Business credit cards might not be the flashiest part of running a company, but getting the right one can quietly power everything from payroll to plane tickets. Finding the best business credit card in Canada is worth your time, so your spending doesn’t unravel your company goals.

Credit is a critical topic for businesses. Nearly 30% of Canadian independent businesses surveyed still carry pandemic-related debt, with an average balance of $65,000. While there have been some reductions in credit card fees, only 7% of businesses eligible for reductions have noticed savings.

But here’s the catch: not all business credit cards are built for how you do business. That’s where this guide comes in. We’ll help you find the one that pulls its weight.

Try Float for free

Business finance tools and software made by Canadians, for Canadian Businesses.

A business credit card is exactly what it sounds like—a credit card built for business spending. Whether you’re a sole proprietor or running an incorporated company, a business card helps keep your work expenses separate from your personal ones (because no one wants to sort through a messy statement at tax time).

But it’s not just about staying organized. Business credit cards often come with perks tailored to how companies spend. They can also help you smooth out cash flow, cover short-term expenses and build your business credit profile, which comes in handy when it’s time to scale up.

Why are business credit cards important?

As a small business owner in Canada, you’re juggling many responsibilities, and one of the most critical is tracking your expenses. Let’s break down why this matters and how to do it effectively.

Why expense management matters

From tax time to audit season, strong expense management helps you stay compliant, save money and make smarter decisions.

Keeps you compliant with CRA regulations

Enables you to claim tax rebates and benefits

Prepares you for potential audits

Provides clear insights into your business finances

Key responsibilities of small business owners

These key responsibilities aren’t just best practices; they’re must-dos if you want to stay onside with the CRA and unlock financial benefits.

Accurate tracking

You’re responsible for recording all business expenses and reporting them correctly to the CRA.

Tax rebate opportunities

Proper expense tracking allows you to apply for GST, HST and other tax rebates in Canada, potentially saving your company significant money.

Audit readiness

Good record-keeping ensures you can pass an audit if one comes your way, reducing stress and potential penalties.

Can I use a personal credit card for business expenses?

It’s a common question. After all, as a small business in Canada, it can feel like the easiest option for you to start with.

Here’s what’s important about having a dedicated business credit card:

Separates personal and company finances

Builds business credit

Offers higher spending limits

Provides company-specific rewards and perks

Makes tax time a breeze

Sounds good, right? Now, let’s check out the different kinds of business credit cards available for small businesses in Canada.

Types of small business credit cards in Canada

There are two main types of small business credit cards in Canada: cards from traditional banks and cards from modern fintech providers.

Traditional banks offer corporate cards with familiar perks. However, banks often design these cards with larger, established companies in mind, which means higher fees, more paperwork and slower approval processes. In some cases, we’re talking about weeks to open a credit card. If you get approved at all.

On the other hand, fintech providers are bringing business credit cards into the modern age. With fast approvals, virtual cards, real-time expense tracking and integrations that actually talk to your accounting software, they’re built for businesses that want more control and less hassle. For example, you can open an account with Float and get started with a corporate card in close to 24 hours.

5 best practices for business credit card use in Canada

Whether you’re just starting out or scaling up, a few smart habits can help you avoid unnecessary costs, build credit, and make the most of your spending.

Here are 5 best practices to keep your business finances on track:

Keep business and personal spending separate

Mixing expenses can get messy, especially at tax time. Use your business card strictly for business to stay organized and protect yourself legally if you’re incorporated.

Pay off your balance every month

Interest charges eat into your cash flow fast. Paying in full helps you avoid fees and can boost your business credit score over time.

Don’t spend right up to your limit

High credit usage can hurt your credit score. Keep it under control by tracking your spending or making early payments mid-month.

Pick a card that pays you back

Look for a card with low fees and rewards that match your business’s spending, whether on travel, office supplies, or digital tools.

Avoid cash advances

They’re pricey. If a vendor doesn’t take cards, consider other financing options instead of pulling cash from your line of credit.

Key features to look for in a business credit card

When you’re shopping around for the best credit card for business in Canada, keep these factors in mind:

Annual fee: Is it worth the perks?

Rewards structure: Points, cash back, or travel miles?

Additional cardholders: Can employees get cards, too?

Foreign transaction fees: Important for international businesses

Insurance coverage: For travel, purchases, or even cell phones

Digital experience: Software integrations, easy-to-use banking portal and easy expense tracking

Remember, the best card for you depends on your business needs. A small local shop might benefit from different features than a globe-trotting consulting firm.

Not quite. Corporate cards are typically for larger companies and often require the business to be liable for charges.

It’s not recommended. Mixing personal and business expenses can create accounting headaches.

Regular use and timely payments on a business credit card are reported to business credit bureaus, helping establish your company’s credit history.

If you are a business owner, we recommend choosing a company credit card that doesn’t require personal background checks, can offer you high credit limits, and is easy to get started with! Float is a great option with no personal guarantee requirements!

Despite transformative innovation in accounts payable software like AI-driven optical character recognition (OCR) and workflow automation, 69% of Canadian SMBs still feel that invoice processing and vendor payment needs to be more efficient. The accounts payable system that today’s growing businesses rely on stifles operations. Twenty-seven percent of Canadian SMBs report that their most pressing challenge is delays in incoming and outgoing payments while 18% report that cash flow management issues are their biggest obstacle.

In this article, we’ll discuss why today’s businesses need better solutions for AP automation and how to choose the best accounts payable automation software in 2025.

What is accounts payable software?

Accounts payable (AP) software solutions automate invoice and bill intake, GL coding, matching, validation, and approvals to streamline the process of paying your suppliers and vendors.

Business leaders often look into investing in accounts payable workflow software when their teams get fed up with tedious manual data entry and when their current approvals and payment processes create frustrating bottlenecks. But beyond just saving you time and labour, the right AP software solutions also give you greater control over your expenses, provide more accurate invoice validation and help you close your books quickly.

The best accounts payable automation software have embedded payment and business options, so you can make EFT payments to your vendors and contractors or pay them via ACH, international wire transfer, cheque or credit card without having to navigate through your online banking portals every time an invoice comes due.

Why Canadian businesses need accounts payable automation software

Your AP strategy is where you put your budget into action. Accounts payable automation software is an essential tool for monitoring and controlling where your cash is allocated so you can keep your business running and invest wisely in growth-driving opportunities. With AP automation software, businesses can:

Eliminate manual data entry. The best AP software solutions offer OCR that automatically transfers information from invoices and receipts into the system and applies appropriate general ledger (GL) and tax codes.

Enhance security and reduce fraud. Two- and three-way matching automatically check invoices against purchase orders (POs) and goods receipt notes (GRN) to ensure you’re paying the right person.

Improve vendor relationships. If you’re trying to figure out how to pay an invoice faster for a valued vendor, you can schedule transactions and track payments with an AP solution to reduce days payable outstanding (DPO), build trust with your vendors, and take advantage of early payment discounts.

Control spend and manage expenses. Track spend in one place to get insights into your budget. With an AP automation solution like Float, you can also proactively set limits (not just company handbook policies) on corporate card spending to keep everyone on track.

Make global payments. Leading AP solutions allow you to seamlessly pay US invoices and international invoices within the platform.

Close the books faster. Automatically reconcile invoices in your AP solution with your accounting software.

Make EFT Payments with Float

Canada’s best-in-class EFT, ACH, and Global Wires payments platform — plus average savings of 7%.

What to look for in accounts payable software in 2025

Today, the status-quo accounts payable system for a Canadian businesses includes a patchwork of point solutions that breeds bottlenecks and holds businesses back.

The best accounts payable automation software provides holistic, end-to-end workflows, speedy payments and cash flow management, facilitating financial momentum so you can grow your business. Look for an AP software solution with key features like:

✓ AI-driven OCR for automated receipt and invoice intake

✓ Automatic GL and tax coding

✓ Automatic two- or three-way invoice matching and validation

✓ Employee expense management and reimbursement capabilities

✓ Customizable approvals controls and automated approvals processes

✓ Multiple ways to pay invoices including EFT and ACH, wire, credit card or via platform-based account

✓ International payment capabilities plus low- or no-fee FX

✓ Payment tracking for both you and your vendors

✓ Reliable two-way sync integrations and automatic reconciliation with accounting software

Does accounts payable workflow software handle employee expenses?

Most AP software workflows lump employee expenses—like travel, meals, fuel, and supplies—in with vendor invoices, even though they should be treated differently. Typical AP solutions focus on facilitating vendor payments and most businesses opt to (or have to) reimburse employees through payroll.

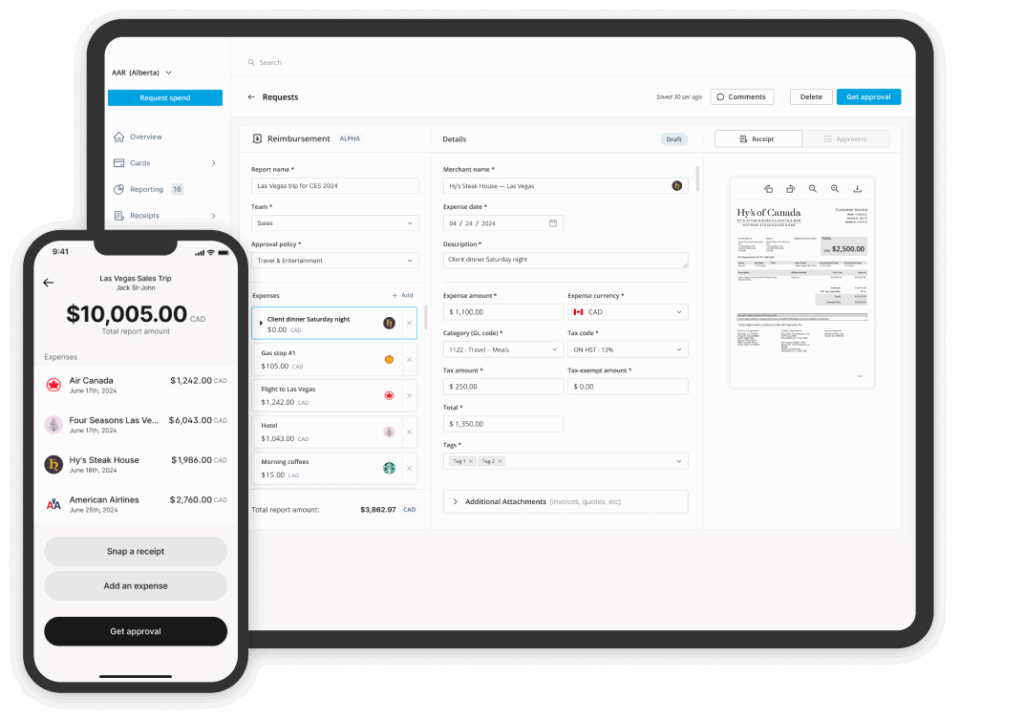

With an AP automation platform like Float, corporate card spending and reimbursements happen seamlessly in the same place as invoice management and vendor payments.

