TORONTO, April 3, 2025 – Float, Canada’s complete business finance platform, today announced the launch of Float FX, a new solution that enables Canadian businesses to easily and instantly convert funds at rates that are 90% lower than traditional banks. This launch is part of Float’s broader US spending package designed to support businesses with any degree of US operations, helping mitigate the impact of currency volatility, rising operating costs and overall trade tensions.

Float’s recent survey for The Financial Outlook of SMBs in 2025 report found that while 39% of Canadian businesses exchange currency weekly or monthly, over half struggle with high fees and poor exchange rates, while 41% find it challenging to manage CAD-USD fluctuations. These findings highlight the significant gap in Canada’s financial infrastructure, where outdated banking systems and slow processes make currency conversion costly and inefficient. Many businesses still rely on traditional financial institutions that require in-person visits, manual approvals or long settlement times, leaving them vulnerable to fluctuating exchange rates and hidden fees.

“With the Canadian dollar under pressure and potential trade disruptions looming, we designed Float FX to give Canadian businesses an advantage when operating across the border,” said Rob Khazzam, CEO and Co-Founder of Float. “Combined with offering high-yield interest on CAD and USD balances, Float provides material opportunities for companies to save on costs and protect margins—at a time when every dollar counts.”

At launch, Float FX offers market-leading fees of just 0.25% all-in—up to 90% lower than Canadian banks—along with seamless, built-in currency conversion within the Float platform. Businesses can convert, hold and spend USD all in one place, eliminating high costs, long delays and the need for a USD bank account.

“This FX solution was purpose built for the Canadian market from the ground up,” says Andrew Dale, Chief Financial Services Officer at Float. “That means we don’t use third-party tools that pile on additional costs for business owners and operators. Instead, we worked backwards from what we know Canadian companies need and built exactly that.”

Instantly convert between CAD and USD and vice versa at industry-leading rates of 0.25%.

Easily manage USD and CAD balances directly within Float—without needing a US-domiciled account.

Issue USD cards, pay US vendors via wire or ACH and reimburse US employees within Float.

Float FX is available now for all Float customers. Businesses can start taking advantage of Float’s market-leading FX rates immediately, with no minimum or maximum transaction limits.

About Float Float is Canada’s complete business finance platform, combining modern financial services and software to help businesses spend, save, and grow. Trusted by more than 4,000 Canadian companies, Float provides high-limit corporate cards, automated expense management, next-day bill payments, high-yield accounts and fast, friendly support—all built in Canada, for Canada.

Trying to keep a handle on company spending without the right tools? It may be time to explore the best expense management software to help your team spend smarter without increasing your administrative workload.

And if you’re operating on an outdated system that isn’t helping you, now is the time to upgrade. Throughout the rest of 2025, Canadian businesses are likely operating in an uncertain state. Inflation, rising supplier costs and tighter margins are forcing business owners to keep a closer eye on spending.

To complicate matters, 55% of business owners struggle with financial tools that don’t integrate well, leaving them to scramble for receipts and vulnerable to overspending.

The right software helps you budget better, spot savings sooner and respond faster to financial pressures. So, let’s walk through what you should know about expense management solutions, how to compare the options on the market today and best practices for success.

What is expense management software?

Expense management software helps businesses stay on top of spending. It simplifies how teams track, record and review expenses, but today’s platforms go far beyond the basics.

Modern tools automate administrative tasks like receipt collection and report generation, enforce company expense policies, speed up reimbursements and provide real-time insights into where money is going. For finance teams, this means fewer errors and more reliable data. Plus, it provides a faster and smoother way for employees to handle expenses and receive timely reimbursements.

Expense management vs. expense tracking

While the terms are often used interchangeably, there’s a big difference between tracking expenses and truly managing them.

Expense tracking

Expense tracking typically involves recording spending after it happens, often using spreadsheets, accounting software, or basic apps to reconcile reports and receipts. While this approach covers the essentials, it may not provide the controls needed to prevent overspending or streamline the overall process.

Expense management

Expense management is proactive. It puts systems in place to guide, control and automate spending before it happens. The best expense management software uses approval flows, spending limits, policy enforcement and real-time data to keep things in check.For businesses that want to move faster, stay compliant and spend smarter, expense management software is a clear step up.

Expense management software vs. expense tracking: What does my business need?

Every business tracks expenses. This helps you navigate tax time, whether you’re reviewing a spreadsheet or a shoebox of receipts. (Finance folks still pale at the sight of any shoebox, but we digress.) Even when it’s accurate, it’s reactive. You’re looking back at what’s already happened.

Expense management flips that around. It’s about setting the rules, automating the process and getting visibility before money goes out the door. Budgets, approvals, restrictions and policy enforcement are all built in.

You’ll likely notice a tipping point when you’re tired of overspending surprises, approval delays or hefty manual admin. Expense management helps businesses of any size, not just the big guys.

Use case study: BenchSci

BenchSci, a fast-growing Canadian AI company, was feeling the pain of outdated expense workflows as it doubled in size. Manual spreadsheets, receipt chasing and slow reimbursements were eating up time and delaying finance operations. “Without Float, we’d be in the position of needing to expand our team,” says senior accountant Bonnie Kershaw.

Switching to Float enabled the team to automate expense management and issue corporate cards, eliminating bottlenecks and reclaiming over 40 hours per month. “We wanted to alleviate the pressure of employees having to pay with their own funds and waiting for reimbursement,” Bonnie explains.

Float also supported BenchSci’s culture of freedom and responsibility, empowering employees while keeping spend within policy.

Types of business expenses to manage

From fixed to flexible and direct to indirect, every business has expenses that love to sneak up on you. That’s why you need expense management software that does the heavy lifting. The right platform should track it all, enforce your policies and free up your time.

Here are key expenses you don’t want to overlook:

Operating costs: The keep-the-lights-on costs like salaries, utilities, insurance, maintenance and subscriptions can add up fast. You need a system that gives you real-time visibility to avoid overspending on your overhead.

Employee reimbursements: In most businesses, there are moments that pop up where employees are spending money out of their own pocket and then requesting reimbursement. Your system should make managing reimbursements easy for your finance team and beyond. The right system also lets you catch the receipt, apply your spending rules and keep expectations crystal clear. No more chasing paper trails.

Travel expenses: This includes flights, meals, accommodations, gas, parking and more. Do you track and reimburse individual receipts? If receipts are piling up faster than frequent flyer miles, it’s time to let your software take the wheel.

Petty cash: Whether you’re buying postage or pastries with cash, small costs add up and need to be recorded. Swap the cash chaos for prepaid cards with better tracking and give your team peace of mind.

Corporate card expenses: Company-issued credit cards are a great way to track employee expenses. However, smart corporate cards with built-in limits and auto-approvals are your finance team’s best friend. They’ll help you scale without losing control or sanity.

Compare top expense management software solutions for Canadian companies

Let’s look at how these stack up side-by-side in this expense management software comparison chart.

*Float Professional plan members. Essential members get unlimited virtual cards and 20 physical cards.

5 tips for choosing the right expense management solution

Not sure where to start? Here are five key factors to consider when choosing the best expense management software for small businesses in Canada.

1. Know what you really need: tracking or management?

Basic tracking tools might suffice if you’re just logging expenses after the fact. But you’ll need full-fledged corporate credit card expense management software if you want proactive control, like setting spending limits, enforcing policies and managing approvals.

2. Look for automation that actually saves time

Choose a tool that doesn’t just look good on paper. The right platform should reduce manual work (think auto-coding transactions, syncing with your accounting software, prompting for receipts) and reclaim hours for your team every month.

3. Make sure it grows with you

As your company scales, your spending will become more complex. Look for corporate credit card expense management software that supports multi-user controls, customizable policies and automation. This software can handle increased volume without expanding your finance team.

4. Prioritize real-time visibility and controls

Proactive spend management means you’re not waiting until month-end close to spot issues. Choose a tool that gives your team real-time access to spending data, approvals and alerts so you can course-correct instantly.

5. Consider local compatibility and support

Some global platforms aren’t built with Canadian businesses in mind. If you’re operating in Canada, make sure the software supports CAD and local tax codes and has an easy path to onboarding Canadian entities. Otherwise, you’ll be stuck filling in the gaps manually.

Best expense management software for Canadian businesses

Now that you know some of the features to look out for, you may be wondering: with so many expense management tools on the market, how do you know which fits your business best, especially if you’re operating in Canada? We’re partial to Float, but we’re happy to dive into the details on why, so you can make the best choice for your business.

Below, we break down some of the top options, what they offer and how they compare.

Float

Float is a modern expense management platform built for Canadian businesses. It streamlines finance operations by combining real-time spend tracking, unlimited virtual and physical corporate cards and accounting integrations.

