform preventative maintenance

Replacing air filters, changing oil, and checking tire pressure on a regular basis boosts fuel efficiency and ensures your fleet is in good working order. This reduces unnecessary emergency repair expenses.

Float for fleet management

Fuel cards are great for trucking companies or last-mile delivery companies whose drivers mostly spend money at fuel stations, truck stops, and mechanics. But if you run a trades- or service-based company, and/or provide commuter vehicles for your employees, the best fuel card for you might be a general use corporate card.

Float offers the best business credit card in Canada. Our flexible corporate cards enable you to manage all of your employee expenses, including fleet costs like fuel and maintenance, in one place. Drivers can use Float cards wherever Visa and Mastercard are accepted across Canada.

With Float, you can set the same strict spending limits that you’d expect from the best fleet fuel cards in Canada and customize those restrictions—in real time—for all the purchases your employees need to make. Float’s suite of powerful reporting features show transactions as they happen in the moment and enable you to track budgets vs. actuals over time.

Float also offers high spending limits up to $1M with no personal guarantees. Benefits like 1% cash back, 4% interest on funds kept in your Float and low USD conversion fees rolled up with increased efficiency across your team delivers 7% total cost savings.

Managing business expenses shouldn’t be a headache, but it often can be. If clunky financial processes have started slowing down your team, you may be asking yourself if the time is right to implement a corporate card program.

Before you jump in with both feet, you’ll want to get a sense of how different programs work and which features fit with your company’s needs. Without this knowledge, you risk choosing a solution that adds complexity to your business instead of reducing it.

A well-designed corporate card program should provide clear spending controls, real-time visibility into transactions and streamlined expense management. So, let’s make sure you choose a winner.

In this guide, we’ll walk through everything you need to know to set up a successful corporate card program, from selecting the right provider to setting policies, training employees and optimizing spend management as your business grows.

What is a corporate card program?

A corporate card program centralizes business spending, eliminating the need for employees to pay out-of-pocket and seek reimbursement. Unlike personal or generic business credit cards, corporate cards are issued under the company’s account, with the business handling payments.

The best corporate credit card program will improve visibility, automate expense tracking, and allow finance teams to set spending limits and policies that align with your company’s needs. Because—let’s be honest—no employee loves having awkward conversations about getting reimbursed for work expenses.

Is a corporate card program right for your business?

Maybe! A corporate card program can support different types of businesses in meaningful ways, so let’s explore what you should know to make the best decision for your company.

Here are few common questions about corporate credit cards:

The reality is, fiscal challenges loom large for many startups and business owners. Over a third of businesses in Canada aren’t able to take on any more financing, reporting cash flow as their biggest obstacle. A corporate card program offers flexibility and control for startups and scaleups, ensuring seamless approvals, automated tracking and better cash flow management.

Existing SMBs can also benefit by reducing reimbursement hassles, enforcing clearer expense policies, and leveraging rewards. The right program also minimizes administrative work, giving you time for more strategic priorities, like protecting the bottom line—and actually having time for lunch.

Instantly create and manage cards.

Float provides unlimited* Physical and Virtual corporate cards with no monthly user or card fees. Virtual cards are perfect for digital one-time payments or recurring expenses.

Issue cards to anyone on your team and set custom limits for each employee to avoid overspending

Benefit from high acceptance rates worldwide with Visa and Mastercard cards

The best corporate credit card program streamlines expense management by eliminating the need for manual reimbursements and receipt tracking. With automated workflows and real-time expense reporting, finance teams spend less time chasing down transactions and more time on strategic priorities. This efficiency is a game-changer for startups and SMBs with lean teams.

Another key advantage is better cash flow visibility. Corporate credit cards for employees allow businesses to track spending in real time, set limits for individual employees and prevent budget overruns. This level of control is especially valuable for high-growth companies managing tight budgets and scaling operations.

Many programs offer perks like cashback, travel rewards and waived foreign transaction fees, turning everyday business expenses into financial advantages. Programs also help companies build business credit, opening once-stubborn doors to larger credit lines and better financing options as they grow.

Corporate cards vs. reimbursements: Why a card program is the better option

Managing business expenses effectively is crucial for maintaining financial health and operational efficiency. Traditionally, companies have relied on employee reimbursements, where employees pay out-of-pocket for business expenses and later seek repayment. While this method might seem like it gives the business more control over spending, it often leads to challenges in visibility, control and employee satisfaction.

