How to Get a Business Credit Card: A Step-by-Step Guide

A business credit card can be a powerful tool—helping you manage cash flow, build business credit and keep personal and business expenses separate. But knowing how to get a business credit card (and which one to choose) isn’t always straightforward.

This comprehensive guide walks you through how to get a business credit card without the headache. From determining your eligibility to submitting your application, you’ll find it all here. We’ve also included tips to maximize your approval odds, along with answers to the most frequently asked questions on these cards from business owners.

Ready to learn how to get a business credit card? Let’s go!

What is a business credit card?

A business credit card is a type of corporate card designed specifically for business-related expenses—like inventory, software subscriptions, travel and day-to-day operations. It offers companies a flexible way to manage cash flow, track spending and often earn rewards or cash back on purchases. Unlike personal credit cards, business cards also help you build business credit, which can be valuable as your company grows.

Business credit card vs. corporate credit card

In Canada, “business credit card” and “corporate credit card” are often used interchangeably. However, there are differences between the two types of cards.

Business credit cards are designed for entrepreneurs, sole proprietors and small businesses. They require a personal credit check and guarantee, meaning you’re personally liable if the business can’t cover the balance. These cards are ideal for smaller operations with limited expenses.

Corporate credit cards cater to larger businesses, scaling startups and SMBs with higher spending needs. They offer greater spending limits, advanced expense tracking and automated controls. Unlike with business credit cards, personal guarantees are not required for corporate cards, so your personal credit or assets are not at risk. Approval is based on the financial health of the business and the company is responsible for paying the balance each month, not individual cardholders.

How to get a business credit card in Canada: Prerequisites

While it may seem daunting to get a business card, there are a few steps you can take to simplify the process and maximize your approval odds.

1. How to get a business credit card: Eligibility requirements

In Canada, businesses must prove their eligibility and often include supporting documentation to apply for a credit card.

- Is the business registered?

- Do you have a valid business number?

- If incorporated, do you have Articles of Incorporation or a Masters Business License?

For more information on registering your business, please visit the Government of Canada website. Province-specific support can be found here.

2. Gather necessary documentation

Collect key documents such as your business registration, tax ID (EIN) and financial statements. You should also be prepared to provide personal information. For small business owners and operators, please note that your personal credit score may impact your business credit card approval.

Pro tip: Separating your personal and corporate cards is key for protecting your personal credit score. You can find tips for getting approved for a virtual corporate card without hurting your credit score here.

3. Choose the right card

Evaluate your business needs and spending habits to determine the type of business credit card that best suits your operations.

Consider factors such as:

- Annual percentage rate (APR): The cost to borrow money if you plan on carrying a monthly balance.

- Rewards: These can include points, travel miles, cashback or other perks based on your qualifying spend.

- Fees: Most cards charge an annual fee (although Float doesn’t), so consider if the perks are worth it.

- Additional cards: Are they readily available if you need them for your team?

- Foreign transaction fees: These can add up if you conduct business internationally.

- Insurance coverage: For expenses such as travel, car rentals or technology, are you protected in the event of theft or damage?