With built-in approval workflows, automated receipt capture and fast reimbursements, Float makes it easy to stay in control of company spending. It’s designed to scale alongside your team without adding headcount or hassle.

BMO Travel & Entertainment MasterCard

Many of Canada’s big banks offer business credit cards, but it’s rare to find robust expense management solutions. BMO offers a traditional expense management option through its T&E corporate card program, which includes centralized billing and some reporting functionality.

However, this solution lacks modern features like receipt capture, automation or policy enforcement and doesn’t support real-time integrations or virtual cards.

Expensify

Expensify streamlines employee expense reporting, particularly for companies with reimbursement-heavy workflows. It features automatic receipt scanning, mobile submission and integrations with popular accounting tools. It also offers a corporate card, though that’s not the primary focus.

While great for basic reporting and reimbursements, Expensify may lack the advanced spend controls or real-time card management that growing teams need. Its issue resolution process is often slow and inefficient, with frequent technical glitches that disrupt workflows.

SAP Concur

Concur is a global enterprise platform offering highly customizable travel and expense solutions. It supports complex workflows, multi-currency accounting and integrations with large enterprise resource planning systems, making it a fit for enterprise-level operations.

However, many find the platform overly complex, expensive and slow to implement (or so say a ton of Reddit users in this thread), so it may not be the best expense management software for small businesses. The user experience might feel dated compared to newer, more intuitive tools.

Plooto

Plooto is an automated accounts payable (AP) and accounts receivable (AR) platform built for small and mid-sized businesses. It offers next-day payments from cash balances as well as the ability to make payments via EFT, ACH and or international wire transfer in CAD or USD. Designed with accountants and finance teams in mind, Plooto syncs with popular accounting software, keeping your data accurate and up-to-date automatically.

However, Plooto does not offer corporate credit cards. It also doesn’t pay interest on any cash balance carried in the platform. Additionally, some users find the payment processing to be slow.

A look at Float’s expense management software

Float is an expense management platform designed to provide businesses with real-time control over their finances. With corporate cards, automated approvals and seamless accounting integrations, it takes the mess (and stress) out of managing team spend.

Leverage corporate cards

Identify employees who need a corporate card and set spending limits for each cardholder—it’s that simple. Choose from physical or virtual cards with no annual fees. The best part? Receipts and categories are handled automatically, making month-end expense reporting a breeze instead of a scramble.

Reimburse with confidence

Say goodbye to your admin burden. Float’s AI-powered workflows make submitting out-of-pocket expenses feel like taking off early on Friday. Fast approvals (even for mileage) mean your team gets reimbursed quickly. You can also pair Float Cards and Reimbursements to keep all spending in one powerful expense management platform.

Pay bills faster

Let your inbox do the heavy lifting by simply forwarding invoices to Float and watching the software pull data together in seconds. Keep all bills in a centralized location and set up customized approvals. And when it’s time to pay? Float gets it done quickly and securely with EFT, ACH or wire transfer, with up to 4% interest earned on your AP balance. Our Canadian-built solution even tracks GST and HST.

Hassle-free vendor management

With Float, vendor management doesn’t have to feel like herding cats. The platform enables you to pre-approve vendor-specific cards for subscriptions with set limits so there’s no surprise spending. It also tags transactions with receipts, tax codes and vendor info automatically, making vendor payments smooth and spot-on.

Onboarding and change management support

Getting started with Float is seamless. Onboarding, training and change management are all part of the package. From easy syncing with QuickBooks, Xero or NetSuite to setting up smart expense policies and approval flows, Float helps your team spend with confidence. With hands-on support, proactive risk planning and best-practice guidance, you’ll shift gears smoothly with no bumps or detours—just full-speed adoption.

Purpose-built for Canadian businesses, Float helps you ditch the hassle and get back to what matters.

Float: The expense management software your business needs

Choosing the right expense management software comes down to finding a solution that fits the way your team spends—and grows. Whether you need advanced controls, real-time visibility, or just a better way to ditch messy spreadsheets, the best platform is one that actually takes work off your plate.

With a tool like Float in place, you can spend smarter, save time, and stay focused on what really matters: running your business.

Taking advantage of the Small Business Deduction (SBD) and claiming business expenses on your taxes can save you some serious cash. If you don’t know what if you qualify for the SBD or what tax deductions are available for companies like yours, you could be paying more taxes than you need to—money you could be spending on growing your business.

In this article, we’ll explain how to get the Small Business Deduction Canada provides to eligible companies. We’ll also offer an overview of some of the main tax deduction categories for small businesses and give you a list of the top small business tax deductions you can (and should) claim when you file your taxes this year.

The Small Business Deduction (SBD) is a rate reduction tax benefit for small- and medium-sized businesses that reduces the total corporate income tax you owe in a given year. It’s a pretty sweet deal. Normally, Canadian corporations pay the federal tax rate of 15%. With the SBD, companies can get a reduced tax rate of 9% on up to $500,000 of active business income (ABI)—the total income generated from your business operations for the year.

How to qualify for small business deduction

Depending on the size and type of business you run, figuring out if you qualify for the SBD can be kind of complex. We’d definitely recommend reaching out to a tax professional to see if you can take advantage of this benefit.

The Small Business Deduction Canada offers is only available for Canadian-controlled private corporations (CCPCs). This means that businesses controlled by one or more non-residents (i.e., one of the owners is from the US) or another public corporation aren’t eligible. Those that list shares on the stock exchange also aren’t eligible.

To qualify for the SBD, your business must have less than $10 million in taxable capital employed in Canada across all associated corporations. Taxable capital is different from taxable income. Capital refers to the total financial resources you use to generate income for your business—including shareholder’s equity, surpluses and reserves, and loans and advances received during the year.

If your business has between $10 million and $50 million in taxable capital, you can still take advantage of the SBD benefit. However, the amount of ABI that qualifies for a reduced tax rate goes down as taxable capital increases. Earning over $50,000 in aggregate investment income also lowers the total ABI that qualifies for the reduced tax rate. If you earn over $150,000 in investment income (very impressive), you can’t get the SBD.

Each province and territory has its own SBD benefits that can reduce the provincial tax you owe which kicks in if you qualify for the Small Business Deduction Canada offers.

NOTE: The SBD only applies to incorporated businesses. Sole proprietors and partnerships are taxed differently and don’t qualify for the SBD.

What are the tax deduction categories for small business?

In addition to the federal and provincial Small Business Deduction, you can also deduct or “write off” business-related expenses to reduce your total taxable income, therefore reducing the total tax you’ll pay. Generally speaking, any money you spend to run your business is considered a business expense. You might be tempted to claim your daily espresso as a business expense—how would your company function without caffeine?—but the Canada Revenue Agency (CRA) has some rules around what you can and can’t deduct from your taxable income.

It’s smart to organize your transactions into the categories recognized by the CRA as you go, rather than waiting until month-end or *shudder* until you need to file your taxes. This makes closing your books at the end of the month way less stressful. When tax season rolls around, you can easily report your properly-categorized expenses and claim them.

Your accounting software might have some built-in expense category suggestions that should align with the CRA categories. If you’re tracking expenses manually with a spreadsheet, you might want to familiarize yourself with the official CRA categories so you can label your transactions accordingly.

The CRA has a comprehensive list of all the types of expenses businesses are allowed to claim as a deduction. Here are a just a few tax deduction categories that might apply to your small business:

advertising

business tax, fees, licenses and dues

business-use-of-home expenses

capital cost allowance

delivery, freight and express

fuel costs

insurance

interest and bank charges

legal, accounting and other professional fees

maintenance and repairs

management and administration fees

meals and entertainment

long-haul truck drivers

motor vehicle expenses

office expenses

rent

salaries, wages and benefits

supplies

telephone and utilities

travel

FYI, the deadline for small businesses to file taxes is usually April 30 each year, although sole proprietors typically have until June 15 (though they are not eligible for the SBD). Corporations need to file their taxes six months after the end of their tax year.

Top 10 small business tax deductions

If you’re wondering, “What can I write off on my taxes?” you should check in with an accountant or tax expert who can ensure you’re claiming the right expenses—and help you identify expenses you might not realize you can claim. You definitely don’t want to miss out on tax savings you could reinvest in growing your business.

Beyond the SBD, here are 10 small business tax deductions that can help you reduce your taxable income, including a few you might miss when you’re getting your expenses together at tax time:

1. Salaries, wages and contractor fees

You can deduct the gross salary you pay your employees—which is their salary before taxes, benefits and any other payroll deductions that come off their paycheque. You can also claim any payments made to contractors or freelancers who provided services for your business, like a designer you hired to update your website.