Implementing a corporate card program addresses these issues by providing enhanced oversight and a more streamlined process.

But how can you ensure employees aren’t overspending when given access to company cards?

Overspending is the biggest concern businesses have around traditional corporate card programs. Issuing cards to employees can feel like it requires a high level of trust, as many businesses worry about potential misuse on non-approved expenses. This concern is especially significant for CFOs and finance teams focused on maintaining strict budget controls—and, in these uncertain economic times, this includes pretty much every business in Canada.

But the problem with relying solely on reimbursements is that it places the financial burden on employees, requiring them to front personal funds for business-related expenses. This approach can lead to both employee dissatisfaction and financial strain, especially if reimbursements are delayed. Employees get frustrated by having to wait until the next pay cycle or even month-end to get back funds they’ve put on personal cards. Additionally, companies miss out on potential rewards (e.g. cashback) and added visibility (e.g. surprise employee expense reports at month-end) that come with corporate spending, both of which could otherwise contribute to the organization’s financial well-being.

Modern corporate card programs like Float combine the advantages of traditional corporate cards and the control of reimbursements. Here’s how Float addresses these concerns around over-spending:

Real-time visibility: Get immediate insights into all transactions, so your team can monitor spending as it happens. This transparency ensures that any unauthorized expenses are quickly identified and addressed.

Customizable spending controls: Set specific spending limits and policies for each cardholder (including vendor-specific cards), ensuring expenditures align with company budgets and policies.

Automated expense management: Automate expense tracking and reporting, reducing administrative burdens and minimizing the potential for errors or fraudulent claims.

Employee empowerment without financial strain: By providing corporate cards, employees are relieved from the need to use personal funds for business expenses, leading to improved satisfaction and morale.

Implementing a corporate card program actually provides more financial control and rewards, while helping to foster a positive and efficient workplace culture.

How to set up a corporate card program

1. Assess business needs

Evaluate your current spending patterns before implementing a corporate credit card program. You may not need a program if your business purchases are minimal or centralized. However, companies with distributed teams, frequent travel or high recurring expenses (think software subscriptions or advertising) can benefit significantly.

Next, consider the number of employees making purchases, the types of expenses that could be consolidated under a corporate card and the potential rewards or cashback opportunities. A well-designed program will give you control and efficiency, particularly for remote teams that need seamless purchasing capabilities.

2. Choose the right provider

Selecting a corporate card provider depends on business priorities. Some companies are motivated by cashback and rewards (okay, we all love these), while others focus on control and automation. Key features to evaluate include customizability, automation for reconciliation and strong spending controls.

Another critical factor is the ability to issue virtual and physical cards on demand. This ensures your employees will have the access they need without unnecessary risk. Choosing a flexible provider means the program can evolve with your business rather than become a bottleneck.

3. Set up policies and controls

Establishing a clear company credit card policy is essential for maintaining compliance and preventing misuse of corporate cards. A well-structured expense policy should outline what kinds of purchases are allowed and any required approvals.

Similarly, a purchasing policy ensures employees follow a standardized process for vendor payments, whether or not a purchase order system is in place. A travel policy for companies with frequent travellers should define what types of expenses are covered, from flights to meals and accommodations.

Automated approvals, built-in compliance checks and real-time monitoring can reinforce policies without relying solely on manual oversight.

4. Train employees

Having a policy isn’t enough, so don’t be shy about actively communicating expectations and best practices. Holding training sessions, hosting lunch-and-learn events or providing digital resources can make policies more accessible and easier to follow.

Training should also emphasize practical aspects of card use, like submitting expenses, determining what types of purchases are permitted and requesting temporary card access if needed. Overcommunication is often better than assuming employees will instinctively follow the guidelines.

Don’t forget: training materials and processes should be revisited regularly as your business scales to ensure they remain relevant and practical.

5. Monitor, adjust and optimize

A corporate credit card program is not a set-it-and-forget-it solution. It requires continuous oversight to maximize efficiency. Finance teams should track spending patterns to ensure expenses align with company policies and identify any inefficiencies, like unnecessary reimbursements due to lack of card access.