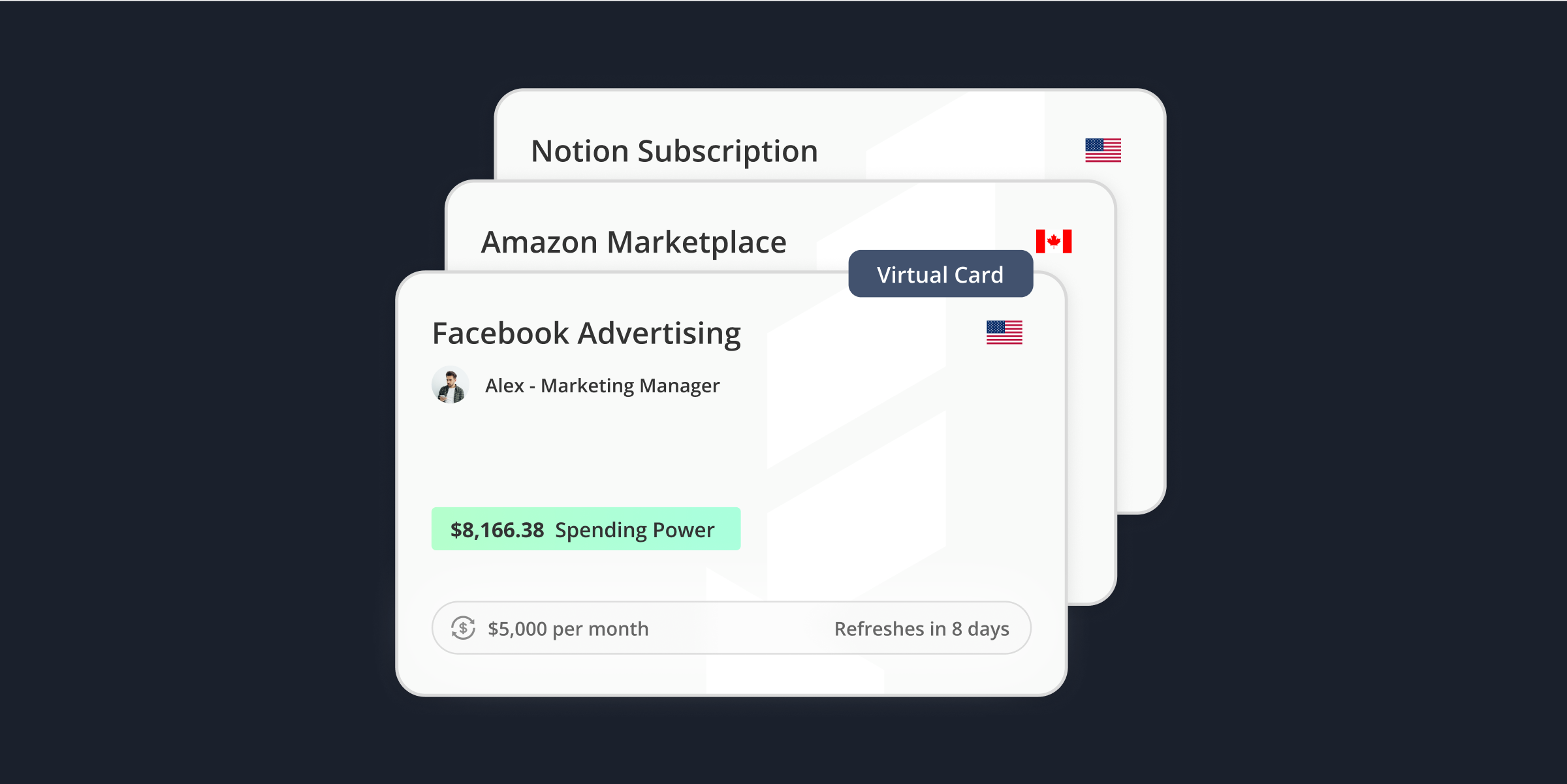

- Card type: Do you require physical cards, virtual cards or a combination of formats?

- Digital experience: Can cards be integrated with your existing systems for user-friendly experiences and easy expense tracking?

Pro tip: Before selecting a card, compare the 7 best credit card options for Canadian businesses in 2025.

4. Complete your application

Most credit card applications can be completed online. Ensure all information is accurate and complete, and be prepared to provide additional information if requested by the issuer.

How long does it take to get a business credit card?

Waiting weeks to get approved for a business credit card was once the norm, especially with traditional banks that rely on lengthy review processes and paperwork. But that timeline doesn’t work for fast-moving startups or small businesses that need access to funds now, not next month.