Float lets you see how spending across all your corporate cards impacts cash flow as transactions happen. You can also customize spending limits in real time, giving you total control over when and how your team spends. You can use Float to process same-day reimbursements, but with corporate cards, you don’t have to worry about reimbursements at all.

6 best accounts payable software for Canadian businesses in 2025

Float Bill Pay is an accounts payable software small business teams love to use, but there are other options out there. To help you make an informed decision about the accounts payable software that fits your business, here’s how Canadian AP software solutions stack up.

1. Float Bill Pay

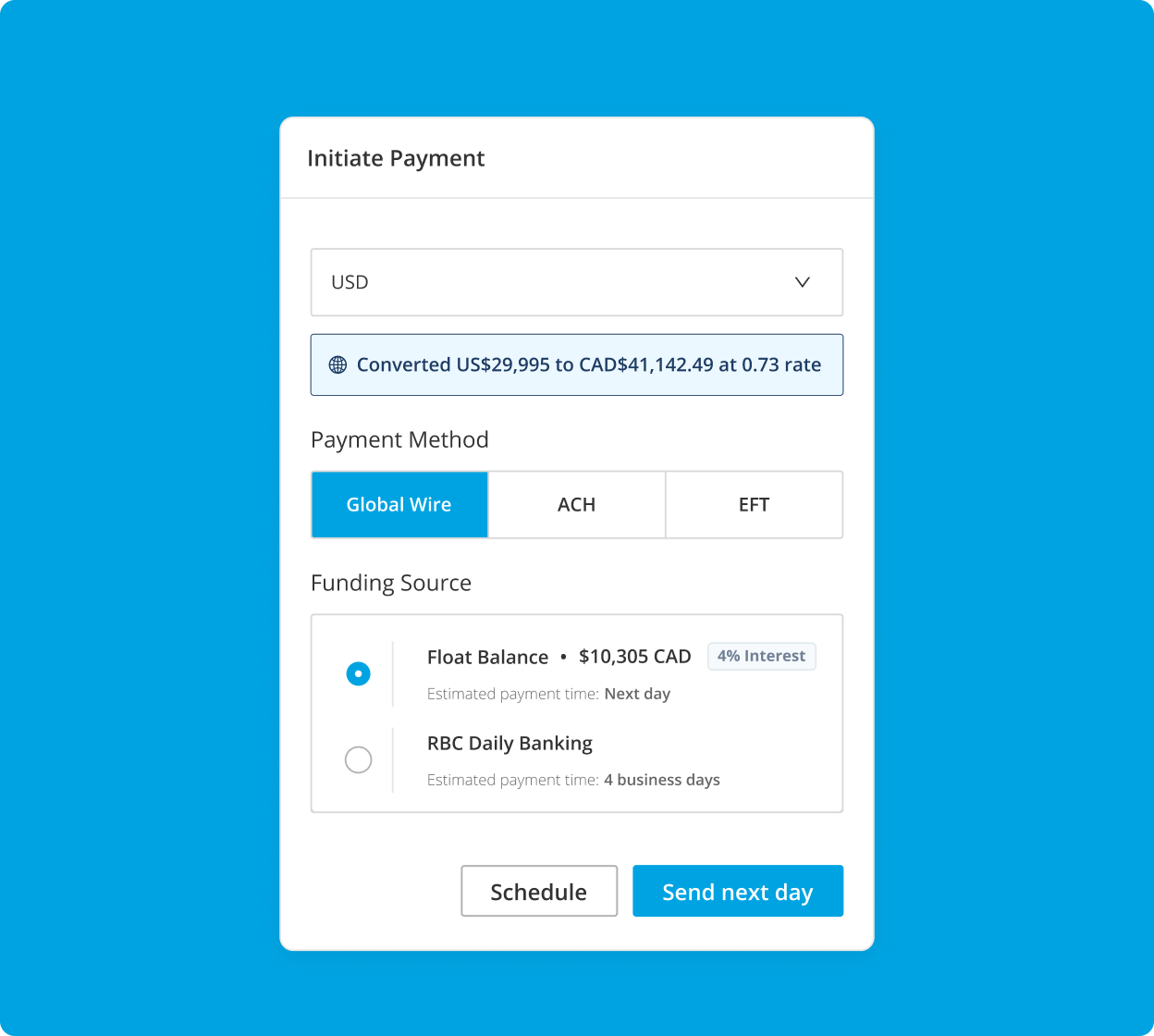

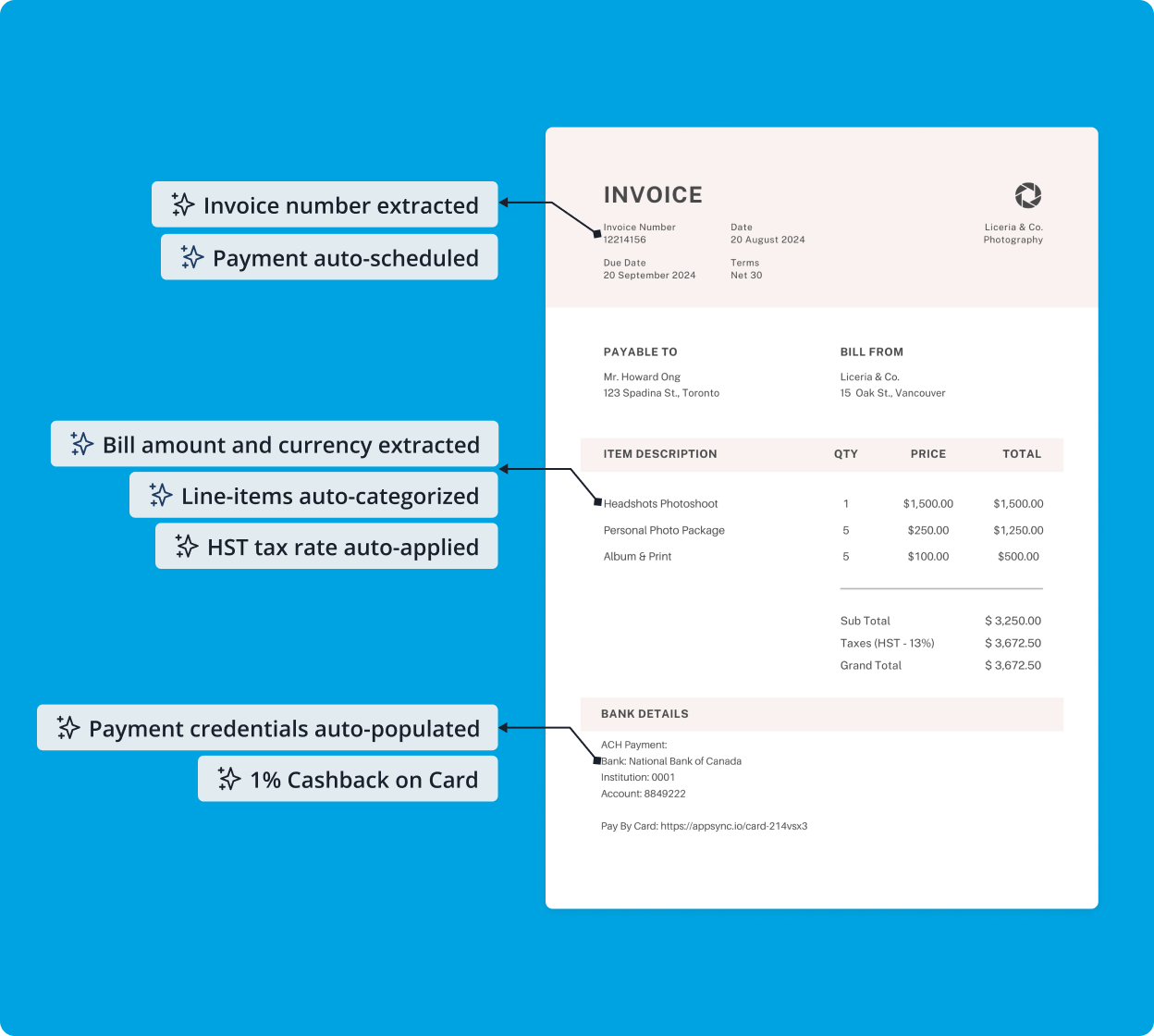

Float Bill Pay is an intuitive financial management platform built in Canada for Canadian businesses of all sizes. Designed for efficiency, it offers seamless invoice and receipt capture workflows powered by leading-edge AI data extraction. With automated GL and tax coding, custom approval workflows and embedded EFT/ACH and wire payments (CAD and USD), managing payments has never been easier. Float also includes built-in FX services, ensuring smooth international transactions.

Payments made through your Float balance arrive within one to two business days, with real-time payment tracking for vendors. The platform integrates effortlessly with QuickBooks, Xero and Netsuite through two-way sync, along with HRIS and Slack integrations.

Float Bill Pay is available at a SaaS pricing of $0 to $10 per user per month, with enterprise pricing options. EFT/ACH transactions are just $1 per transaction. Additionally, Float combines best-in-class accounts payable automation software with corporate and virtual cards for employee spend management. Businesses can also benefit from 1% cashback on corporate card purchases and earn 4% interest on CAD and USD business balances.

2. Plooto

Plooto is an AP and accounts receivables (AR) automation software. It’s a good point solution for SMBs looking for status-quo AP software.

The platform offers automated invoice processing alongside customizable automated approval workflows so that invoices are routed to the right person at the right time. The platform also provides in-depth payment history with a comprehensive audit view of transactions.

Plooto subscriptions cost between $32 and $99 per month. It offers EFT and ACH payments at $0.50 per transaction and enables international payments to over 40 countries with no FX fees. However, payments can take between 4 to 5 days to process and customers report that payments often take far longer to go though. Limited customer support and a poor payee experience are also common issues with this platform. Plooto is purely an AP/AR solution and doesn’t handle employee spend or reimbursements.