2. Cost of goods sold (COGS)

If you make and sell physical goods or run a food-based business, you can claim the supplies, materials, ingredients and packaging you use to create the products you sell. If you run a service-based business, you can also claim the cost of supplies you use to get the job done. For example, a cleaner can claim the cost of the cleaning tools and products they use in their clients’ homes.

3. Office expenses

You can claim the cost of rent, utilities and internet at your office space. You can also claim everyday items you use while you work like stationery, furniture and computers or tablets—as long as you can prove these items are used for business purposes. If you work from home, you can also claim a portion of your bills on your taxes.

4. Business software

When you’re calculating your office and operating expenses, don’t forget about your software subscriptions, which are also part of the above category. This could include your accounting software, inventory or customer management software and collaboration solutions like Microsoft 365 or Google Workspace.

5. Advertising

The cost of running ads on Canadian radio and television stations and in Canadian newspapers is tax deductible—but you can’t claim the costs of advertising outside the Canadian market. You can also claim costs associated with digital advertising and running your business’ website, such as domain and hosting fees.

6. Interest and banking fees

No one loves racking up interest, but hey, at least paying interest on your loans or mortgages on the property you use to do business (or home office space) can lower your taxable income. If you meet the CRA’s criteria, you may be able to claim a portion of these fees. You can also claim banking fees including account service fees and fees for lowering the interest on loans.

7. Legal, accounting, consulting and professional fees

Getting advice from someone about your taxes or contracts? Hired a business coach? You can claim what you pay to professional service providers like lawyers, bookkeepers and accountants, as well as consultants who help you improve your business and expand your skills. If you’re a member of a commercial or trade organization, you can also deduct membership fees or dues.

8. Business travel, meals and entertainment

Turns out, the CRA does want you to have a little fun sometimes. In general, you can claim 50% of meals, beverages and entertainment associated with running your business, such as staff parties, client dinners or during business travel. You can also claim the cost of travelling including flights, hotels and transportation.

9. Vehicle and fuel costs

You can claim the costs associated with running and maintaining the vehicles you use in your business, which could include machinery or the cars your team uses to deliver products or drive to work sites (sorry, the car you use to commute to work doesn’t count). The cost of fuel, repairs, new tires and car insurance can be written off as business expenses.

Float combines intuitive expense management software with flexible corporate cards. When you use Float, all your transactions—including employee purchases like travel, food, office and fuel expenses—land in the same place and are automatically organized into categories that match up with your accounting software. You can also proactively control your expenses with Float cards. In addition to setting spend limits on each card, you can also restrict where the cards can be used to ensure your team spends funds in the right places.

If you’re tired of chasing down receipts and sorting through transactions coming in from all your bank accounts, try Float free and make expense tracking and categorization seamless. Future tax-season you will thank you.

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. Every business is unique, and tax rules can change or vary depending on your specific circumstances. We recommend consulting a qualified accountant or tax professional to ensure you’re making the right decisions for your business.

Toronto, ON – March 12, 2025 – Canadian businesses are navigating a “two-speed economy” as financial pressures mount, according to Float’s Canadian SMB Financial Outlook 2025 report. The study, which surveyed more than 400 small and medium-sized businesses (SMBs), highlights a widening gap between established businesses investing in growth and younger businesses struggling with financial constraints that keep them stuck in survival mode.

While overall business confidence remains stable—dipping only slightly from 87% in Q4 2024 to 86% in Q1 2025—the divide between older, well-established businesses and newer businesses is becoming more pronounced. Experienced SMBs are twice as likely to project 10%+ year-over-year profit growth compared to their younger counterparts, who continue to grapple with limited access to capital and cash flow challenges.

The report also sheds light on the Canadian business response to impending US tariffs and rising operational costs. Although 65% of SMBs expect to be affected by tariffs, a concerning 4 in 10 businesses remain in “wait-and-see” mode—choosing not to adapt their strategies in advance. Top concerns about the impact of tariffs include increased costs when exporting to the US, currency fluctuations and higher prices from US suppliers. At the same time, 7 out of 10 businesses believe expected Bank of Canada rate cuts will have little-to-no impact, signaling that broader economic policy shifts may not provide enough relief.

“Canadian businesses have consistently proven their resilience, but in today’s economic climate, survival is no longer just about perseverance—it’s about access,” said Andrew Dale, Chief Financial Services Officer at Float. “Access to capital, real-time financial insights and efficient financial systems are critical for businesses to stay competitive. To really be elbows-up, we need bold policy changes and financial solutions that target these newer businesses and empower them to plan strategically—without blindspots, long wait times or red tape.”

The report also shows a significant portion of businesses still operate with outdated financial reporting tools, with 44% struggling with inefficient processes, 40% lacking a single financial source of truth, and 39% using tools that don’t integrate effectively. The data also indicates that SMBs with poor financial visibility are more likely to increase spending blindly, potentially making risky financial decisions without a clear understanding of their cash flow. This underscores the importance of efficient financial systems in helping Canadian businesses navigate these uncertain times.

To combat these challenges, Float is committed to equipping Canadian businesses with modern financial solutions that provide real-time visibility, seamless integrations, and efficient financial management.

About Float

Float is Canada’s complete business finance platform, combining modern financial services and software to help businesses spend, save, and grow. Trusted by more than 4,000 Canadian companies, Float provides high-limit corporate cards, automated expense management, next-day bill payments, high-yield accounts and fast, friendly support—all built in Canada, for Canada. Float is backed by world-class venture and fintech investors, including Growth Equity at Goldman Sachs Alternatives and OMERS Ventures.

If you’re running a small business, chances are you’ve experienced cash flow problems at some point. The stress of not knowing if you’ll have enough to cover payroll, supplier payments, or office rent can keep you up at night.

It’s frustrating to work hard, bring in sales, and see profits on paper, only to find yourself short when an unexpected invoice lands or an essential expense arises.

You may feel alone in these struggles, but you have more company in that leaky boat than you realize. In Canada, 60% of small and medium-sized businesses (SMBs) report ongoing cash flow challenges. Look at your small business neighbours. Yep, they’re worried about this, too. This number is only slightly better for established businesses. According to Float data, 48% of SMBs that have been operating for 20+ years reported insufficient cash flow as a top financial challenge in 2024.

The good news? You’re not alone, and there are ways to take control. Plus, we get what it’s like running a small business in Canada. We’ve got you covered.

In this guide, we’ll walk you through the most common cash flow issues small businesses face, why they happen and—most importantly—how to solve them.

Common business cash flow problems

Cash flow problems are one of the biggest challenges small businesses face, and they can feel relentless. When cash runs low, every unexpected expense or delayed payment adds stress, making it feel like you’re always on the edge of a financial crunch.

Why are cash flow issues so common in small businesses?

A few patterns crop up when business owners dig into the dark corners of their cash flow management. (It’s okay, we brought flashlights.) Have a look at the list and see if these sound familiar.

Have you ever struggled with:

Unpredictable revenue cycles that make it hard to plan ahead?

Customers who delay payments, leaving you scrambling to cover your expenses?

Large upfront supplier costs that tie up cash before you’ve even made a sale?

Rising operating expenses that creep up month after month?

Incomplete or poor financial forecasting leading to unexpected shortfalls?

Many small business owners feel like they’re constantly playing catch-up, shifting funds around and hoping nothing major goes wrong.

We get it. But hope isn’t a strategy. Understanding what’s causing your cash flow struggles is the first step to fixing them. So, let’s dig in together.

How many businesses in Canada fail due to cash flow problems?

Cash flow problems impact your financial stability, but beyond that, they also affect your peace of mind. Every small business owner knows the sinking feeling of realizing that despite solid revenue, cash is tight again, and making it through the month will require careful juggling. In fact, 29% of small businesses ultimately have to close because they run out of money, and 67% of small business owners rely on personal funds to keep things afloat—an unsustainable strategy in the long run.

Fears about keeping your business in the black aren’t unfounded. Almost 20% of business owners surveyed have faced past bankruptcy or insolvency. How high is the risk of a business failing? It can vary, but these are not easy times. In the first quarter of 2024, insolvencies were up 87% over the year before, with experts warning of a high number of quiet business failures hiding behind that number.

Small business cash flow problems can pose real risks for business owners. Even if your business seems to be bringing in new customers and making plenty of sales, these signs can hide real troubles. Learning how to solve cash flow problems could be crucial to your business building the longevity you’ve dreamed of.

Business types prone to cash flow issues

We hate to be the ones to say it out loud, but certain industries are more susceptible to problems with cash flow than others. Common culprits include those that require large upfront investments, have long payment cycles or experience seasonal fluctuations.