Another key area to monitor is the reconciliation process. If month-end closing is still a time-consuming manual task, or if finance teams frequently must correct errors retroactively, this may signal the need for adjustments.

6. When to consider switching providers

A corporate card program that once worked well may become a bottleneck if it lacks automation, restricts access to employees who need it or creates unnecessary administrative work.

If finance teams frequently encounter manual reconciliation, need to increase reimbursement requests or struggle to maintain visibility over spending, it might be time to reevaluate your current provider.

You’ve also got to think long-term. If your corporate card program was initially designed for a small team but now struggles to accommodate a larger, more distributed workforce, switching to a more scalable provider can save you significant time and resources.

7. A better answer to the question: Who gets a corporate card?

Traditional corporate card programs restricted access to senior employees, but modern solutions allow businesses to issue cards based on need rather than hierarchy. A corporate card should empower your people and simplify spend, no matter how long they’ve been on your team.

With temporary virtual cards, businesses can grant short-term access without permanent commitments.

No more worrying about how to get a business credit card into the right hands in time. For example, imagine issuing a card for a two-day conference that deactivates automatically, or providing an expense card for contract employees. This flexibility reduces reimbursement delays and financial strain on employees while ensuring company funds are available when needed without unnecessary risk.

Let’s take a look at Float in action

For fast-growing companies, managing expenses at scale can quickly become a challenge. Practice Better, a Toronto-based software company in the health and wellness space, faced this reality as their team expanded and new departments formed. With financial processes still partially outsourced, the finance team needed a more efficient, scalable solution to keep up.

“Things would not get booked in correctly and we wouldn’t know until after close. And by then you’re almost into the next month,” says Deena Lu, Controller at Practice Better.

The company successfully transitioned to an entirely in-house financial model by implementing Float. With automated approvals, built-in controls and real-time expense tracking, Practice Better streamlined operations while mitigating risk.

“[With Float], we’ve decentralized the approval process so that it’s not all on finance,” says Deena. “It’s really the team leads now who are responsible for the budget and can approve their team’s spend requests.”

The result? A more efficient finance team and a company-wide culture of responsible, transparent spending prove that the right corporate card program can seamlessly scale with a growing business.

The smarter way to manage company spend

A well-structured corporate card program streamlines expense management, improves cash flow oversight and empowers employees while maintaining control. It provides you with flexibility in offering corporate credit cards for permanent employees or setting up expense cards for contract staff.

If the benefits sound tempting, it could be time to assess your business needs and see if Float corporate cards could help support your goals. With the right provider, clear policies, and automation, you can quickly scale your financial operations.

We think we’re offering the best business credit cards in Canada, and we’re happy to show you why. Whether you’re a startup, SMB or growing enterprise, the right program can save time, reduce administrative burdens and even unlock rewards.

Book a demo with our team to see how a Float corporate card program could work for you.

Enable team spending without losing control.

Float is a smart corporate card backed by intelligent spend management software. The software provides a real-time overview of individual, department, and category spend so you can scale with insight.

No more Past Due late fees or last-minute-declined-payments because of lack of visibility on your corporate cards.

The U.S. has just announced new tariffs on steel and aluminum imports from Canada. While the more widespread proposed tariffs still remain on hold until March 4, these latest developments mean rising costs and supply chain disruptions are on the horizon. If tariffs go into effect, small businesses will feel the squeeze first. Higher costs, disrupted supply chains, and tighter margins mean that businesses need financial tools that move as fast as they do.

So many questions remain. Will tariffs actually happen? Which industries will be hit hardest? And how can your business stay resilient, no matter what?

In this article, we’ll break down what tariffs are, how they might impact Canadian SMBs and, most importantly, the proactive steps your business can take to navigate this period of economic uncertainty. You’ll learn practical strategies to mitigate risks, manage costs and keep your business agile in the face of potential trade disruptions.

What is a tariff?

A tariff is a tax imposed by a government on imported or exported goods. These taxes are used to:

Protect domestic industries

Generate government revenue

Influence international trade policies

In this case, President Trump’s proposed tariffs include a 25% tax on Canadian imported goods heading to the US and a 10% tax on Canadian energy products.

How will proposed US tariffs on Canada impact SMBs?