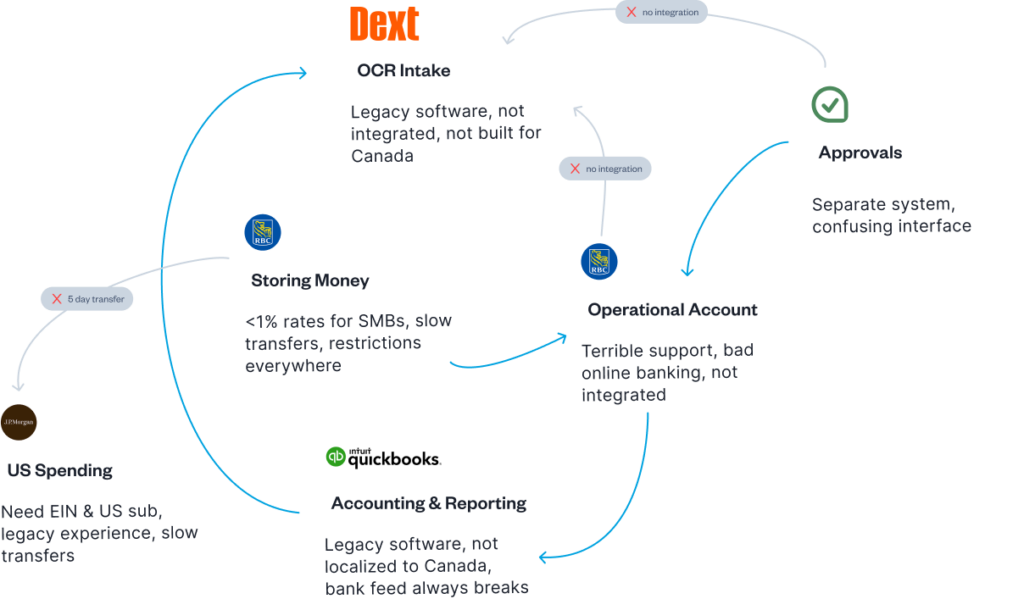

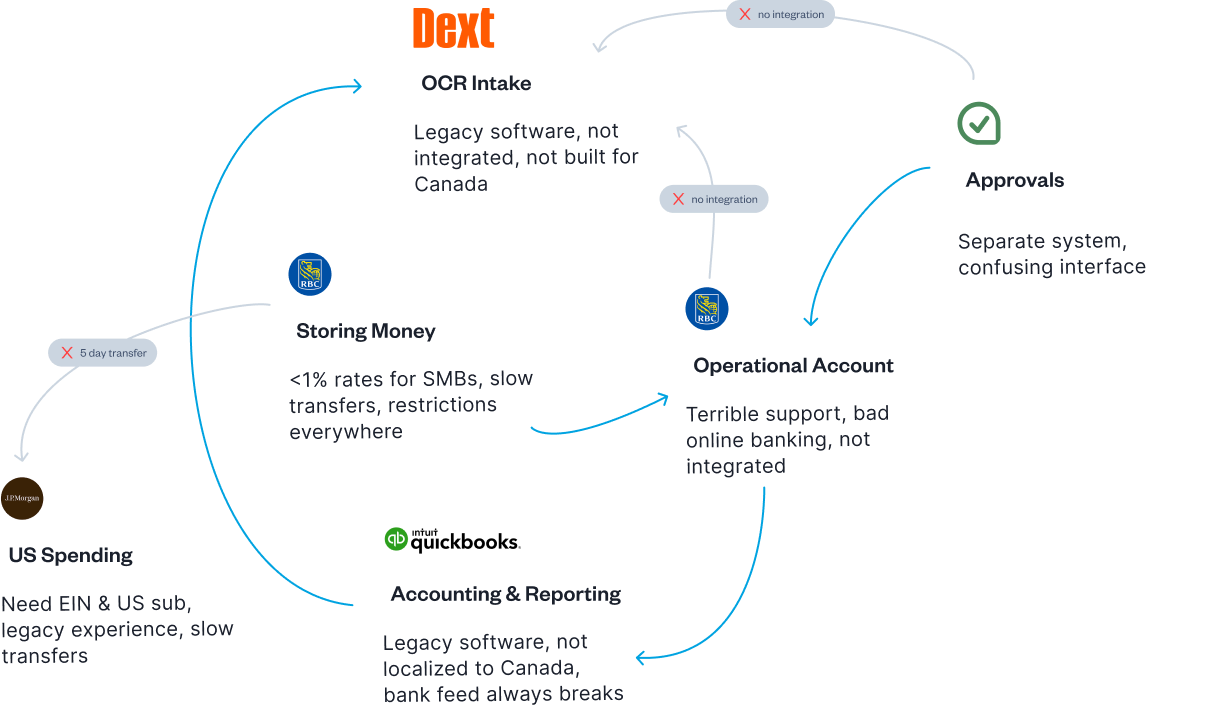

3. Dext

Dext is a bookkeeping automation software with a focus on record-keeping. Its strength is its OCR intake functionality. Dext provides multiple convenient ways for employees to upload receipts on the go with real-time expense tracking for the back office. Like Plooto, it offers robust approvals controls. It also provides automated reporting to help get the books closed quicker.

Currently, Dext doesn’t offer payment features. You’ll need to manually make payments through your bank or another platform. Dext may offer payment features in the future, but for now, it only provides a point solution that must be integrated with other platforms.

A Dext subscription costs between $30 and $107.50 per month.

4. Loop

Loop is a banking platform focused on streamlining cross-border payments. It’s built more like a digital banking app than an AP software solution. Loop delivers on flexibility and speed for making global payments, but it’s not the best choice for end-to-end AP automation. It doesn’t integrate with accounting software or automate invoice intake—you’ll need another solution for collecting and storing invoices. You’ll also have to manually validate and reconcile payments made through Loop with other systems.

Similar to Float, Loop does offer corporate credit cards in CAD and USD, as well as GBP and EUR with no annual fees, rewards points up to $1 million credit limits and a 55-day repayment grace period. The corporate card makes it easier to track and control employee spend alongside vendor payments for a more holistic view of your cash flow.

Loop has a free version, but its paid tiers cost between $49 and $199 per month. EFT/ACH payments cost between 0.25% and 0.5% per invoice plus $1, which means that the bigger the invoice, the more you’ll pay. Loop provides real-time payment tracking and payments typically arrive in 1 to 3 business days.

5. Quadient accounts payable automation by Beanworks

Primarily a mailing and customer experience solution provider, Quadient also offers a AP automation by Beanworks. Quadient might be a good option for larger, global mid-market businesses and enterprises, but it’s not flexible (or affordable) enough for SMBs. It offers comprehensive AP features like automated purchase order (PO) and invoice processing as well as automatic GL coding.

You can make payments through an integration with your online banking portal or via cheques, e-cheques, ACH or virtual credit cards which offer 1.1% cash back. Payments are automatically reconciled with your accounting software—Quadient offers custom integrations in addition to its long list of financial and enterprise resource planning (ERP) integrations.

There’s no publicly available pricing, but costs are tied to transaction volume, so it’s not ideal for rapidly growing companies.

6. RBC PayEdge

RBC PayEdge is an AP platform from RBC Royal Bank. It’s a good option if you want to make payments through the traditional banking system. The platform allows you to pay invoices from multiple Canadian bank accounts or credit cards and also offers EFT/ACH and cheque payments. You can also pay multiple vendors from a single payment order. RBC PayEdge offers tracking for global payments. Both domestic and international payments can take between 1 to 7 business days to arrive.

The platform doesn’t offer robust expense management features or reporting. As you might expect from a bank, the user interface is outdated and customers report that it’s not intuitive to use. It does integrate with accounting and ERP software.

RBC PayEdge has a free version, but its paid tiers cost between $89.95 and $219.95 per month (woof). EFT transactions cost $1 while ACH transactions cost a whopping $9.99, which means it’s not an ideal solution for businesses that need to make cross-border payments on a regular basis.

AI-powered invoice and receipt captureAutomated GL and tax codingCustom approval workflowsEmbedded EFT/ACH & wire payments (CAD, USD)Built-in FX servicesPayments in 1–2 business daysReal-time vendor trackingTwo-way sync with QuickBooks, Xero, Netsuite

Focus on incorporated businesses vs. freelancers or sole proprietorsBuilt for Canadian-based companies

Automated invoice processingEFT/ACH, cheque payments via credit cardNo FX fees.Payments (might) arrive in 4–5 business daysAR automation and payment processingTwo-way sync with QuickBooks, Xero, and Netsuite

Customers find that payments take far longer than 5 business daysLimited customer supportPoor payee user experience Doesn’t handle employee spend and reimbursements

Dext

SaaS: $30–$107.50/mo. EFT/ACH fees: N/A

Leading OCR receipt and invoice intakeMultiple ways to upload receiptsReal-time expense trackingRobust approvals controlsAutomated reportingQuickBooks, Xero, Sage, and other accounting software integrations

No payment functionalityDoesn’t handle employee spend and reimbursements

Global payments Multi-currency corporate credit cardsRobust approval controlsReal-time payment trackingPayments arrive in 1–3 business days

No invoice intake or storageNo accounting software integrationsPercentage-based pricing punishes growthNo cash backNo interest

Quadient accounts payable automation by Beanworks

No public pricing available. Pricing is based on monthly invoice volume and purchase order and payment requirements.

Automated PO, invoice processingAutomatic GL codingReal-time spend trackingRobust approvals controls1.1% cash back with virtual credit cardsTwo-way sync with QuickBooks, Xero, Sage and moreERP software integrations

Expensive and over-built for SMBsComplex user interfaceFrequent issues with integrationsTransaction volume-based pricing punishes growthDoesn’t handle employee spend and reimbursements

Pay out of multiple Canadian bank accounts or credit cardsSet approval controlsEFT/ACH, cheque payments via credit cardPay multiple vendors in a single payment orderTrackable global paymentsPayments arrive in 1–7 business daysQuickBooks Online, Sage, Xero, ERP software integrations

No robust expense management features No reporting featuresOutdated user interface Limited customer supportDoesn’t handle employee spend and reimbursements

Choosing the accounts payable automation software that’s right for your business

Migrating your AP processes to a new system is a major investment, so it’s important to choose software that’s easy to add into your existing workflows and is intuitive to use. Find a solution that can deliver tangible, measurable results—like reducing DPO and time saved closing the books—as well as intangible benefits like employee satisfaction. If you’re doing business across borders, select a solution that allows you to easily make EFT or ACH payments, wire transfers or no-fee FX payments in your required currencies.

The solution you choose should also address your business’s unique needs today while pushing your operations forward by boosting efficiency and reducing costs. Float’s Bill Pay provides accounts payable software small business owners and their accounting teams can use to manage employee spend and pay vendors for total control over AP. It’s designed by Canadians to support the nuances of Canadian accounts payable systems.

But don’t just take our word for it. Try Float for free and take the headache out of your accounts payable software processes, once and for all.

Make EFT Payments with Float

Canada’s best-in-class EFT, ACH, and Global Wires payments platform — plus average savings of 7%.

As a Canadian business owner, you understand the importance of managing your finances effectively, especially when it comes to cross-border transactions. Navigating the complexities of foreign exchange (FX) conversion can be a daunting task, but with the right strategies and tools, you can save money and optimize your financial operations.

In this article, we’ll dive into the world of FX conversion, focusing specifically on how to save on conversions between Canadian dollars (CAD) and United States dollars (USD). By the end of this guide, you’ll be equipped with the knowledge and strategies to make informed decisions and minimize costs associated with currency exchange.