What might this look like in your business? Common examples include:

Construction firms

Long payment terms and high material costs create cash flow gaps. You may end up trying to cover multiple payroll cycles (and even overtime) long before you’re paid for a job.

Retailers and wholesalers

Balancing your stock levels is a juggling act. Holding too much inventory ties up cash, while slow-moving stock leads to liquidity issues.

Agencies or companies with extended payment terms

If you’re a recruiter, you may not be able to bill your client until you’ve completed the placement of a candidate. Payment delays from clients can disrupt payroll and make it difficult to operate smoothly.

Hospitality businesses

You may have months where business slows to a trickle. Seasonal variations impact revenue consistency, making it hard to cover fixed costs during slow months.

Startups

More invoices and fees? We haven’t billed a single customer! If this thought has tightened the tension around your skull more than once, this could be you. Heavy upfront costs before revenue kicks in can leave early-stage businesses tight for cash.

If your business falls into one of these categories, proactive cash flow management is critical.

10 common cash flow problems (and how to fix them)

While cash flow issues are common, they’re not inevitable. Understanding why they happen will help you start taking proactive steps to regain control. With help, you can stabilize your cash flow and set your business up for long-term financial health.

Some of these challenges can be made easier with financial tools that give you better control and visibility over your cash flow. We’ll walk you through 10 common cash flow problems and solutions to help you tackle them.

1. Late customer payments

Many small businesses operate on tight margins, so when customers don’t pay on time, it can throw everything off balance—like famous Italian leaning tower levels of off balance. You still have bills to pay, employees to compensate and suppliers to keep happy. When you’re chasing overdue invoices, it takes time away from running and growing your business.

Solution: Set clear payment terms, offer early payment discounts and use automated invoicing tools to follow up on overdue payments.

2. Revenue fluctuations

Not every business has steady income each month. Seasonal businesses or those affected by market shifts often experience unpredictable revenue cycles. You may have a great month followed by a slow one, making it tough to manage expenses consistently.

Solution: Build a cash reserve during peak periods, diversify revenue streams and forecast cash flow regularly.

3. Upfront supplier payments

Many businesses must pay suppliers before they generate revenue. This creates a cash crunch, especially for companies that need to invest heavily in inventory, materials or services before getting paid.

Solution: Negotiate better payment terms, explore just-in-time inventory management or use credit options to delay payments.

4. High overhead costs

Fixed costs like rent, utilities and payroll don’t go away, even when business slows down. If expenses keep creeping up while revenue stays the same, cash flow gets squeezed tight like a pair of too-skinny jeans.

Solution: Audit expenses, cut unnecessary costs and consider flexible lease options or remote work setups.

5. Poor financial planning

Many small business owners focus on sales and operations but overlook financial forecasting. Many have business acumen and strengths that may not include deep financial literacy. Without a clear cash flow plan that includes cash flow statements and other key financial planning documents, unexpected expenses or slow months can cause financial stress.

Solution: Use accounting software to track cash flow, create realistic budgets, and plan for potential shortfalls.

6. Expense management inefficiencies

Unmonitored spending by employees or disorganized expense tracking can drain cash reserves faster than expected. Without proper oversight, it’s easy to lose track of where money is going.

Solution: Implement an expense management system to monitor and control spending in real time.

7. Tax compliance surprises

Nothing disrupts cash flow like an unexpected tax bill, and with online access to everything, there’s no pretending anything got lost in the mail. Many small businesses underestimate their tax liabilities or miss filing deadlines, leading to penalties and financial strain.

Solution: Set aside tax reserves, use automated tax software and consult a professional accountant to avoid surprises.

8. Inventory mismanagement

Too much inventory means cash is tied up in unsold products, while too little inventory can lead to missed sales opportunities. Striking the right balance is essential.

Solution: Use inventory management software to optimize stock levels and reduce holding costs.

9. Emergency expenses

Unexpected costs like equipment breakdowns, legal fees or emergency repairs can drain your cash reserves overnight. Without a financial cushion, these expenses can be devastating.

Solution: Maintain a contingency fund and explore business insurance options to protect against unexpected expenses. You can even earn interest on those funds, if you opt for a high-interest yield account, like Float Yield, which offers 4%.

10. Access to credit

When cash is tight, having access to financing can make the difference between surviving and shutting down. But many businesses struggle to secure loans or credit lines when they need them most. Solution: Establish good credit, explore business lines of c

How Float can help you manage cash flow with confidence

Float provides an all-in-one expense management platform that helps you track spending in real time, automate expense approvals and gain critical visibility into your financial health.

With Float’s corporate cards, you can set spending limits, automate receipt collection and prevent overcharges. This ensures that every dollar spent is accounted for and surprise expenses don’t catch you off guard. (Less panic means you get to spend a few weekends relaxing instead of transferring money around, hoping to cover everything.)

Float also helps you gain financial control by integrating corporate cards with real-time expense management. Unlike traditional solutions that encourage spending, Float is designed to help you spend smarter while offering up some pretty appealing rewards, like high-yield accounts.

Proactive cash management is essential, but business cash flow problems don’t have to derail your business. The key is to stay proactive, monitor your finances closely and leverage the right tools to improve business cash flow management.

Looking for smarter ways to manage your business expenses? Explore how Float can help improve your cash flow visibility and control.

AI adoption is growing rapidly in Canada. But how are companies using AI to drive efficiency and innovation?

Businesses use AI for everything from automating customer service and streamlining workflows to global marketing campaigns and laundry sorting. In many industries, AI adoption is quickly moving from cost-cutting advantages to must-have tools. Companies in these already innovative sectors that fail to adopt AI risk falling behind, while those in industries with lower AI adoption still have the chance to gain a competitive edge.

No matter where your business falls on the AI scale, looking at AI industry trends specific to Canada can help you benchmark its adoption efforts by understanding where competitors are likely investing, identifying emerging opportunities, and optimizing spend to make the most of your investments.

With insights from millions of transactions across thousands of Canadian businesses, Float offers a unique real-time look at corporate finance trends and AI spending. Our data highlights clear distinctions—industries leading AI adoption, those lagging behind, the tools businesses are investing in, and the average cost of these transactions.

Let’s dive in.

Confident SMBs are 2x as likely to expect >10% profit growth

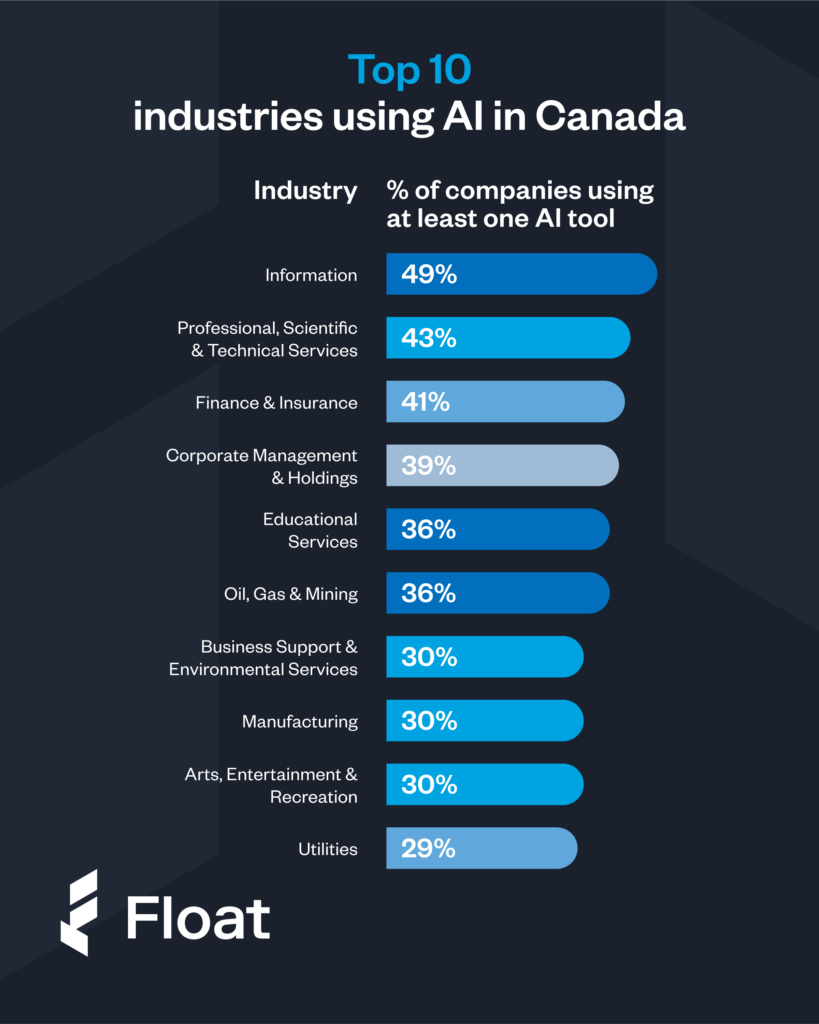

AI adoption is most prevalent in knowledge-based industries such as IT, consulting and finance-related industries, where automation, data analysis and predictive modeling provide a competitive advantage. These sectors have embraced AI to streamline operations, enhance decision-making and optimize customer experiences.