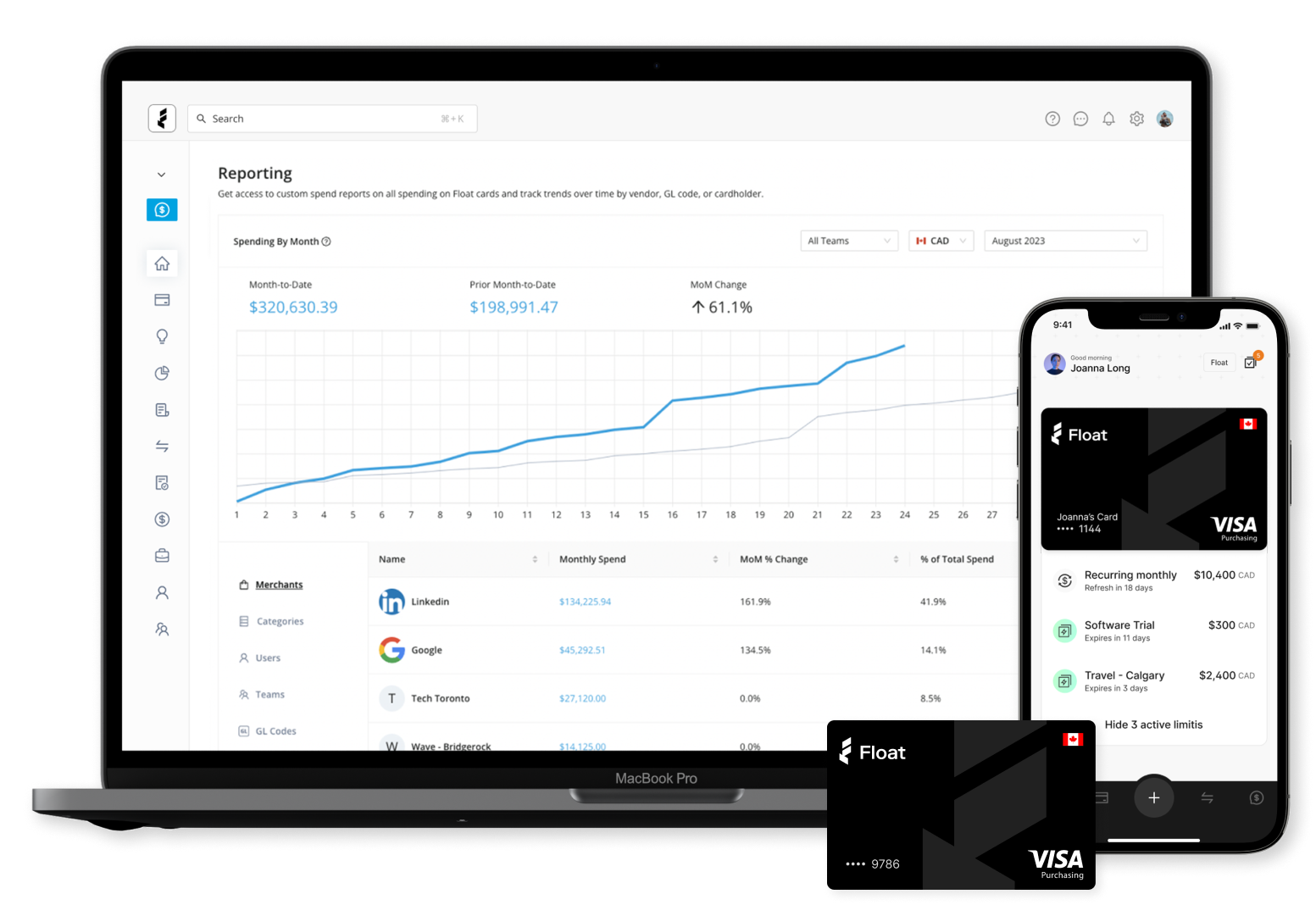

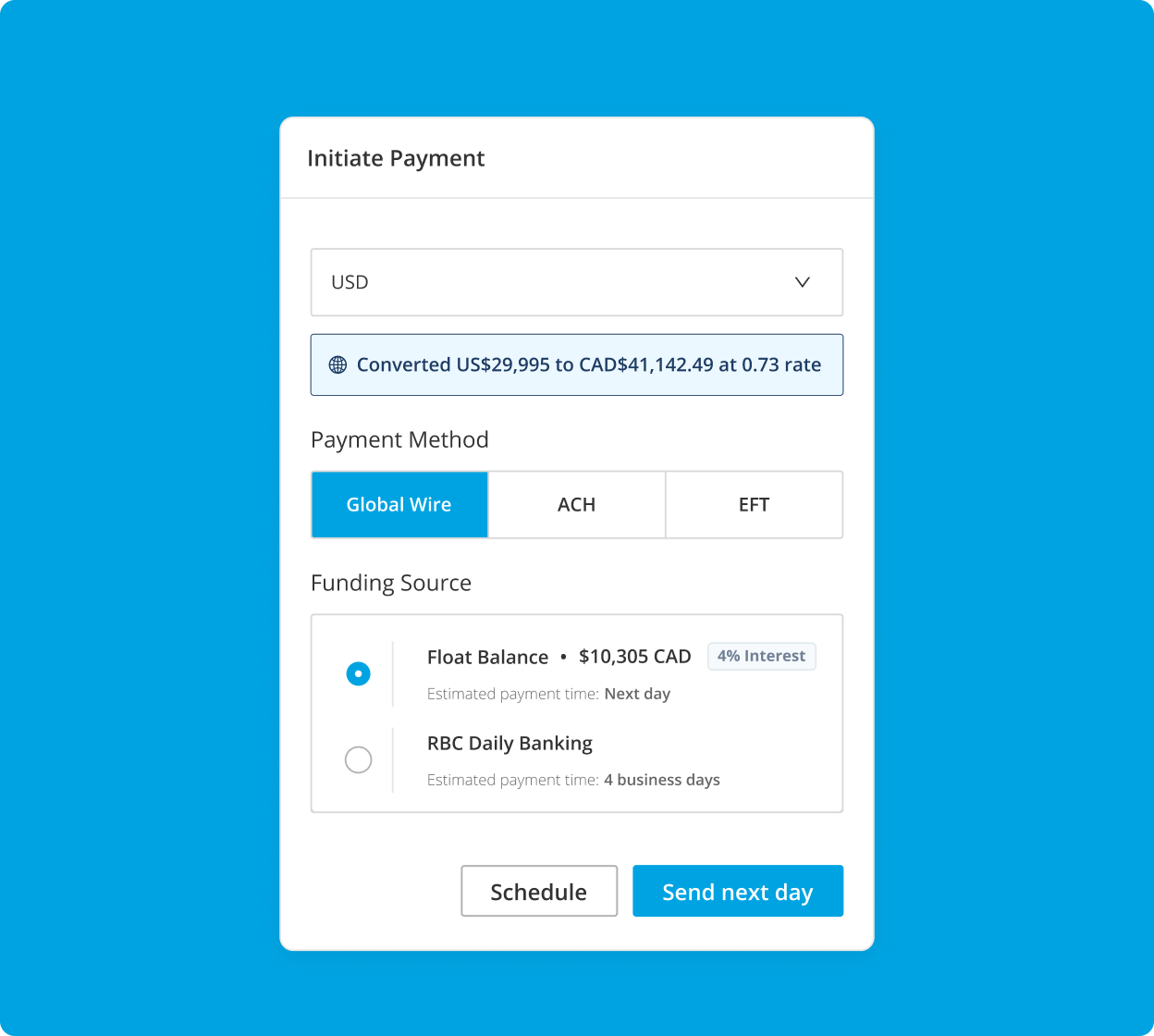

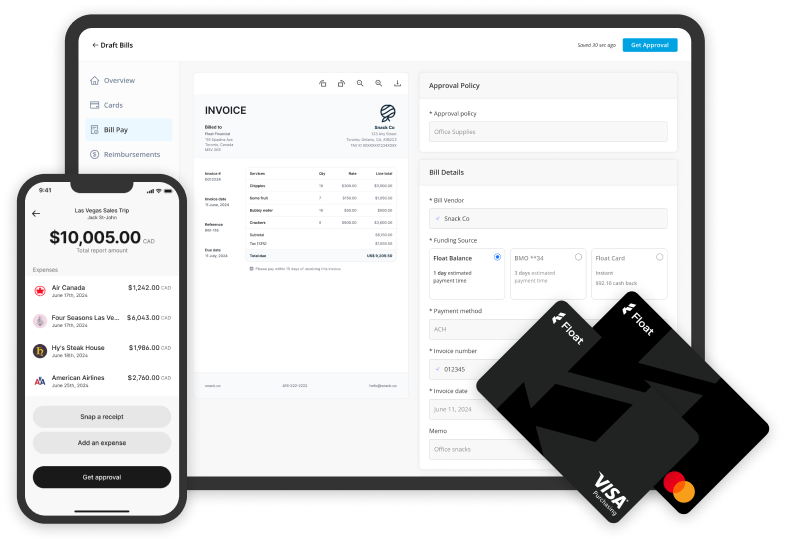

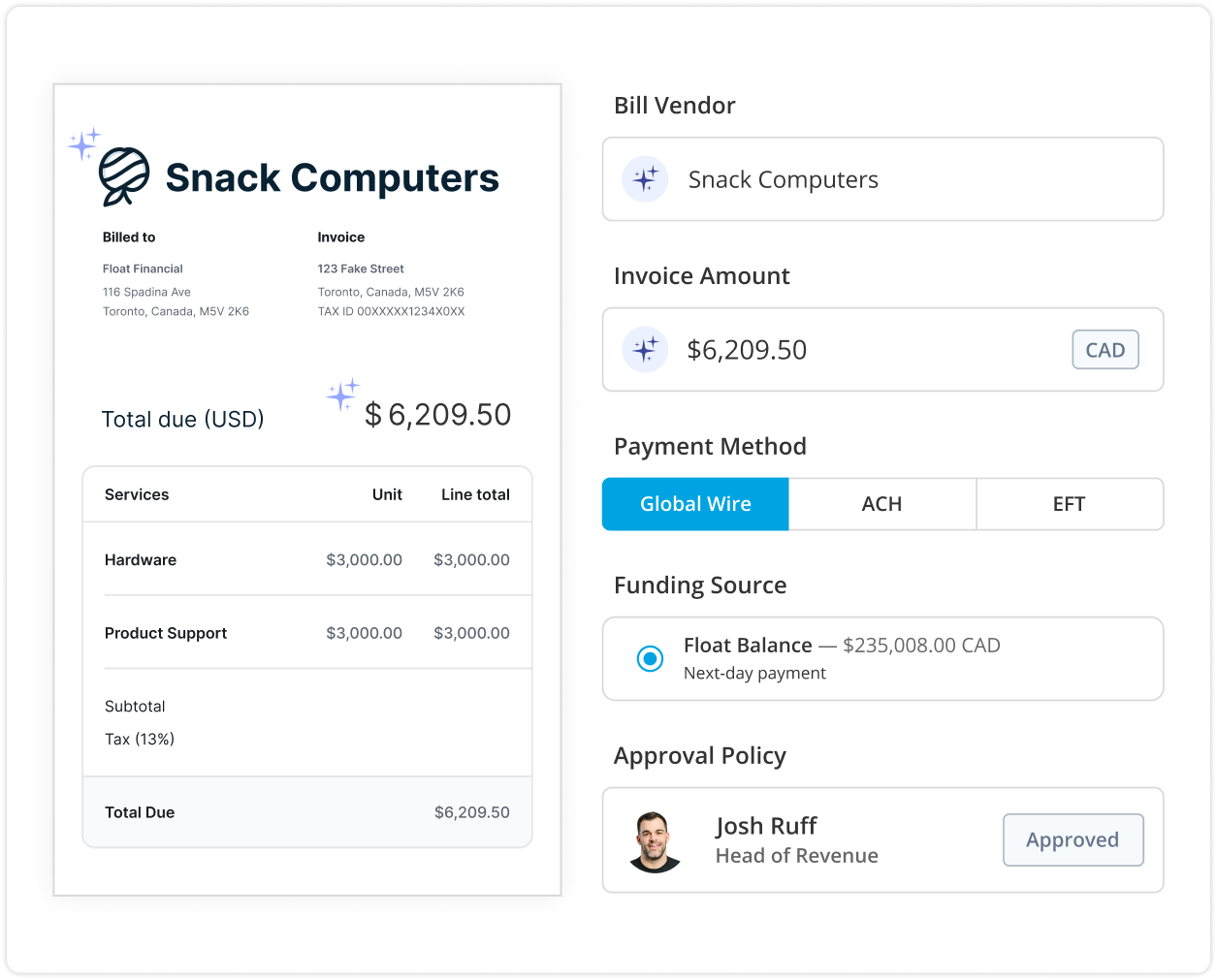

With instant corporate card issuance from providers like Float, you can skip the wait. Instant issuance enables your company to get approved and set up with a business credit card in as little as one day. No branch visits, no red tape—just fast, seamless access to company spend.

Tips on improving your approval odds

Getting approved for a business credit card isn’t always straightforward, especially for early-stage startups or small businesses without a long credit history. But there are a few smart steps you can take to boost your approval odds:

1. Keep your personal credit in good shape

For many new businesses, personal credit plays a big role in the approval process. Here’s how to keep it strong:

- Pay your bills on time and keep your credit use low

- Regularly check your credit report and fix any errors

- Limit the number of hard credit inquiries in a short period