What is FX Conversion?

FX conversion is the process of exchanging one currency for another, such as Canadian dollars (CAD) to United States dollars (USD). Understanding the foreign exchange process is crucial for businesses engaging in cross-border transactions.

How to Save on FX Conversion Between CAD and USD

Explore strategies to minimize costs: Researching and implementing effective strategies can significantly reduce the financial impact of currency exchange on your business.

Optimize transactions: By optimizing your cross-border transactions, you can minimize fees and maximize savings.

1. Understand Currency Conversion Fees

Familiarize yourself with typical fees: Banks and brokers often charge various fees for currency conversion. Understanding these fees is the first step in saving money.

Compare providers: By comparing different providers, you can identify those that offer the most competitive rates and save on conversion fees.

2. Seek Competitive Exchange Rates

Monitor the market: Keeping a close eye on exchange rates can help you identify favorable times to convert your currency.

Utilize rate comparison platforms: Platforms that offer real-time rate comparisons can help you find the best deals and save money on conversions.

3. Use Norbert’s Gambit for Large Transactions

Implement Norbert’s Gambit: This strategy involves buying dual-listed stocks to transfer between CAD and USD, effectively minimizing conversion costs.

Understand the steps: To execute Norbert’s Gambit effectively, it’s essential to familiarize yourself with the process and follow the steps carefully.

4. Consider a Corporate Card for USD Transactions

Use a corporate card for USD: A corporate card for USD transactions can help minimize conversion fees for business expenses.

Benefits of a specialized corporate card: Corporate cards designed for cross-border transactions often offer competitive rates and additional features to streamline your financial operations.

Tips on Reducing FX Costs

1. Plan Transactions Strategically

Timing is crucial: By planning your conversions when exchange rates are favorable, you can maximize savings and minimize costs.

2. Utilize Financial Tools

Leverage financial software: Specialized financial software can help you track and optimize your currency exchanges, ensuring you’re always getting the best rates.

Frequently Asked Questions

What is the cheapest way to convert CAD to USD?

Use cost-effective methods: Strategies like Norbert’s Gambit or platforms with low conversion fees can be the most cost-effective ways to convert CAD to USD.

How can I avoid high fees when converting currency?

Compare and use specific strategies: Comparing providers and using strategies like Norbert’s Gambit for large sums can help you avoid high conversion fees.

What are the best strategies for saving on FX conversion?

Monitor, use corporate cards, and apply Norbert’s Gambit: By monitoring exchange rates, using corporate cards designed for cross-border transactions, and applying Norbert’s Gambit when appropriate, you can effectively save on FX conversion.

How does Norbert’s Gambit work for CAD to USD conversion?

Buy dual-listed stocks and journal them: Norbert’s Gambit involves buying dual-listed stocks and journaling them to exchange currencies at minimal cost.

Conclusion

By implementing these strategies and staying informed about the latest trends in FX conversion, you can significantly reduce costs and optimize your cross-border transactions. At Float, we understand the unique challenges faced by Canadian businesses, and we’re here to help you navigate the complexities of foreign exchange. Get started for free today and discover how our innovative solutions can help you save on FX conversion between CAD and USD.

Managing business expenses can quickly become chaotic without the right systems. From vendor invoices to employee reimbursements, keeping track of payments is a critical part of maintaining healthy cash flow.

This is where accounts payable (AP) comes in—the core of your company’s financial operations. But traditional AP processes are often slow, error-prone and a major headache for finance teams. So, how can you streamline your AP process and free up time for what really matters?

In this guide, we’ll break down everything you need to know about accounts payable: what it is, how it works and how modern automation tools like Float can transform your AP workflow. Whether you’re a finance leader aiming to eliminate gruntwork or a business owner seeking better visibility into company spending, we’ve got you covered.

What is Accounts Payable (AP)?

Accounts payable (AP) refers to the money a company owes to its vendors for goods or services received but not yet paid for. It’s recorded as a liability on the balance sheet and includes payments such as supplier invoices, contractor fees and utility bills.

Examples of accounts payable:

Invoices for supplies and equipment (e.g. office supplies, computer hardware, raw materials, etc.)

The way your business manages accounts payable can make or break its cash flow, vendor relationships and bottom line. In fact, 65% of SMBs report long processing times for financial transactions, which ties directly to cash flow problems and missed opportunities for growth.

Imagine a missed invoice leads to a late fee and a frustrated vendor who pauses your deliveries. Or maybe your finance team is scrambling to fix a double payment, wasting hours chasing down refunds. Meanwhile, slow approvals stall an important purchase, putting a critical project on hold. There are just a few ways inefficient AP processes can cost you time, money and trust.

Accounts payable vs. accounts receivable

While accounts payable tracks what your business owes, accounts receivable (AR) tracks what others owe you. AP is a liability, whereas AR is an asset. Both are important for understanding cash flow and maintaining financial stability.

Tracking both AP and AR is key to maintaining a healthy cash flow—see how cash flow statements tie it all together.

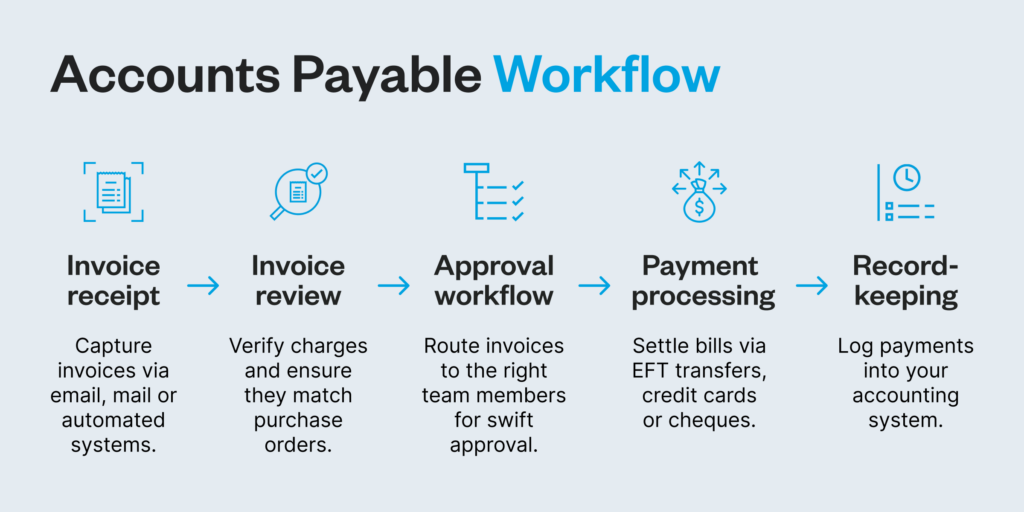

What is the accounts payable process?

Accounts payable management involves outlining the journey from invoice to payment, offering a clear framework for how to pay an invoice efficiently and accurately.

Here’s how it typically flows:

Invoice receipt: Capture invoices via email, mail or automated systems.

Invoice review: Verify charges and ensure they match purchase orders.

Approval workflow: Route invoices to the right team members for swift approval.

Payment processing: Settle bills via EFT transfers, credit cards, or cheques.

Record-keeping: Log payments into your accounting system.

When your AP process runs smoothly, payments are on time, vendors stay happy and your cash flow stays clear.

6 common challenges in traditional AP management

Traditional accounts payable processes can feel like a time sink—slowing operations, frustrating finance teams, and leaving room for costly mistakes. Without modern tools, businesses face a range of issues that can quickly snowball into bigger problems.

1. Manual workflows

First, there’s the chaos of manual workflows. Paper invoices, spreadsheets and email chains create confusion, waste time and make it easy for documents to slip through the cracks. Finance teams end up chasing receipts instead of focusing on strategic work.

2. Approval bottlenecks

Then come the approval bottlenecks. Payments stall when they’re stuck in endless sign-off loops. The longer the delay, the greater the risk of late fees—or worse, strained vendor relationships.

3. Frequent errors

On top of that, errors run rampant with manual processes. It’s easy to enter the wrong numbers, pay the same invoice twice or miss a payment altogether.

4. Poor visibility

There’s also the issue of poor visibility into spending. Without a centralized view, finance teams are left in the dark, scrambling to piece together where money is going and struggling to catch unwanted expenses in real time.

5. Decentralized tools

Compounding these problems is that many businesses still rely on disconnected tools to manage the AP process—55% of SMBs say financial tools that don’t integrate well with each other are a top inefficiency driver. Often, this looks like using one system for bill intake, another for approvals, an accounting platform to track unpaid bills and a separate bank portal to process payments.

When integrations between tools break, it causes delays and wastes time on troubleshooting. Even if you’re processing high volumes of payments every month, this patchwork approach can waste time rather than save it.

6. Fraud

What’s worse, all of these challenges compound to increase your fraud risk. Loose controls and outdated systems can leave the door open for unauthorized payments or fake invoices to slip through unnoticed, costing your business money and damaging trust.

When these challenges pile up, they can have real-world consequences. But with a modern, automated accounts payable process, you can gain the visibility and control you need to make payments simpler.

Confident SMBs are 2x as likely to expect >10% profit growth

Benefits of automating accounts payable management

From speeding up payments to improving visibility, accounting automation helps your business move faster, smarter, and more securely.

Here’s how:

Faster invoice processing Manual invoice processing is slow and clunky, often dragging payments out for days or even weeks. Automation can capture invoice data instantly and route approvals with a click. Payments that once took days can be completed in minutes, keeping your vendors happy and your operations running smoothly.

Reduced errors and fraud risk Manual data entry is a breeding ground for costly mistakes: duplicate payments, missed invoices and misfiled records. Automated accounts payable systems use built-in validations to catch errors before they happen, reducing the risk of costly slip-ups. With proper controls and approval workflows in place, you’ll minimize the chance of fraudulent activity or unauthorized spending.

Improved cash flow management With automation, you get real-time insights into every outgoing payment—what’s due, what’s paid and what’s pending. Clear visibility into your liabilities helps you forecast expenses, avoid late fees and take advantage of early payment discounts.

Increased visibility and control No more chasing down receipts or wondering where an invoice stands. Automation centralizes your AP data into one dashboard, giving you a complete, real-time view of every transaction. You can track approvals, spot spending patterns and enforce policies, all without digging through email threads or spreadsheets.

Modern accounts payable strategies

Focus on these accounts payable strategies to reduce delays, eliminate errors, and gain better control over your AP processes.

1. Automate invoice processing

Manual data entry is a productivity killer that leads to errors and slows down your entire AP workflow. Automating invoice processing is one of the fastest ways to make your AP process more efficient and accurate.