Traditional industries, including mining and manufacturing, are also incorporating AI, but at a slower rate. While these industries benefit from automation and predictive maintenance, adoption is not as rapid, likely due to infrastructure challenges and higher implementation costs.

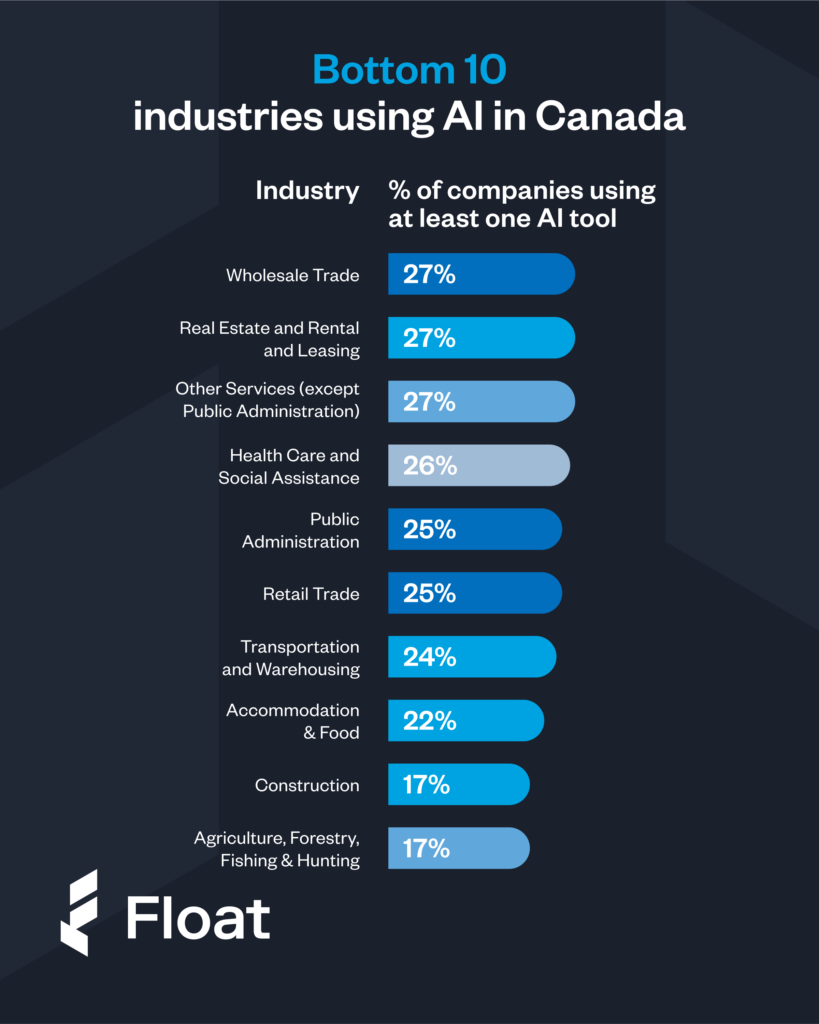

Industries lagging in AI adoption

Despite significant potential for automation and personalization, customer-facing industries such as retail and hospitality have lower AI adoption. Many businesses in these sectors still rely on traditional customer service methods and manual operations, slowing AI integration. But, retail is an industry poised for innovation, especially when it comes to spend management and overall financial operations. For example, retail and ecommerce businesses are already using virtual credits cards and expense automation to optimize ad spend with campaign-specific credit cards and targeted spend controls, keeping them growing without going over budget. AI could be the next step here.

Public sector organizations and healthcare providers are also lagging in AI adoption, despite opportunities to improve operational efficiency, patient care and decision-making. Regulatory concerns and bureaucratic hurdles may be contributing factors.

Agriculture and construction have the lowest AI adoption rates, even though AI could enhance predictive analytics, automate workflows and improve resource management. Limited technological infrastructure and the hands-on nature of these industries may be barriers to widespread AI use.

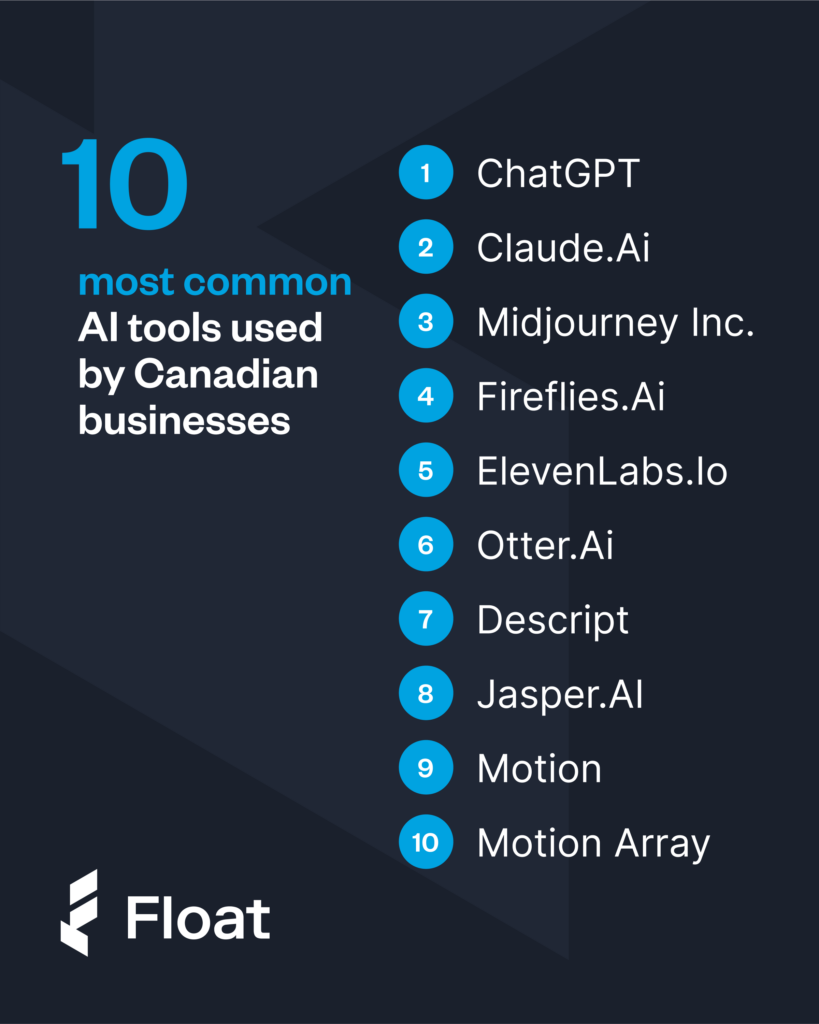

Most common AI tools used by Canadian businesses

AI-powered writing and communication tools such as ChatGPT,Claude.Ai and Otter.Ai are the most widely used across Canadian businesses. These tools support content creation, transcription and real-time collaboration, making them valuable for various industries.

Creative AI tools like Midjourney and Leonardo.Ai are gaining traction in content-driven industries. Businesses focused on marketing, design and media are increasingly leveraging AI to generate high-quality visuals and streamline creative workflows.

Productivity and workflow automation tools such as Fireflies.Ai, Reclaim.Ai, and Motion indicate a strong demand for AI-driven efficiency improvements. These tools help teams automate scheduling, transcription and workflow optimization to enhance productivity.

What this data doesn’t capture are AI features embedded within existing platforms, such as Google’s Gemini, which are seamlessly integrated into business workflows without requiring separate subscriptions. To cut costs, some businesses that already use Google workspace might consider replacing ChatGPT subscriptions with Gemini use among their employee base.

What businesses are spending on AI subscriptions

Float customers have collectively spent nearly $2 million on ChatGPT alone, significantly outpacing spending on other AI tools. This suggests that ChatGPT has become a core tool for businesses, driving efficiencies in content creation, communication and automation.

Many businesses are spending most of their AI budget on a single tool, which raises the question—are they using AI in the best way, or just relying too much on one option? Companies might get better results by either trying different AI tools or cutting back on overlapping subscriptions to save money.

Since more AI features are being built into everyday software, businesses should check if they’re fully using what they already have. It’s important to track whether these tools are actually helping with productivity, reducing costs, or increasing revenue.