If these tariffs go into effect, they’ll likely result in:

Higher costs on imported goods and materials

Price increases as businesses offset rising production expenses

Supply chain disruptions, forcing companies to renegotiate with suppliers

Reduced demand for Canadian exports, as US buyers seek domestic alternatives

In the long run, this could lead to more nearshoring, diversified supply chains and a greater focus on local partnerships.

4 ways small businesses can get ready for US tariffs on Canada

Even if tariffs don’t happen, preparation is key. Here’s how Canadian SMBs can stay ahead:

1. Prepare for extended economic uncertainty

Review your expenses and cut non-essential costs. This might include:

At Float, we’re proud to support thousands of Canadian SMBs with financial tools that help them navigate uncertain times. Whether through improved expense management, efficient payment solutions, or financial insights for smarter decision-making, we’re here to ensure your business stays competitive and resilient.

Canadians use credit cards more frequently than any other payment method, and 57% say it’s because of the rewards they get for spending. If the perks are paying off for the average shopper, just imagine what Canadian businesses with more bills and buying power stand to gain from the benefits that come with corporate credit cards.

But not all corporate card programs are created equal. Selecting the right one requires a bit of research—and thankfully, we’ve done the legwork for you.

In this guide, we’ll break down everything you need to know about corporate credit cards in Canada: how they work, the perks and how to choose the best corporate card program for your start-up, scale-up or SMB.

What is a corporate credit card?

A corporate credit card, often called a corporate card or commercial card, is a card issued to employees to manage business expenses. Corporate cards typically offer more features than your average personal credit card, like higher limits, expense tracking, and enhanced reporting tools.

In Canada, the terms “corporate credit card” and “business credit card” are often used interchangeably, but there are a few key differences.

Business credit cards are suited for entrepreneurs, sole proprietors, or small businesses and require a personal credit check and guarantee. Think of these like an extension of your personal credit, where the card owner is held liable for the balance if the business can’t pay.

Corporate credit cards are for businesses with more spending power—like scaling start-ups or SMBs. They typically offer higher spending limits, automated controls and no personal guarantees (meaning you won’t need to risk your personal assets or credit to secure a card for your business).

Corporate cards are issued based on your business’s financial health rather than the applicant’s personal credit. (Note: they may also have other eligibility requirements). The company is responsible for paying the balance in full each month—not the “cardholder” or employee the card is assigned to.

What is a corporate card program?

A corporate card program makes managing your business expenses faster and easier by bringing all credit spending into one place.

Here’s what to think about when building your corporate card program:

1. Issuance and eligibility

Full-time employees who regularly manage expenses—like client lunches, travel or team purchases—can benefit the most. For contractors or temporary staff, set clear guidelines on if and how they can use a card.

2. Types of charges

Spell out exactly what your corporate cards can be used for. Whether it’s travel, software subscriptions or team events, a clear expense policy helps your employees know how to use the card appropriately.

3. Responsibility for payments

With corporate cards, your business handles payments—not the employees. This takes the pressure off your not-so-finance-savvy teammates while giving whoever pays the bills complete visibility and control over spending.

4. Credit limits and policies

Set limits that match the needs of your team. For example, you might have higher limits set for frequent travelers or decision makers. Use tools like category-specific caps or single-use virtual cards for added security and flexibility.

5. Reconciliation

Here’s the best part about corporate cards: you can finally say goodbye to chasing receipts and juggling spreadsheets.

With automated tools, employees can upload receipts instantly, so your finance team can track and approve expenses in real time. For employees, this removes the hassle of out-of-pocket payments and slow reimbursements.

Who offers corporate card programs in Canada?

Traditional banks

Canada’s major banks, such as RBC, TD and Scotiabank provide corporate credit cards that often include features like rewards programs and travel perks. These cards are well-suited for larger enterprises but may come with higher fees, lengthy application processes and less flexibility.

Modern fintech providers

Fintech companies have introduced a new generation of corporate card solutions designed for more flexibility. These programs often prioritize ease of use, offering tools like virtual cards, automated expense tracking, and accounting integrations. Some providers (like Float) focus specifically on Canadian businesses, offering options like CAD and USD card limits with lower fees and faster approval processes.