Here’s how to do it right:

Digitize invoices with OCR technology. Optical character recognition (OCR) technology scans and converts paper invoices into digital records. This eliminates manual data entry, reduces errors, and speeds up processing—especially if you’re dealing with high volumes of invoices.

Automate invoice-to-PO matching. Set up rules to automatically match invoices to purchase orders (POs). With automated matching, any discrepancies like price differences or unexpected charges are flagged for review. This helps catch errors early and prevents overpayments.

Schedule recurring payments. For vendors with regular billing cycles, such as utilities or monthly service providers, automate recurring payments. This ensures that predictable bills are paid on time without the risk of missed deadlines or late fees.

2. Optimize approval workflows

Bottlenecks in the approval process slow down payments, frustrate vendors, and create unnecessary delays. Streamlining your approval workflows keeps payments moving and eliminates confusion.

Here’s how to do it:

Establish clear approval hierarchies. Define who needs to approve invoices based on payment amounts, vendor types, or departments. With clear guidelines, everyone knows their role, and invoices don’t get stuck waiting for the right sign-off.

Set spending limits for team members. Create thresholds for automatic approvals to reduce unnecessary reviews. For example, purchases under $250 can be pre-approved, while anything above requires manager review. This keeps small expenses moving without bottlenecks.

Route approvals digitally. Use an automated system to assign invoices to the right approvers, notify them instantly, and track every step of the process. Real-time updates and digital records eliminate back-and-forth emails and make it easy to follow the status of each invoice.

3. Transition to electronic payments

Paper cheques are slow, costly and prone to error. Switching to electronic payment methods speeds up your accounts payable process and reduces administrative headaches.

Here’s how to make the shift:

Prioritize virtual cards for all online payments. Virtual cards are single-use or limited-use payment numbers tied to your corporate account. They’re easy to track, help prevent fraud and are perfect for one-off payments or online purchases (especially software trials). Many vendors prefer virtual cards because they process instantly and don’t require banking details.

Use electronic transfers for domestic payments. For all other domestic transactions,EFT (Electronic Funds Transfer) payments are faster, more secure and often cheaper than traditional cheques in Canada. An EFT payment is ideal for recurring payments and bulk transfers, cutting out mailing delays and lowering processing costs.

💡 Pro tip: Understand the difference between ACH vs EFT. Automated clearing house payment (ACH) is a specific type of EFT used primarily for domestic payments within the US. Some more modern providers do offer cross-border ACH payments, but you’ll need to check with your bank. Or, try making international payments with Float.

New to digital payments? Start by learning how to make an EFT payment, from setting up vendors to scheduling transfers.

Looking to pay invoices from Canada to other countries?

While this may seem overwhelming at first, modern tools have come a long way. Solutions (like Float) will allow you to implement all of these strategies in one place.

Accounts Payable Metrics to Track

Days Payable Outstanding (DPO): measures the average time it takes to pay vendors

Invoice processing time: tracks the efficiency of the AP process from invoice receipt to payment

Early payment discount capture rate: shows the percentage of available discounts captured

Electronic invoice adoption rate: indicates the level of automation in the AP process

Vendor satisfaction score: assesses the strength of vendor relationships based on timely payments and communication

Tips for choosing the right accounts payable software

Start with automation. Capabilities like invoice capture and approval workflows will save your team time and reduce errors. Look for features like OCR technology to digitize invoices and automatic matching to purchase orders to streamline your process.

Next, prioritize integration. Your software should connect seamlessly with your accounting system, keeping your records accurate without extra manual work.

Visibility matters, too. Real-time dashboards and easy-to-read reports help you track spending, catch errors and make smarter financial decisions.

Don’t forget security. Built-in safeguards like multi-factor authentication and role-based permissions protect your payments from fraud and unauthorized access.

Last, choose software that grows with you. Look for a solution that can handle increasing transaction volumes, add users easily and adapt to your changing needs, all while offering responsive support.

Why Float fits the bill

Float offers fast automation, real-time insights and secure, seamless integrations—everything you need to manage your accounts payable process without the headaches. With built-in tools like bill pay to automate invoice payments, you can process transactions faster and reduce manual work. Plus, it’s built to scale with your business, supporting your growth every step of the way.

Simplify business spending with Float’s smart AP & corporate cards

“Float’s Bill Pay has become our main AP solution for Canadian business expenses. They built a product that is better than anything else on the market in Canada.”

Thomas Kwon Head of Finance & Operations

Accounts payable management doesn’t have to be complicated or costly. Float brings everything you need into one easy-to-use platform, helping you automate your AP workflows, track spending in real time, and process payments faster—all while keeping complete control over your finances.

With Float, you get a smarter way to manage every dollar your business spends.

Issue corporate cards instantly

Automate bill payments from one place

Close your books up to 8x faster with seamless accounting integrations

Earn 4% interest on your Float balance

Get 1% cashback on card spend

Float is trusted by thousands of Canadian businesses to simplify their spending, from approvals to payments—all with no hidden fees and fast, friendly support when you need it. Whether you’re eliminating approval bottlenecks or gaining better control over your cash flow, Float helps your business spend smarter and scale faster.

Ready to take control of your business spending?

Get started with Float today and experience faster payments, fewer errors, and complete visibility.

Try Float for free

Business finance tools and software made by Canadians, for Canadian Businesses.

Rising costs at gas pumps nationwide can make operating vehicles in your business both challenging and expensive. In addition to maintenance, fuel accounts for a major portion of operational spend for companies that use vehicles to provide services. The good news? Finding the best fuel card or fleet card for your business can save you money and give you control over the cost of getting from A to B.

In this guide, we’ll go over how businesses benefit from providing fleet cards to employees and introduce some of the best fleet fuel cards Canada has on offer—plus a few alternatives.

What is a fleet card?

Fleet cards, also known as fuel cards, enable employees to pay for the costs associated with operating a vehicle—including gas, maintenance and repairs—and forward the charge to their company as a business expense. Fleet cards can only be used for vehicle-related expenses, whereas other corporate cards can be used for purchases like office supplies, software subscriptions, or meals.

Fleet cards are for businesses of all sizes with employees who drive a vehicle as part of their job. This includes companies that manage field workers or contractors who commute to different job sites (think plumbers, landscapers and telecommunications techs). Fleet cards are a must for long-haul trucking and last-mile delivery companies that need a way for drivers to pay for fuel and maintenance while they’re on the road.

How does a fleet card work?

If you’re looking into business cards, you might be wondering: What is a fleet card used for? Can’t a corporate card do the same thing?

There are definitely similarities. Employees can use fleet cards to make fuel and vehicle maintenance purchases on the company’s tab the same way they’d pay with a company debit or credit card. Many fleet cards are a type of credit card or charge card that accumulate a balance the employer needs to pay down on a regular basis. Some providers, like Float, also offer prepaid business credit cards for fuel.

Unlike general-use business credit cards, fleet cards enable employers to set strict spending limits and restrict the types of transactions employees make—and even where they can make them.

There are two types of fleet cards:

Closed-loop fleet cards are offered by fuel retailers and can only be used within their fuel networks. One of the major downsides is that drivers have to go out of their way to use them at specific gas stations and truck stops.

Open-loop fleet cards are offered by financial institutions or corporate card providers and can be used anywhere the card’s brand is accepted. Open-loop cards are often Visas or Mastercards.

You can assign a fleet card to an employee or to a vehicle, which makes it easier to track total cost of ownership (TCO) and identify any gas-guzzling lemons in your fleet. The cards also offer security features like flagging unauthorized transactions and allowing you to suspend or cancel non-compliant cards.

Benefits of fleet cards

1) Eliminate the reimbursement rigamarole

With a fleet card, employees don’t have to worry about gathering receipts to submit for approval or wait for reimbursement. In turn, your accounting team doesn’t have to spend time hunting down receipts or juggling payouts, making it easier to control cash flow.

2) Give drivers autonomy without compromising on control

Using a fleet card keeps the budget under control without causing roadblocks for drivers. Fleet cards give you the best of both worlds: the ability to set spend limits and track usage while also allowing your team to fuel up when it’s convenient for them.

3) Get better insights and analytics

Top-performing fleet cards can be integrated with bookkeeping or expense management software to automatically log details like fuel grade, fuel price, and location. This enables you to measure fuel efficiency and maintenance costs so you can spot opportunities for improvement.

4) Take advantage of savings and rewards

Many closed-loop fleet cards offer rebates or discounts on fuel, car washes, tires and mechanic services. Some also offer cash back or points programs. At Float, our corporate cards offer a stack of rewards including 1% cashback and 4% interest on yield account balances—without the restrictions that come with closed-loop cards.

Best fleet fuel cards in Canada

The best fuel card will offer employees flexibility and convenience when they need to fuel up while giving you greater visibility and control around your vehicle expenses. If your employees are driving out-of-province or into the U.S., you need to consider cards that work across borders.

To help you find the card that fits your business, here’s an overview of some of the best fleet fuel cards Canada has to offer:

Closed-loop fleet cards

Shell Fleet Plus: One of the leading fuel cards for trucking companies in Canada. Offers discounts at Shell stations and Jiffy Lube, plus Air Miles. Includes purchase controls and reporting.

Esso and Mobil Business Card and Premier Plus Business Card: Another leader with a wide network offering fuel cards for trucking companies in Canada. Provides volume discounts and, at the Premier Plus level, advanced performance reporting.

Co-op Fleet Cards: A popular option for transport and agriculture companies. Can only be used at Co-op, Tempo and Western Nations Gas Bars in Western Canada.

Open-loop fleet cards

Shell Fleet Navigator: An open-loop Mastercard that has all the benefits of Shell Fleet Plus along with additional chip and PIN security and universal acceptance.

BMO Fleet Card: BMO offers the Mastercard Corporate Fleet Card that can be used everywhere, including Mastercard ATMs. Offers spend controls and reporting.

Foss National Leasing Fuel Card: This open-loop-ish card is accepted at 98% of Canadian fuel retailers. The program includes tire services from Foss, which also offers vehicle leasing.

Corporate cards for vehicle expenses from modern business finance providers

Float: Flexible open-loop corporate card solutions, including fuel cards for small businesses in Canada. Provides built-in expense management and spend limit features and offers 7% total average savings. Built for Canadian businesses.

Keep: General-use corporate card with higher credit limits. Offers basic spend controls and expense tracking. Not available in Québec.

Loop: General-use corporate card with no FX fees. Offers points rewards on purchases. Expense management through a single pane of glass.

Vault: General-use corporate cards that offer 1% cashback on purchases and no FX. Provides multi-currency accounts. Not available in Québec.