The future of AI use in Canadian industries

AI adoption is expanding across Canadian industries, but its use varies significantly by sector. Businesses must regularly evaluate their AI investments to ensure they are maximizing efficiency and optimizing costs. The rapid rise in AI-related spending underscores the need for a strategic approach to AI budgeting, balancing innovation with financial sustainability.

The U.S. has just announced new tariffs on steel and aluminum imports from Canada. While the more widespread proposed tariffs still remain on hold until March 4, these latest developments mean rising costs and supply chain disruptions are on the horizon. If tariffs go into effect, small businesses will feel the squeeze first. Higher costs, disrupted supply chains, and tighter margins mean that businesses need financial tools that move as fast as they do.

So many questions remain. Will tariffs actually happen? Which industries will be hit hardest? And how can your business stay resilient, no matter what?

In this article, we’ll break down what tariffs are, how they might impact Canadian SMBs and, most importantly, the proactive steps your business can take to navigate this period of economic uncertainty. You’ll learn practical strategies to mitigate risks, manage costs and keep your business agile in the face of potential trade disruptions.

What is a tariff?

A tariff is a tax imposed by a government on imported or exported goods. These taxes are used to:

Protect domestic industries

Generate government revenue

Influence international trade policies

In this case, President Trump’s proposed tariffs include a 25% tax on Canadian imported goods heading to the US and a 10% tax on Canadian energy products.

How will proposed US tariffs on Canada impact SMBs?

If these tariffs go into effect, they’ll likely result in:

Higher costs on imported goods and materials

Price increases as businesses offset rising production expenses

Supply chain disruptions, forcing companies to renegotiate with suppliers

Reduced demand for Canadian exports, as US buyers seek domestic alternatives

In the long run, this could lead to more nearshoring, diversified supply chains and a greater focus on local partnerships.

4 ways small businesses can get ready for US tariffs on Canada

Even if tariffs don’t happen, preparation is key. Here’s how Canadian SMBs can stay ahead:

1. Prepare for extended economic uncertainty

Review your expenses and cut non-essential costs. This might include:

At Float, we’re proud to support thousands of Canadian SMBs with financial tools that help them navigate uncertain times. Whether through improved expense management, efficient payment solutions, or financial insights for smarter decision-making, we’re here to ensure your business stays competitive and resilient.

Canadians use credit cards more frequently than any other payment method, and 57% say it’s because of the rewards they get for spending. If the perks are paying off for the average shopper, just imagine what Canadian businesses with more bills and buying power stand to gain from the benefits that come with corporate credit cards.

But not all corporate card programs are created equal. Selecting the right one requires a bit of research—and thankfully, we’ve done the legwork for you.

In this guide, we’ll break down everything you need to know about corporate credit cards in Canada: how they work, the perks and how to choose the best corporate card program for your start-up, scale-up or SMB.

What is a corporate credit card?

A corporate credit card, often called a corporate card or commercial card, is a card issued to employees to manage business expenses. Corporate cards typically offer more features than your average personal credit card, like higher limits, expense tracking, and enhanced reporting tools.

In Canada, the terms “corporate credit card” and “business credit card” are often used interchangeably, but there are a few key differences.

Business credit cards are suited for entrepreneurs, sole proprietors, or small businesses and require a personal credit check and guarantee. Think of these like an extension of your personal credit, where the card owner is held liable for the balance if the business can’t pay.

Corporate credit cards are for businesses with more spending power—like scaling start-ups or SMBs. They typically offer higher spending limits, automated controls and no personal guarantees (meaning you won’t need to risk your personal assets or credit to secure a card for your business).

Corporate cards are issued based on your business’s financial health rather than the applicant’s personal credit. (Note: they may also have other eligibility requirements). The company is responsible for paying the balance in full each month—not the “cardholder” or employee the card is assigned to.

What is a corporate card program?

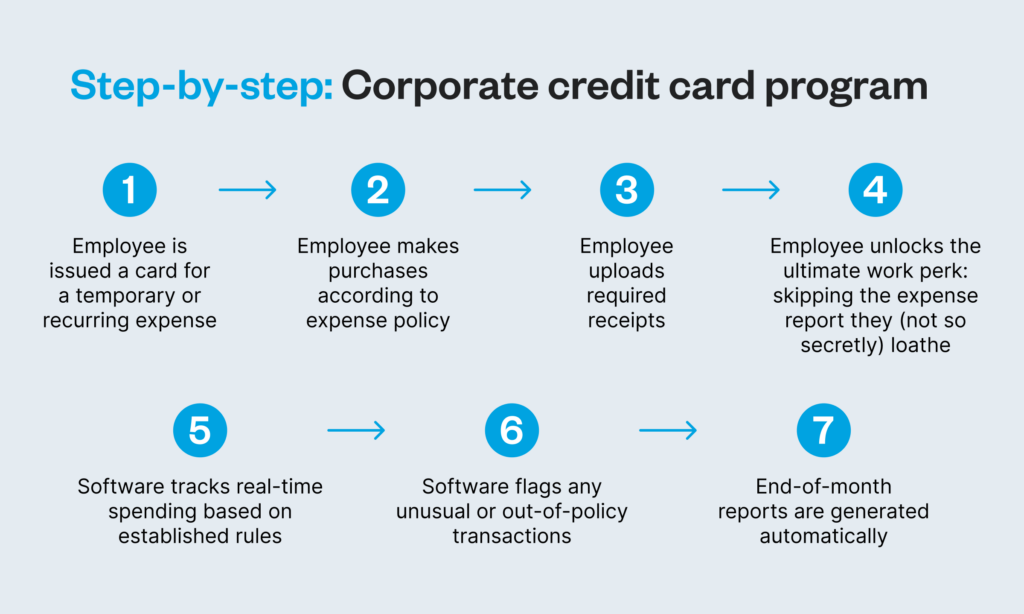

A corporate card program makes managing your business expenses faster and easier by bringing all credit spending into one place.

Here’s what to think about when building your corporate card program:

1. Issuance and eligibility

Full-time employees who regularly manage expenses—like client lunches, travel or team purchases—can benefit the most. For contractors or temporary staff, set clear guidelines on if and how they can use a card.

2. Types of charges

Spell out exactly what your corporate cards can be used for. Whether it’s travel, software subscriptions or team events, a clear expense policy helps your employees know how to use the card appropriately.

3. Responsibility for payments

With corporate cards, your business handles payments—not the employees. This takes the pressure off your not-so-finance-savvy teammates while giving whoever pays the bills complete visibility and control over spending.

4. Credit limits and policies

Set limits that match the needs of your team. For example, you might have higher limits set for frequent travelers or decision makers. Use tools like category-specific caps or single-use virtual cards for added security and flexibility.

5. Reconciliation

Here’s the best part about corporate cards: you can finally say goodbye to chasing receipts and juggling spreadsheets.

With automated tools, employees can upload receipts instantly, so your finance team can track and approve expenses in real time. For employees, this removes the hassle of out-of-pocket payments and slow reimbursements.

Who offers corporate card programs in Canada?

Traditional banks

Canada’s major banks, such as RBC, TD and Scotiabank provide corporate credit cards that often include features like rewards programs and travel perks. These cards are well-suited for larger enterprises but may come with higher fees, lengthy application processes and less flexibility.

Modern fintech providers

Fintech companies have introduced a new generation of corporate card solutions designed for more flexibility. These programs often prioritize ease of use, offering tools like virtual cards, automated expense tracking, and accounting integrations. Some providers (like Float) focus specifically on Canadian businesses, offering options like CAD and USD card limits with lower fees and faster approval processes.

Canada’s major banks, such as RBC, TD and Scotiabank provide corporate credit cards that often include features like rewards programs and travel perks. These cards are well-suited for larger enterprises but may come with higher fees, lengthy application processes and less flexibility.

Modern fintech providers

Fintech companies have introduced a new generation of corporate card solutions designed for more flexibility. These programs often prioritize ease of use, offering tools like virtual cards, automated expense tracking, and accounting integrations. Some providers (like Float) focus specifically on Canadian businesses, offering corporate card options like CAD and USD card limits with lower fees and faster approval processes.

Types of corporate credit cards

Corporate credit cards

Corporate cards or corporate credit cards are your versatile, all-purpose cards designed to cover a wide range of business expenses and day-to-day operational costs. They’re a great option for businesses looking for a straightforward way to manage spending without focusing on special categories.

Charge cards require the full balance to be paid off at the end of each billing cycle, making them ideal if your business wants to maintain disciplined spending habits. With higher spending limits than traditional credit cards, they’re great if your company is growing or has variable cash flow. If you plan on spending a minimum of $10,000 per month and want to pay it off quickly, a charge card could be for you.