2. Demonstrate business stability

Lenders want to see that your business is stable and reliable. You can demonstrate that by:

- Registering your business properly and keeping your info consistent

- Using a business bank account

- Paying vendors and bills on time to build business credit

- Showing revenue growth or consistent income

- Having a business address and a few months of operating history

3. Apply strategically

Not every card is a fit for every business. Improve your chances by:

- Applying only for cards that align with your business size and financial profile

- Understanding the card issuer’s approval criteria in advance

- Keeping your application accurate and complete

Frequently asked questions

Have credit card application questions? Your answers are here.

Eligibility often depends on your business structure and creditworthiness.

Yes, a strong personal credit score can increase your chances of approval.

These can include rewards, credit line access and financial separation between personal and business expenses.

Yes! Depending on your business credit card provider, you can get both physical and virtual credit cards. Float offers both virtual and physical credit cards options for users.

Business credit card application checklist for Canada

Before applying for a business credit card in Canada, ensure you have the following documents and information prepared, as they may be requested throughout the application process:

- Business registration (e.g., Articles of Incorporation, Master Business Licence, or provincial/territorial registration)

- Business Number (BN) issued by the Canada Revenue Agency (CRA)

- Business incorporation documents, such as:

- Certificate of Incorporation

- Articles of Incorporation

- Certificate of Amalgamation (if applicable)

- Recent financial statements, including:

- Income Statement (Profit & Loss)

- Balance Sheet

- Business plan (typically required for startups or newly incorporated businesses)

- Government-issued personal identification (e.g., Canadian driver’s licence, passport) for:

- Authorized signers

- Beneficial owners (anyone owning 25% or more of the business)

Float’s Know Your Business (KYB) application requirements

When applying for a Float corporate card, you’ll need to provide the following information as part of our KYB verification process:

- Legal entity name

- Principal place of business (legal address)

- Jurisdiction of incorporation (e.g., Ontario, British Columbia)

- Corporate identification number (e.g., Corporation Number or Business Number)

- Business type (e.g., SaaS, retail, professional services)

- Legal structure (e.g., corporation, partnership, sole proprietorship)

Take the next step for your business credit card with Float

Whether you’re launching a new business, scaling operations or looking to separate business from personal expenses, we can help you get a business credit card today. To learn about options that can help you streamline and manage your finances more effectively, contact our team at Float.