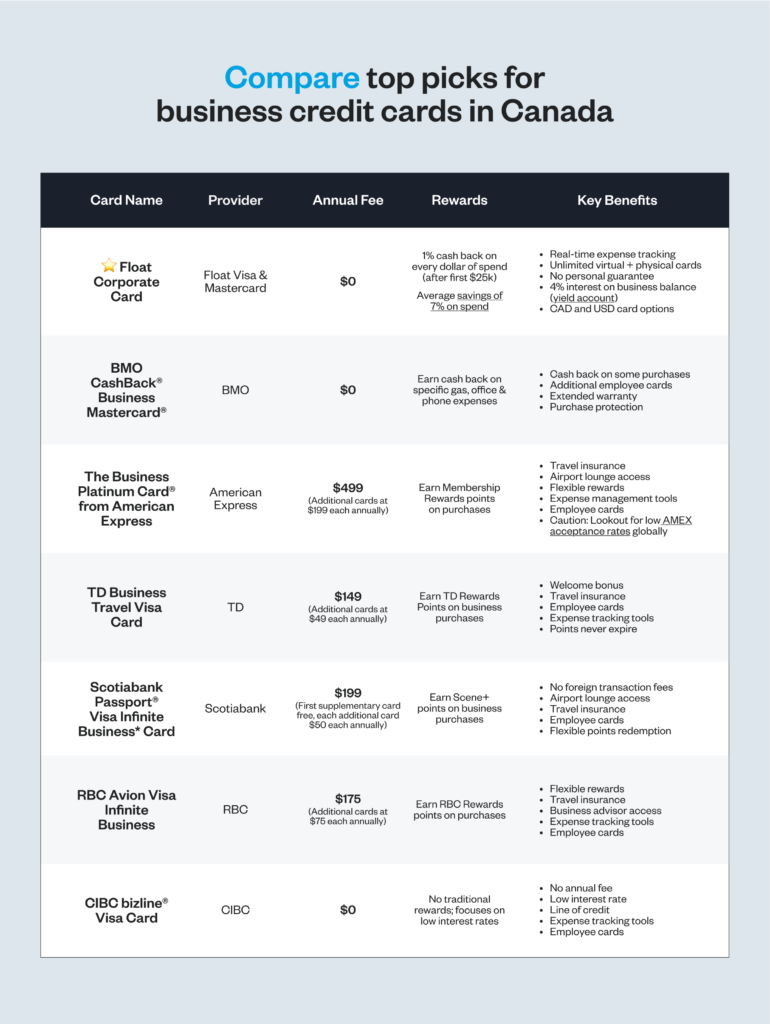

Best business credit cards

Compare top options, fees and benefits for Canadian companies.

Fuel cards should give you tools to track fuel efficiency and maintenance costs to better understand TCO so you can invest wisely in new vehicles moving forward.

Fleet cards that integrate seamlessly with your tax and accounting or business intelligence software make it easy to stay compliant and measure success.

The best fuel cards for trucking companies in Canada offer expense management solutions that integrate with telematics and electronic logging device (ELD) software for a holistic view of vehicle costs.

Bear in mind that some cards require you to buy a certain volume of fuel each month to qualify for benefits like discounts and rebates. If fuel purchases aren’t a major cost for your business, choosing a general-use corporate card allows you to have the same level of control over employee purchasing, without limitations around what types of expenses they can pay for with their card.

How to apply for fleet cards

Unlike business credit cards, many fleet cards on the market are provided by fuel retailers or corporate card providers, not traditional financial institutions. If you’ve looked into how to get a business credit card before, you might be wondering, what is a fleet card application process like?

You’re in luck. Applying for a fleet card is typically quick and easy. Here’s how.

1) Get your business info together

Applications require information like your company name, location, type, industry, registration documents and your GST/HST number.

2) Gather fleet information

You’ll need to report details like the size of your fleet, your monthly fuel and maintenance costs and your monthly fuel use.

3) Gather financial documents and check your credit score

Some providers may need to look at financial statements, proof of income and your credit score to determine the credit limits you’re eligible for. Some also require a personal guarantee or other collateral.

4) Complete your application

Many closed-loop cards and cards that are available through banks require you to speak directly to a representative about your needs. Open-loop cards, especially those offered by fintechs, typically have fast online application processes. At Float, it takes just 10 minutes to apply for your corporate cards.

5) Get approved and issue your cards

With Float, you can get a 24-hour turnaround on approval. Some providers have longer approval timelines. Once you’ve been approved, you can put rubber to the road and start assigning cards to your drivers.

Managing fuel expenses in your business

According to the American Transport Research Institute (ATRI), fuel accounts for almost a quarter of trucking company operating expenses and costs an average of $22.23 USD per hour, per vehicle in 2023.

Saving on fuel frees up cash in your business. Reducing fuel costs also goes hand-in-hand with lower emissions, which can help you meet climate action targets.

Here’s how you can control your fuel costs in addition to using a fleet card.

Optimize routes and loads

Use telematics solutions to find faster routes and enable drivers to proactively navigate around traffic and construction. Ensure your drivers are only carrying what’s required—i.e., don’t let employees lug their hockey bags around in the company car—as fuel consumption increases by about 1% for every 25 kg in mid-sized cars.

Habits like repeatedly hitting the breaks and speeding up can increase fuel use by up to 33%. Coasting rather than using the accelerator and brakes can also save gas. Proactively coach drivers on techniques to reduce fuel use and minimize wear-and-tear on your vehicles.

Perform preventative maintenance

Replacing air filters, changing oil, and checking tire pressure on a regular basis boosts fuel efficiency and ensures your fleet is in good working order. This reduces unnecessary emergency repair expenses.

Float for fleet management

Fuel cards are great for trucking companies or last-mile delivery companies whose drivers mostly spend money at fuel stations, truck stops, and mechanics. But if you run a trades- or service-based company, and/or provide commuter vehicles for your employees, the best fuel card for you might be a general use corporate card.

Float offers the best business credit card in Canada. Our flexible corporate cards enable you to manage all of your employee expenses, including fleet costs like fuel and maintenance, in one place. Drivers can use Float cards wherever Visa and Mastercard are accepted across Canada.

With Float, you can set the same strict spending limits that you’d expect from the best fleet fuel cards in Canada and customize those restrictions—in real time—for all the purchases your employees need to make. Float’s suite of powerful reporting features show transactions as they happen in the moment and enable you to track budgets vs. actuals over time.

Float also offers high spending limits up to $1M with no personal guarantees. Benefits like 1% cash back, 4% interest on funds kept in your Float and low USD conversion fees rolled up with increased efficiency across your team delivers 7% total cost savings.

Looking to sharpen your bookkeeping skills without breaking the bank? We’ve rounded up 5 free online bookkeeping courses online that’ll help Canadian small businesses owners and finance teams.

Why Bother with Courses on Bookkeeping?

Let’s face it, training in bookkeeping isn’t the most thrilling part of running a business. But it’s crucial for:

Keeping your financial records in order

Making tax time less of a headache

Understanding your company’s financial health

Making smarter business decisions

So, let’s dive into these free online bookkeeping courses that’ll transform you from a numbers novice to a balance sheet boss!

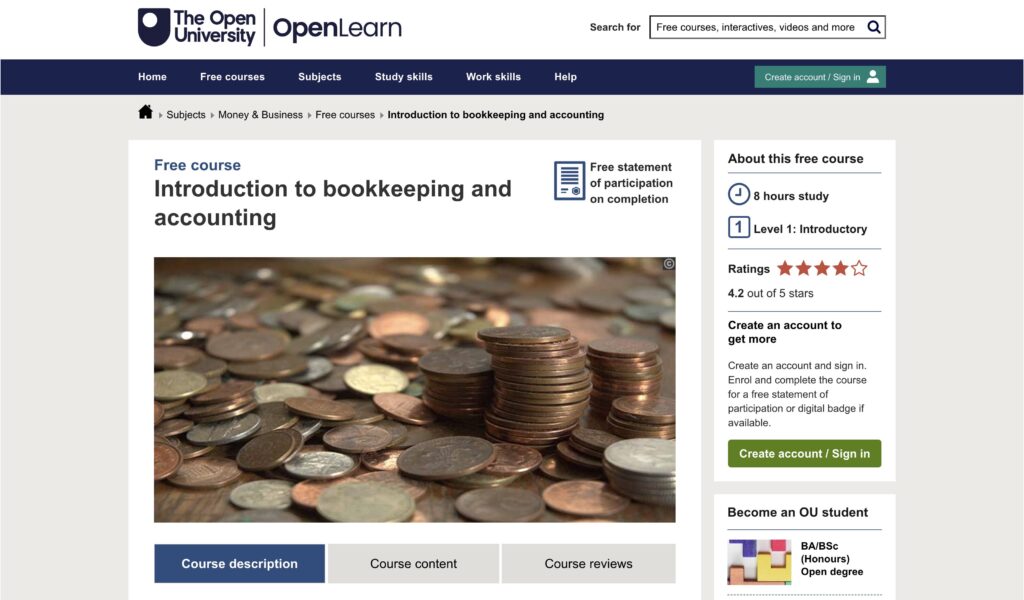

Are you keen to grasp the essentials of bookkeeping and online accounting? The Open University offers a fantastic free online bookkeeping course that’ll set you on the path to financial wizardry.

Introduction to Bookkeeping and Accounting is a gem for anyone looking to:

Master the numerical skills crucial for bookkeeping

Understand the accounting equation and double-entry bookkeeping

Learn how to record transactions like a pro

Create balance sheets and profit & loss accounts

This course is completely free and self-paced. You can learn at your own speed, fitting it around your own schedule.

What’s included:

8 hours of study material

Beginner level content

A free statement of participation upon completion

Option to earn a digital badge

Whether you’re a small business owner wanting to get a handle on your finances, or you’re considering a career change into accounting, this course provides a solid foundation.

Head over to The Open University’s website and create your free account. Your journey into the world of bookkeeping starts now!