Purchasing cards (P-cards)

P-cards are built for procurement and vendor payments and eliminate the need for traditional purchase orders or invoices. These cards simplify tracking vendor-specific expenses, reduce paperwork and ensure spending stays within your allocated budgets.

Travel and entertainment (T&E) cards

T&E cards are designed for travel-related expenses like flights, hotels, car rentals, and client dinners. They often come with travel perks like discounted rates, travel insurance and airport lounge access, making them handy for sales teams or frequent travelers.

Virtual cards

Perfect for online transactions, virtual cards offer added security and flexibility to your business. These digital-only cards are ideal for managing subscriptions, one-off purchases or vendor payments online.

Using a virtual card platform, your accounting team generates a single-use card customized with a specific spending limit and assigns it to an individual employee or vendor. This limited nature minimizes the risk of fraud and is especially useful for recurring expenses.

Ghost cards are assigned to vendors, projects or departments rather than individuals. They help your business track spending by budget or recurring expenses, offering an easy way to monitor compliance and streamline reconciliation.

Fleet cards

Designed for companies with vehicles, fleet cards manage fuel, maintenance, and other vehicle-related costs. They often include fuel discounts, detailed reporting on mileage and consumption, and tools to track vehicle expenses with ease.

Expense management cards

Expense management cards combine payment functionality with integrated tracking and approval workflows. They can reduce the time your finance team spends on reconciliation by syncing directly with accounting software.

Prepaid corporate cards

Unlike traditional credit cards, prepaid corporate cards require you to load funds onto the card upfront instead of borrowing from a bank. This gives your business more control over expenses while helping you avoid debt. Explore the prepaid business credit card Canada’s businesses love.

Types of corporate credit cards comparison chart

Top 4 benefits of corporate cards

1. Take back time with automated workflows

Corporate cards eliminate the hassle of managing paper receipts and processing reimbursements. With real-time tracking and automated expense reporting, your finance team will save hours on admin.

For start-ups and SMBs operating with lean resources, this means your staff spends less valuable time sorting through expense reports. For mid-market companies, finance teams will appreciate the ease of categorizing expenses without chasing receipts from hundreds of employees each month.

2. Drive smarter decisions with better cash flow

Corporate cards provide better visibility into company spending, allowing you to track it in real time and set individual limits. This is especially beneficial for start-ups and scale-ups diligently managing cash flow in the early stages of growth when budgets can be tight.

3. Save more and earn rewards

Many corporate card programs offer rewards, such as cashback, travel benefits, or discounts on essential services. At Float, we help businesses save an average of 7% on their spend through a combo of rewards like 1% cashback, 4% interest on deposits, no foreign transaction fees with our USD cards and employee time savings. We call that a win.

4. Control your capital by building credit

Building credit is vital for growth. For start-ups, corporate cards grant you access to higher business credit card limits without personal guarantees, creating a strong foundation for future financing opportunities. For larger SMBs and mid-market companies, you can strengthen your credit position to access larger credit lines as you scale.

Risks to be aware of

Security and fraud: Stats show Canadian businesses experience a higher rate of fraud (20%) than Canadian consumers (13%). Make sure to look for features like virtual cards for one-time purchases, transaction alerts and the ability to freeze a card instantly if something seems off.

Compliance headaches: Keeping track of expenses and ensuring they align with tax regulations can get complicated. Automate tracking and reporting to simplify these operations, giving you peace of mind and making tax season less stressful.

Overspending: Without proper limits, it’s easy for spending to spiral. Set clear boundaries with spend limits and restricted categories so you’re always in the driver’s seat.

Confusion: Sometimes, employees simply don’t know the rules. A quick onboarding session or a set of clear expense guidelines can make all the difference and keep everyone on the same page.

When you choose a corporate card program with smart controls and built-in security, you can enjoy all the perks without the headaches.

How to choose the right corporate card

Currency: If your business operates across borders, look for a card that supports CAD and USD spending without high foreign transaction fees. For example, Float avoids conversion fees by linking directly to your CAD or USD bank account, while cards like the RBC Avion Visa Infinite Business focus solely on Canadian spending.

Fees: High annual fees can eat into your budget, so consider whether the benefits outweigh the cost. Float has no annual fees, while traditional cards like the AMEX Business Platinum charge upwards of $799 annually, offering premium travel perks in return.

Rewards: Cashback and point-based systems are common, but the value of these rewards can vary. Float offers unlimited 1% cashback on all spending, while cards like the Scotiabank Momentum for Business Visa provide 3% cashback on specific categories like office supplies.

Features and controls: Real-time expense tracking, virtual cards, and integrations with accounting tools can save your team hours of work. Float excels in this area, offering both physical and virtual cards with spending controls, while traditional banking options focus more on rewards.

The best card for you depends on your goals, spending habits, and priorities. For a detailed breakdown of what’s available, compare Canadian corporate cards here.

💡Pro tip:Startups looking for the best credit cards? Instead of flashy rewards and points, consider prioritizing features and controls that help you scale faster while keeping tight reins on spend.

Best corporate credit cards in Canada

Choosing the best business credit card Canada offers can help you streamline expenses, earn rewards, and maintain better control over your company’s finances.

Here’s a brief overview of the leading programs to make an informed decision:

Float: Offers no annual fees, unlimited 1% cashback, and advanced expense management tools with up to 7% savings on average.

Keep: Provides higher credit limits, up to 4% cashback rewards, and no fees.

Loop: Allows spending in multiple currencies with no foreign exchange fees.

Selecting the right corporate card comes down to how your business spends and other factors like your industry. For example, a Canadian e-commerce business often purchasing from US suppliers, might prioritize a card that doesn’t charge foreign transaction fees. Or, a marketing agency managing several online ad accounts might prioritize a card that tracks spending per client.

Once you’ve selected a corporate card and have confirmed you meet the qualifications, applying is quick and easy with most providers.

Gather your business info: You’ll need basic details like your company name, location, type, industry, registration documents and financial figures.

Verify identities: Provide ID for key shareholders or decision-makers, as required.

Gather financial documents: Some providers may ask for proof of income or financial statements.

Complete your application: Many fintechs offer online applications, while traditional banks might require more paperwork and in-person appointments. At Float, our fast online application only takes 10 minutes.

Get approved: Approval times vary—some cards are ready in 24 hours (like Float), while others take a few days.

Once approved, you can start issuing cards to employees and using your new corporate card program to simplify spending.

Best business credit cards

Compare top options, fees and benefits for Canadian companies.

Start by establishing clear policies that outline which employees will receive cards, set spending limits, and define approved expenses.

Next, take advantage of your provider’s tools to set up spending controls. Features like customizable limits, category restrictions, and virtual cards for one-off purchases help you keep expenses organized and transparent.

Once the program is set up, train your team on how to use it effectively. A quick overview of the guidelines, including how to upload receipts and manage expenses, will set them up for success.

Finally, monitor spending using real-time reporting tools. This allows you to spot trends, adjust limits, and refine your policies to better fit your business as it changes.

Float offers Canadian businesses a smarter, simpler way to manage spending. With no annual fees, unlimited 1% cashback on every dollar spent and tools like real-time tracking and virtual cards, Float puts you in control of your finances.

Unlike traditional corporate credit cards, Float corporate cards provide high spending limits with no personal guarantees, making it easier to grow without the stress of added liability. You’ll also earn 4% interest on funds held in Float and enjoy a seamless onboarding process that gets you started in as little as 24 hours.

Growth Equity at Goldman Sachs Alternatives leads this funding round of over CAD$70M, joined by other prominent investors including OMERS Ventures, FJ Labs, Garage Capital and Teralys.

With the CAD$50M credit facility announced in February 2024—bringing total funding to over CAD$120M in the past year—this investment highlights Float Financial’s significant potential despite economic uncertainty.

Float will use the money to accelerate its product expansion, continue to attract top talent and expand its leadership in the Canadian market coast-to-coast.

TORONTO, Jan 13, 2024 — Float Financial, a business finance platform for Canadian businesses, today announced it has signed a CAD $70 million Series B financing round, which brings its total funds raised in the last 12 months to $120 million. The round is led by Growth Equity at Goldman Sachs Alternatives, with participation from OMERS Ventures, FJ Labs, Teralys and existing investor Garage Capital. Float’s range of business finance products is already trusted by big Canadian brands like Jane Software, LumiQ, Knix and more.

Float brings much-needed change to how Canadian businesses of all sizes spend, save and grow their money with a combination of innovative financial services and software. Since their November 2021 Series A, Float has seen 45x growth in total payment volume (TPV), 50x revenue, 30x increase in assets under management (AUM) and 140x expansion in credit issuance—all while achieving top quartile performance in capital efficiency. Float’s Series B investment round demonstrates its significant potential, with a higher valuation compared to its Series A, despite macroeconomic uncertainty.