Types of corporate credit cards

Traditional banks

Canada’s major banks, such as RBC, TD and Scotiabank provide corporate credit cards that often include features like rewards programs and travel perks. These cards are well-suited for larger enterprises but may come with higher fees, lengthy application processes and less flexibility.

Modern fintech providers

Fintech companies have introduced a new generation of corporate card solutions designed for more flexibility. These programs often prioritize ease of use, offering tools like virtual cards, automated expense tracking, and accounting integrations. Some providers (like Float) focus specifically on Canadian businesses, offering corporate card options like CAD and USD card limits with lower fees and faster approval processes.

Types of corporate credit cards

Corporate credit cards

Corporate cards or corporate credit cards are your versatile, all-purpose cards designed to cover a wide range of business expenses and day-to-day operational costs. They’re a great option for businesses looking for a straightforward way to manage spending without focusing on special categories.

Charge cards require the full balance to be paid off at the end of each billing cycle, making them ideal if your business wants to maintain disciplined spending habits. With higher spending limits than traditional credit cards, they’re great if your company is growing or has variable cash flow. If you plan on spending a minimum of $10,000 per month and want to pay it off quickly, a charge card could be for you.

Purchasing cards (P-cards)

P-cards are built for procurement and vendor payments and eliminate the need for traditional purchase orders or invoices. These cards simplify tracking vendor-specific expenses, reduce paperwork and ensure spending stays within your allocated budgets.

Travel and entertainment (T&E) cards

T&E cards are designed for travel-related expenses like flights, hotels, car rentals, and client dinners. They often come with travel perks like discounted rates, travel insurance and airport lounge access, making them handy for sales teams or frequent travelers.

Virtual cards

Perfect for online transactions, virtual cards offer added security and flexibility to your business. These digital-only cards are ideal for managing subscriptions, one-off purchases or vendor payments online.

Using a virtual card platform, your accounting team generates a single-use card customized with a specific spending limit and assigns it to an individual employee or vendor. This limited nature minimizes the risk of fraud and is especially useful for recurring expenses.

Ghost cards are assigned to vendors, projects or departments rather than individuals. They help your business track spending by budget or recurring expenses, offering an easy way to monitor compliance and streamline reconciliation.

Fleet cards

Designed for companies with vehicles, fleet cards manage fuel, maintenance, and other vehicle-related costs. They often include fuel discounts, detailed reporting on mileage and consumption, and tools to track vehicle expenses with ease.

Expense management cards

Expense management cards combine payment functionality with integrated tracking and approval workflows. They can reduce the time your finance team spends on reconciliation by syncing directly with accounting software.

Prepaid corporate cards

Unlike traditional credit cards, prepaid corporate cards require you to load funds onto the card upfront instead of borrowing from a bank. This gives your business more control over expenses while helping you avoid debt. Explore the prepaid business credit card Canada’s businesses love.

Types of corporate credit cards comparison chart

Top 4 benefits of corporate cards

1. Take back time with automated workflows

Corporate cards eliminate the hassle of managing paper receipts and processing reimbursements. With real-time tracking and automated expense reporting, your finance team will save hours on admin.

For start-ups and SMBs operating with lean resources, this means your staff spends less valuable time sorting through expense reports. For mid-market companies, finance teams will appreciate the ease of categorizing expenses without chasing receipts from hundreds of employees each month.

2. Drive smarter decisions with better cash flow

Corporate cards provide better visibility into company spending, allowing you to track it in real time and set individual limits. This is especially beneficial for start-ups and scale-ups diligently managing cash flow in the early stages of growth when budgets can be tight.

3. Save more and earn rewards

Many corporate card programs offer rewards, such as cashback, travel benefits, or discounts on essential services. At Float, we help businesses save an average of 7% on their spend through a combo of rewards like 1% cashback, 4% interest on deposits, no foreign transaction fees with our USD cards and employee time savings. We call that a win.

4. Control your capital by building credit

Building credit is vital for growth. For start-ups, corporate cards grant you access to higher business credit card limits without personal guarantees, creating a strong foundation for future financing opportunities. For larger SMBs and mid-market companies, you can strengthen your credit position to access larger credit lines as you scale.

Risks to be aware of

Security and fraud: Stats show Canadian businesses experience a higher rate of fraud (20%) than Canadian consumers (13%). Make sure to look for features like virtual cards for one-time purchases, transaction alerts and the ability to freeze a card instantly if something seems off.