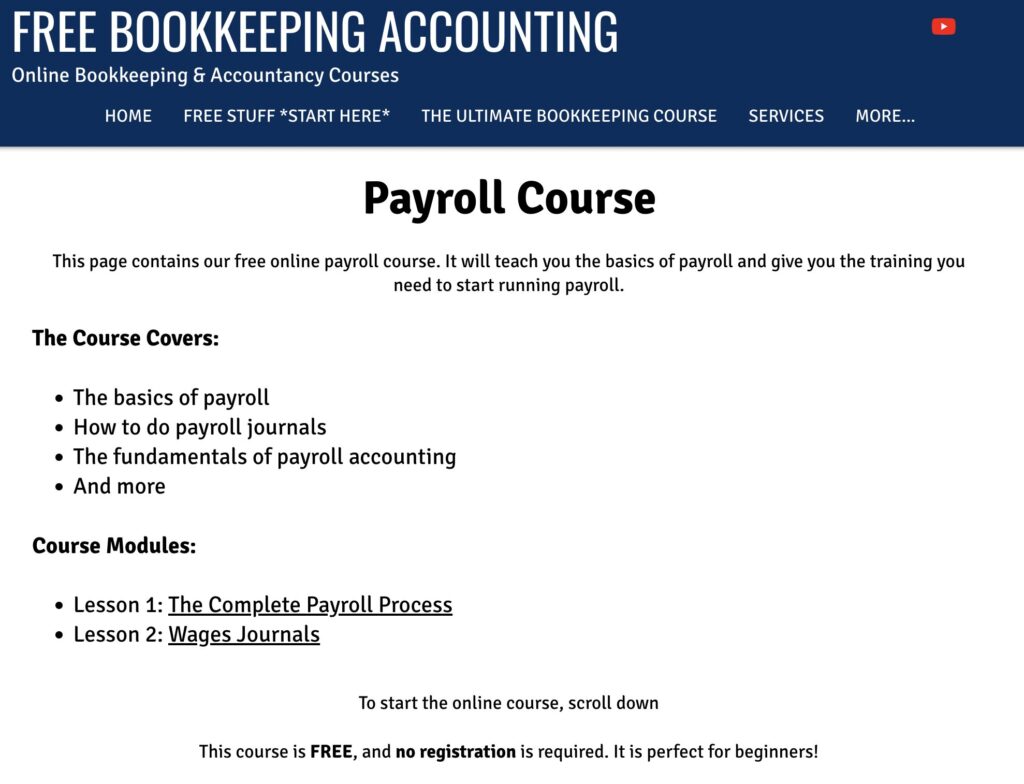

Are you a small business owner or aspiring bookkeeper looking to get a handle on payroll accounting? Look no further! FreeBookkeepingAccounting.com offers a fantastic free online payroll course that’ll have you crunching numbers like a pro in no time.

This course covers all the essentials:

The complete payroll process

Understanding wages journals

Fundamentals of payroll accounting

And much more!

No registration required – simply scroll down and start learning at your own pace. Perfect for beginners, this course breaks down complex concepts into bite-sized, easy-to-digest modules.

Key topics include:

Decoding payslips and key payroll terms

The five main steps of the payroll process

Creating and understanding wages journals

Accounting for deductions and employer costs

Whether you’re looking to handle payroll for your own business or kickstart a career in bookkeeping, this free course is an excellent starting point. It’s packed with practical knowledge, clear explanations, and even includes visuals to illustrate key concepts.

ACCA (Association of Chartered Certified Accountants) is a globally respected body for professional accountants. They’re offering a treasure trove of knowledge to help you level up your career.

Here’s what’s on offer:

Dive into the world of Machine Learning for Finance

Master the basics with Financial Accounting and Management Accounting courses

Get tech-savvy with Robotic Process Automation and Cybersecurity for finance pros

Build a solid foundation with Intro to Bookkeeping and Management Accounting

The best part? These courses are completely free to audit, with the option to earn a verified bookkeeping certificate for a small fee if you want to showcase your new skills.

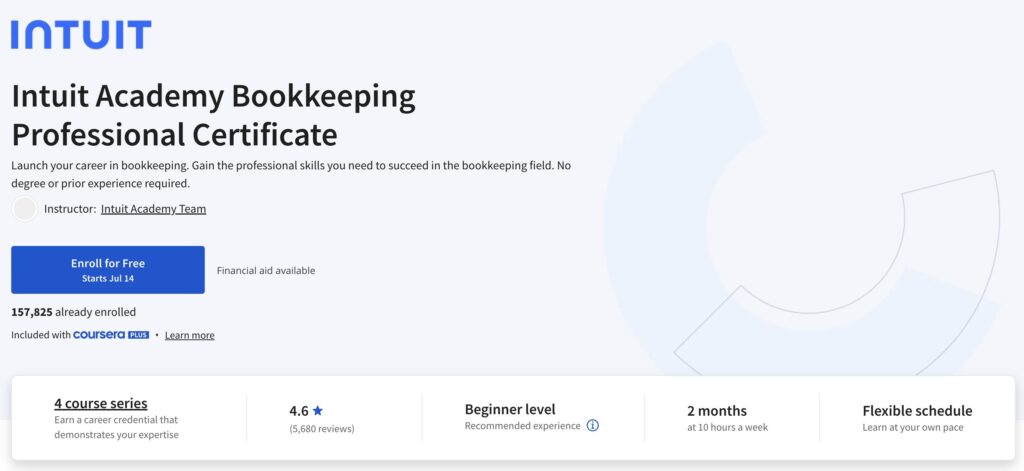

Are you looking to dive into the world of bookkeeping or level up your financial skills? Look no further than the Intuit Academy Bookkeeping Online Professional Certificate offered on Coursera! This comprehensive program is designed for beginners and career-changers alike.

Here’s why it’s worth your time:

No prior experience needed – start from scratch and build a solid foundation

Learn from industry experts at Intuit

Flexible, self-paced learning – complete in about 2 months at 10 hours per week

Earn a respected credential to showcase on your LinkedIn profile and resume

What You’ll Learn:

Essential bookkeeping concepts and accounting principles

Navigating the accounting cycle to produce financial statements

Analyzing financial data to make smart business decisions

Hands-on practice with real-world scenarios

While this course isn’t free, you can always apply for financial aid with Coursera. This bookkeeping program is included with a Coursera Plus subscription, making it an incredibly cost-effective way to invest in your future.

FAQ: Your Burning Bookkeeping Questions Answered

Q: Do I need any prior experience to take these courses? A: Most of these courses are designed for beginners, but check the individual descriptions for any prerequisites.

Q: Will I receive a certificate upon successful completion? A: Yes, some of these courses offer fairly sophisticated bookkeeping training and offer certificates upon program completion.

Q: Can I access course materials after completion? A: This varies by course. Some may offer ongoing access, while others might have time limits.

Q: Are these courses recognized by professional bookkeeping organizations? A: These free courses are great for personal development, but may not count towards official certifications. Check with professional bodies for accredited programs.

Q: How much time should I dedicate to these courses? A: Most courses suggest 3-5 hours per week, but the beauty of bookkeeping training online is its flexibility!

Ready to Balance Those Books?

Whether you’re a small business owner looking to get a handle on your finances or an aspiring professional bookkeeper, these free online bookkeeping courses offer a fantastic starting point. Remember, good bookkeeping is the foundation of a healthy business – so why not invest some time in building those skills?

From mastering the basics of the accounting cycle to tackling complex financial analysis, there’s a course here for everyone. So, grab a cup of coffee, fire up your computer, and get ready to dive into the world of debits, credits, and balance sheets. Your future financially-savvy self will thank you!

Are you drowning in receipts and invoices? Losing sleep over GST/HST deadlines? You’re not alone. Many Canadian small business owners find themselves in the same boat when managing their finances.

Why Bother with Professional Bookkeeping?

Let’s face it: you didn’t start your business to become an accountant. You’ve got bigger fish to fry. That’s where bookkeeping services come in handy.

The Perks of Outsourcing Your Books

More time to focus on what you do best

Accurate financial records

Insights to help your business grow

Reduced risk of costly errors

Stay compliant with CRA regulations

Finding the Right Fit: Bookkeeping Services for Canadian Small Businesses

Not all bookkeeping firms are created equal. Here’s what to look for:

Experience with Canadian small businesses: They should understand your unique challenges and tax obligations

Tech-savvy approach: Online bookkeeping services can save you time and money

Clear communication: No jargon, just direct communication about your finances

Scalable solutions: As your business grows, your bookkeeping needs will too

Knowledge of Canadian tax laws: Including GST/HST, provincial taxes, and corporate tax regulations

Online Accounting and Bookkeeping Services: The Future is Now

Cloud accounting services are changing the game for Canadian small businesses. Here’s why:

Real-time access: Check your numbers anytime, anywhere

Collaboration made easy: Work seamlessly with your accountant

Automatic updates: Always have the latest features at your fingertips

Bank-level security: Keep your financial data safe and sound

Multi-currency support: Essential for businesses dealing with US or international clients

Note that while online bookeeping services could offer lower costs, they usually work best for simple business models. If your business has a unique revenue model, complex vendor relationships or P&L structure, it might be best to work with a human who can cater to your business needs.

What to Ask when Choosing a Bookkeeping Company?

What services do you offer?

How do you handle communication?

What’s your experience with businesses in my industry?

Can you provide references from other Canadian businesses?

What software do they use and is it compatible with the CRA requirements?

How do you stay updated with Canadian tax laws and regulations?

Which accounting systems do you work with?

How Much Should You Spend on a Bookkeeper?

How much should you shell out for bookkeeping services in Canada? Well, it’s not a one-size-fits-all answer.

Bookkeeping costs can vary widely based on:

The size of your business

The complexity of your finances

The services you need

Whether you opt for in-house, freelance, or online bookkeeping services

Here’s a rough guide:

For small businesses, expect to pay anywhere from $300 to $2,000 per month.

Freelance bookkeepers might charge $30 to $90 per hour.

Online bookkeeping services often offer tiered pricing, starting from as low as $200 per month for basic services.

Remember, cheaper isn’t always better. A skilled bookkeeper can save you money in the long run by catching errors, maximizing tax deductions, and providing valuable financial insights.

Consider this: How much would it cost you to do it yourself? Factor in your time, potential mistakes, and the stress of dealing with the CRA. Suddenly, professional bookkeeping services start to look like a bargain!

Professional tip: Many Canadian bookkeepers offer a free consultation. Use this to discuss your needs and get a customized quote. It’s a great way to find a service that fits your budget and your business.

The Cost of Peace of Mind

Investing in bookkeeping and accounting services for Canadian small businesses might seem like a significant expense. But consider this: how much your time is worth, and what’s the cost of a major financial mistake or CRA penalty?

Online bookkeeping services in Canada often offer flexible pricing models to suit businesses of all sizes. From basic bookkeeping to full-service accounting, there’s an option for every budget.

Beyond the Books: How a Bookkeeper Can Boost Your Business

A good bookkeeper doesn’t help you reconcile your bank statements. They can be your financial advisor, offering insights to help your business thrive in the Canadian market.

Cash flow forecasting: Plan for the future with confidence

Budget creation and monitoring: Keep your spending in check

Financial reporting: Understand your business’s health at a glance

Tax planning: Minimize your tax bill

GST/HST management: Stay on top of your collections and remittances

Payroll services: Navigate the complexities of Canadian payroll taxes and deductions

FAQs: Your Burning Questions Answered

Q: How often should I update my books? A: Ideally, daily or weekly. But realistically, as long as you’re consistent, monthly updates can work too. Just ensure you’re prepared for quarterly GST/HST filings if applicable.

Q: Can online bookkeeping services handle Canadian payroll? A: Many do! It’s worth asking about when you’re shopping around. Make sure they’re familiar with CPP, EI, and provincial payroll tax requirements.

Q: I do business in multiple provinces. Can online bookkeeping services handle this? A: Many Canadian online bookkeeping services are equipped to handle inter-provincial business operations, including varying tax rates and regulations.

Q: How secure is cloud accounting for Canadian businesses? A: Reputable cloud accounting services use bank-level encryption to keep your data safe. Many also ensure your data is stored on Canadian servers to comply with privacy laws.

Q: What’s the difference between a bookkeeper and an accountant in Canada? A: Bookkeepers handle day-to-day transactions, while accountants focus on the bigger financial picture and complex tax matters. Many small businesses in Canada need both!

Q: Can a bookkeeper help me with my T2 corporate tax return? A: While bookkeepers can prepare the financial statements needed for your T2, it’s usually best to have a certified accountant review and file your corporate tax return.

Remember, good bookkeeping is the foundation of a healthy Canadian business. Whether you choose traditional bookkeeping services or opt for online accounting services for small business, the important thing is to get your finances sorted.

Don’t let the numbers hold you back. With the right bookkeeping support, you can focus on what really matters: growing your business and living your entrepreneurial dream in the Great White North.

While You Are Looking, Consider New Tools To Streamline Your Finances

While we’re on the topic of making your financial life easier, let’s talk about a game-changer in the world of business expenses: corporate credit cards.

Why Consider a Corporate Credit Card?

Simplify expense tracking

Improve cash flow management

Earn rewards on business spending

Enhance financial control and visibility

But not all corporate cards are created equal. That’s where Float comes in.

Float is Canada’s only all-in-one corporate cards, reimbursements, and bill pay platform that helps customers:

Earn cashback on all categories and save on FX

Generate 4% interest on funds held with Float

Eliminate expense reports and receipt chasing

Close the books 5x faster at the month-end

Want to learn how companies like Clutch, Neo, Knix, and 1,000s of other Canadian businesses on average save 7% of their monthly spend with Float? Get started with Float today by clicking the button below!

Running a Canadian small business? You need the right tools to stay sharp and in the know. Keeping tabs on your finances can be a real headache, especially if you’re a small business owner wearing all the hats. We’ve spent years putting accounting software through its paces, and we’re here to share the cream of the crop. We’ve ranked the best accounting apps for small businesses based on user-friendliness, features, and value for money.

Two standouts have earned our top spots:

QuickBooks Online shines for small to medium-sized operations.

FreshBooks is perfect for solo entrepreneurs and tiny teams.

Ready to find your perfect match? Let’s dive into the best accounting software for Canadian businesses, along with everything you need to know to make the right choice.

Top Picks for Canadian Small Businesses

Overall Best Solution for SMBs ⭐️

Price: $24-160 / month

Reasons to choose QBO:

Scalable to larger finance teams

Tons of integrations and add-ons like payroll, projects, etc…

QuickBooks Online has become a go-to accounting software for many Canadian businesses, and for good reason. This cloud-based solution offers a robust set of features tailored to meet the needs of small to medium-sized enterprises.

Key Features

Invoicing: Create professional invoices and easily track payments.

Expense Tracking: Capture receipts with your smartphone and categorize expenses automatically.

Bank Connections: Sync with your bank accounts for real-time financial updates.

Canadian Tax Support: Automatically calculate GST/HST and prepare returns.

Payroll Integration: Manage employees’ pay and taxes (additional fees may apply).

Reporting: Generate detailed financial reports to gauge your business health.

Multi-User Access: Collaborate with your team or accountant in real-time.

Mobile App: Manage your finances on-the-go with iOS and Android apps.

Who It’s Best For

QuickBooks Online is particularly well-suited for:

Small to medium-sized businesses

Service-based companies

Retailers with inventory needs

Businesses looking for scalable solutions

Its versatility and comprehensive feature set make it a solid choice for many Canadian businesses looking to streamline their accounting processes.

Xero is a powerful cloud accounting solution gaining traction among Canadian businesses. Known for its user-friendly interface and robust features, Xero offers a fresh alternative to traditional accounting software.

Key Features

Bank Reconciliation: Automatically import and categorize bank transactions.

Invoicing: Create and send professional invoices, with online payment options.

Expense Claims: Easily track and manage business expenses.

Inventory Management: Keep tabs on stock levels and costs.

Project Tracking: Monitor time and costs for client projects.

Payroll: Manage employee payments and taxes (through integration with Payroll.ca).

Multi-Currency: Handle transactions in over 160 currencies.

Financial Reporting: Generate customizable reports for better insights.

Mobile App: Access your accounts on-the-go with iOS and Android apps.

Who It’s Best For

Xero is particularly well-suited for:

Small to medium-sized businesses

Companies with inventory management needs

Businesses that work internationally

Teams that value collaboration and need multi-user access

Its clean interface and strong feature set make Xero an attractive option for businesses looking for a modern, scalable accounting solution.

Canadian-Specific Features

GST/HST tracking and reporting

Integration with Canadian banks

Compliance with Canadian accounting standards

While Xero is newer to the Canadian market compared to some competitors, it’s rapidly evolving to meet the specific needs of Canadian businesses. Its cloud-based nature means you’re always using the latest version, with updates and improvements rolling out regularly.

FreshBooks is the only free accounting software that’s gained popularity among Canadian freelancers, small business owners, and service-based professionals. Known for its user-friendly interface and focus on simplicity, FreshBooks offers a refreshing approach to managing finances.

Key Features

Invoicing: Create professional, customizable invoices with automatic payment reminders.

Expense Tracking: Easily capture and categorize expenses, with receipt scanning via mobile app.

Time Tracking: Built-in timer for accurate billing of hourly work.

Project Management: Collaborate with team members and clients on projects.

Client Portal: Provide clients with a secure space to view and pay invoices.

Reporting: Generate insightful financial reports including profit & loss statements.

Double-Entry Accounting: Ensures accuracy and is suitable for accrual accounting.

Bank Reconciliation: Connect your bank accounts for automatic transaction imports.

Mobile App: Manage your business on-the-go with iOS and Android apps.

Who It’s Best For

FreshBooks is particularly well-suited for:

Freelancers and solopreneurs

Service-based small businesses

Agencies and consultancies

Businesses prioritizing ease of use over complex features

Its focus on simplicity and strong project management tools make FreshBooks a go-to choice for many service-based professionals.

Canadian-Specific Features

GST/HST tracking and reporting

Integration with Canadian payment gateways

Support for Canadian tax rates

Compatibility with Canadian banks for bank feeds

The software’s strength lies in its simplicity and focus on the needs of service-based businesses. While it may not offer the depth of features found in some other accounting solutions, its ease of use and time-saving capabilities make it a compelling choice for many Canadian entrepreneurs.

Wave is a cloud-based accounting solution that’s made waves in the Canadian market, particularly among small businesses, freelancers, and entrepreneurs. Its standout feature? It’s free for accounting, invoicing, and receipt scanning.

Key Features

Accounting: Double-entry bookkeeping system

Invoicing: Create and send professional invoices

Receipt Scanning: Capture and organize receipts via mobile app

Bank and Credit Card Connections

Financial Reporting

Multi-Currency Support

Customizable Sales Taxes

Collaborator Access: Add accountants or team members

Paid Add-ons:

Payments: Accept credit card and bank payments (pay-per-use)

Payroll: Full-service payroll for Canadian businesses (monthly fee)

Who It’s Best For

Freelancers and solo-preneurs

Small service-based businesses

Startups and new businesses on a tight budget

Businesses with simple accounting needs

Canadian-Specific Features

GST/HST tracking and reporting

Integration with Canadian banks

Support for multiple currencies, including CAD

Wave stands out in the Canadian market for its commitment to providing free, capable accounting software. It’s an excellent starting point for new businesses or those with straightforward financial needs. The software is continuously updated, ensuring users always have access to the latest features.

While it may lack some of the advanced features of paid software, Wave’s core functionality is robust enough for many small Canadian businesses. Its pay-per-use payment processing and affordable payroll services allow businesses to add features as they grow.

Sage 50 (formerly known as Simply Accounting) is a comprehensive accounting solution tailored for small to medium-sized Canadian businesses. Known for its powerful features and deep functionality, Sage 50 is a go-to choice for businesses with complex accounting needs.

Key Features

General Ledger: Detailed tracking of all financial transactions.

Accounts Payable & Receivable: Manage bills and invoices efficiently.

Inventory Management: Track stock levels, costs, and sales.

Job Costing: Monitor expenses and profitability for specific projects.

Payroll: Built-in Canadian payroll system with tax calculations.

Multi-User Access: Collaborate with team members and accountants.

Bank Reconciliation: Easily match transactions with bank statements.

Fixed Asset Management: Track depreciation and asset values.

Business Intelligence: Generate in-depth financial reports and forecasts.

Customizable Dashboard: Get a quick overview of your financial status.

Who It’s Best For

Sage 50 is particularly well-suited for:

Established small to medium-sized businesses

Companies with complex inventory needs

Businesses requiring detailed job costing

Organizations needing strong audit trails

Those preferring a more traditional accounting software approach

Its powerful features make Sage 50 a solid choice for businesses that have outgrown simpler accounting solutions.

Canadian-Specific Features

Built-in Canadian payroll with up-to-date tax calculations

GST/HST tracking and reporting

Compliance with Canadian accounting standards

Canadian-specific financial statements and forms

As a long-standing player in the Canadian accounting software market, Sage 50 is deeply attuned to the needs of Canadian businesses. It offers a level of depth and customization that many growing businesses find essential.

While Sage 50 is primarily a desktop solution, it does offer cloud access through Sage 50cloud, allowing for some of the flexibility of cloud-based systems while maintaining the robust features of the desktop version.

Choosing the Right Software for Your Business

Consider these factors:

Your budget – pick the tool that you can afford first and foremost

Business size and growth plans – make sure to choose something that will scale with your business. Switching accounting systems after the fact can be very time consuming and costly

Needed features – research must-have features for your business needs (e.g., inventory, payroll).

Ease of use – find something that you will feel comfortable with yourself.

Give it a try – most of the tools offer free trials. Consider signing up on a trial and seeing if the software works for your needs.

If you don’t have anyone to ask for help, consider the following criteria:

Take advantage of free trials

Check for Canadian-specific features (like GST/HST tracking)

Read user reviews from fellow Canadian business owners

Ensure the software can grow with your business

Remember, the best accounting software for your Canadian business is the one you’ll actually use. Don’t get bogged down by fancy features you’ll never touch.

FAQ

Is there truly free accounting software for Canadian businesses?

Yes! Wave is a solid free option. Just be aware that some advanced features may come with a cost.

Do I need special accounting software if I’m a freelancer?

Not necessarily. Simple options like Wave or FreshBooks often suffice for freelancers and solo-preneurs.

Can I switch accounting software mid-year?

You can, but it’s best to do it at the start of a fiscal year to avoid complications.

How often should I update my books?