Compliance headaches: Keeping track of expenses and ensuring they align with tax regulations can get complicated. Automate tracking and reporting to simplify these operations, giving you peace of mind and making tax season less stressful.

Overspending: Without proper limits, it’s easy for spending to spiral. Set clear boundaries with spend limits and restricted categories so you’re always in the driver’s seat.

Confusion: Sometimes, employees simply don’t know the rules. A quick onboarding session or a set of clear expense guidelines can make all the difference and keep everyone on the same page.

When you choose a corporate card program with smart controls and built-in security, you can enjoy all the perks without the headaches.

How to choose the right corporate card

Currency: If your business operates across borders, look for a card that supports CAD and USD spending without high foreign transaction fees. For example, Float avoids conversion fees by linking directly to your CAD or USD bank account, while cards like the RBC Avion Visa Infinite Business focus solely on Canadian spending.

Fees: High annual fees can eat into your budget, so consider whether the benefits outweigh the cost. Float has no annual fees, while traditional cards like the AMEX Business Platinum charge upwards of $799 annually, offering premium travel perks in return.

Rewards: Cashback and point-based systems are common, but the value of these rewards can vary. Float offers unlimited 1% cashback on all spending, while cards like the Scotiabank Momentum for Business Visa provide 3% cashback on specific categories like office supplies.

Features and controls: Real-time expense tracking, virtual cards, and integrations with accounting tools can save your team hours of work. Float excels in this area, offering both physical and virtual cards with spending controls, while traditional banking options focus more on rewards.

The best card for you depends on your goals, spending habits, and priorities. For a detailed breakdown of what’s available, compare Canadian corporate cards here.

Best corporate credit cards in Canada

Choosing the best business credit card Canada offers can help you streamline expenses, earn rewards, and maintain better control over your company’s finances.

Here’s a brief overview of the leading programs to make an informed decision:

Float: Offers no annual fees, unlimited 1% cashback, and advanced expense management tools with up to 7% savings on average.

Keep: Provides higher credit limits, up to 4% cashback rewards, and no fees.

Loop: Allows spending in multiple currencies with no foreign exchange fees.

Selecting the right corporate card comes down to how your business spends and other factors like your industry. For example, a Canadian e-commerce business often purchasing from US suppliers, might prioritize a card that doesn’t charge foreign transaction fees. Or, a marketing agency managing several online ad accounts might prioritize a card that tracks spending per client.

Once you’ve selected a corporate card and have confirmed you meet the qualifications, applying is quick and easy with most providers.

Gather your business info: You’ll need basic details like your company name, location, type, industry, registration documents and financial figures.

Verify identities: Provide ID for key shareholders or decision-makers, as required.

Gather financial documents: Some providers may ask for proof of income or financial statements.

Complete your application: Many fintechs offer online applications, while traditional banks might require more paperwork and in-person appointments. At Float, our fast online application only takes 10 minutes.

Get approved: Approval times vary—some cards are ready in 24 hours (like Float), while others take a few days.

Once approved, you can start issuing cards to employees and using your new corporate card program to simplify spending.

Grow Your Business With Float

Canada’s only finance & corporate cards platform that helps businesses save 7% on their spend.

Start by establishing clear policies that outline which employees will receive cards, set spending limits, and define approved expenses.

Next, take advantage of your provider’s tools to set up spending controls. Features like customizable limits, category restrictions, and virtual cards for one-off purchases help you keep expenses organized and transparent.

Once the program is set up, train your team on how to use it effectively. A quick overview of the guidelines, including how to upload receipts and manage expenses, will set them up for success.

Finally, monitor spending using real-time reporting tools. This allows you to spot trends, adjust limits, and refine your policies to better fit your business as it changes.

Float offers Canadian businesses a smarter, simpler way to manage spending. With no annual fees, unlimited 1% cashback on every dollar spent and tools like real-time tracking and virtual cards, Float puts you in control of your finances.

Unlike traditional corporate credit cards, Float corporate cards provide high spending limits with no personal guarantees, making it easier to grow without the stress of added liability. You’ll also earn 4% interest on funds held in Float and enjoy a seamless onboarding process that gets you started in as little as 24 hours.