In 2024, Float significantly expanded its expense management software and corporate cards offering to streamline how Canadian businesses manage their finances. With the addition of features to automate accounts payable, make reimbursements frictionless and surface real-time insights into company spending, Float helps businesses simplify their financial operations. Float now also offers virtual and physical cards in both CAD and USD, high-yield accounts and next-day fund transfers and payments, providing faster, more flexible alternatives to traditional banking services. The company plans to leverage the new capital to further broaden its product suite, attract top talent and expand its leadership in the Canadian market.

“Our financial system needs to match the speed and ambition of Canadian businesses if we want to thrive locally and compete globally. Float’s mission is simple: cut through the red tape and give businesses the financial tools they need to move faster. To access more opportunities. And to do it all easily, with the click of a button,” said Rob Khazzam, CEO of Float. “Today, 4,000 businesses use Float to manage team spend, earn high-interest on cash reserves and save days of manual reconciliation. This investment will fuel our mission to support thousands more with the financial solutions they need to lead Canada into the future.”

“Float’s impressive growth so early on is a testament to its Canadian focus, customer-centric platform and deeply committed team,” said Clare Greenan, an investor with Growth Equity at Goldman Sachs Alternatives. “We are thrilled to support Float in its next phase of expansion, as it makes innovative business finance solutions more accessible to Canadian businesses.”

In February 2024, Float secured a $50 million credit facility in partnership with Silicon Valley Bank (SVB), a division of First Citizens Bank. Existing venture capital and institutional shareholders from Series A, including Golden Ventures, Susa Ventures, and Tiger Global, demonstrated their confidence in Float’s future by remaining fully invested.

About Float Financial

Float is complete business finance for Canadian companies. We offer modern financial services, powerful software and industry-leading support designed for every company and stage of growth. Our integrated suite of products—including corporate cards, bill pay, expense management and high-yield accounts—gives finance teams everything they need to manage spending and cash flow efficiently, so they can keep pace with the demands of their business. To learn more, visit floatfinancial.com.

About Growth Equity at Goldman Sachs Alternatives

Goldman Sachs (NYSE: GS) is one of the leading investors in alternatives globally, with over $500 billion in assets and more than 30 years of experience. The business invests in the full spectrum of alternatives including private equity, growth equity, private credit, real estate, infrastructure, sustainability, and hedge funds. Clients access these solutions through direct strategies, customized partnerships, and open-architecture programs.

The business is driven by a focus on partnership and shared success with its clients, seeking to deliver long-term investment performance drawing on its global network and deep expertise across industries and markets.

The alternative investments platform is part of Goldman Sachs Asset Management, which delivers investment and advisory services across public and private markets for the world’s leading institutions, financial advisors and individuals. Goldman Sachs has more than $3.1 trillion in assets under supervision globally as of September 30, 2024.

Since 2003, Growth Equity at Goldman Sachs Alternatives has invested over $13 billion in companies led by visionary founders and CEOs. The team focuses on investments in growth stage and technology-driven companies spanning multiple industries, including enterprise technology, financial technology, consumer and healthcare.

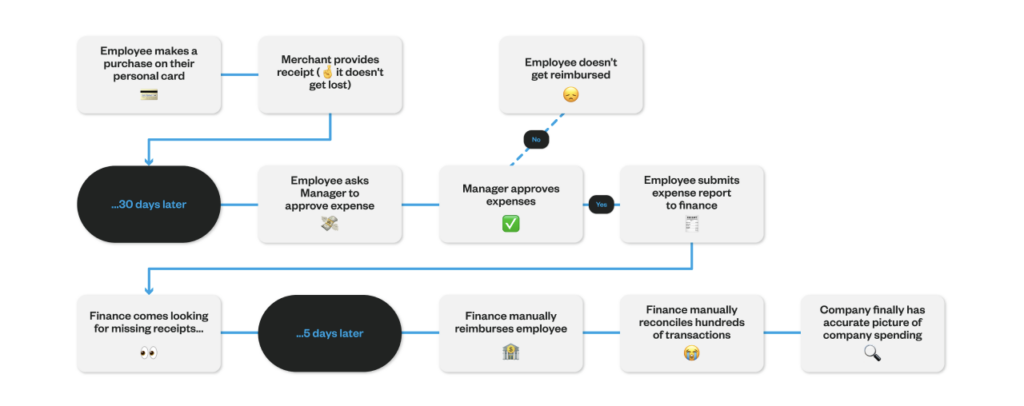

A company expense policy is critical for staying on budget, preventing expense fraud and establishing reimbursement processes. At most companies, however, these important documents for an overhaul. Here’s why.

Traditional company expense policies often use unclear wording that’s laden with financial jargon. They can also be tied into complex manual processes that rely on email or even interoffice mail, involve multiple stakeholders and result in meandering paper trails.

For employers and finance departments, these processes come with reduced insight into the company’s current financial standing—and an increased risk of fraud. According to a recent report by the Association of Certified Fraud Examiners (ACFE), companies lose an average of $251,000—and those massive losses can go undetected for up to 18 months.

Traditional reimbursement policies also include a lot of hidden administrative work. Recent reports show that on average, 19% of expense reports contain errors, which costs a business time and money to correct. In fact, annual processing costs can exceed $500,000. That includes the costs of correcting errors—a task that the average business spends more than a staggering 3,000 hours on every year.

What this spending and reimbursement process looks like with a traditional expense policy and manual/paperwork.

But employers aren’t the only ones who lose time and money due to inefficient expense policies. According to Forbes, 2 in 5 employees have had their cash flow impacted by lengthy and inefficient reimbursement processes, which can significantly impact morale, leading to higher employee churn and lower productivity. All of these concerns can be addressed by creating a modern expense policy that’s designed to help companies maintain control over budgets while also driving growth.

But what does a modern expense policy look like?

In this article, we’ll answer key questions like:

What is an expense policy?

What are the benefits of a modern expense policy?

What types of expense policies exist?

What are the key components of a modern expense policy?

How do I create a modern expense policy?

What are the best practices for enforcing company expense policies?

What is an expense policy?

A company expense policy (also known as a reimbursement policy) is a set of clear expense-related guidelines created by the business owner, operator or finance team. The policy outlines which business expenses are eligible for reimbursement, how employees should submit those expenses for approval and the steps to resolve disputes. This kind of policy ensures consistency, transparency and compliance in expense management.

What are the benefits of creating a company expense policy?

When a strong expense policy is in place, everyone wins.

For companies, the benefits can include:

Efficiently controlled company-wide spending

More accurate spending forecasts

Standardized rules for expense management

Fewer non-compliant expenses and a reduced risk of fraud

Less administration time spent evaluating spend requests

For employees, the advantages are:

Access to clear information on what is reimbursable and what is not, so they can make informed decisions quickly

No unnecessary reimbursement delays or refusals

Reduced administrative workload thanks to a clear and streamlined reimbursement process

Increased morale and reduced frustration, improving general engagement and satisfaction

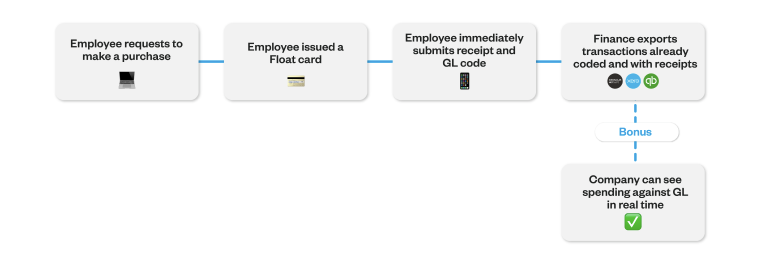

What this process looks like with a modern expense policy and automation.

Overall, an expense policy helps finance departments follow expense management best practices, improves transparency and clarifies expectations.

Key expense policy components

Although company needs and processes differ, several key components appear in most expense reimbursement policies. These include:

Expense categories

These outline the different types of expenses that employees can incur, so they don’t accidentally make a business purchase they can’t be reimbursed for. Categories may include travel, meals, accommodations, or office supplies. (That means Brian’s daily latte habit probably isn’t making the cut).

Spending limits

Each expense category should include clear limits that identify the maximum amount employees can spend without additional approvals. This helps prevent anyone from accidentally over-spending on business expenses.

Reporting and approval

Good expense policies clearly outline the steps employees must follow for expense pre-approval and reporting. This includes access to any required documentation.

Documentation requirements

Listing any supporting documents (like receipts or invoices) that employees will need to submit with their expense reports is a must. When this information isn’t outlined up-front, people are more likely to misplace necessary documents, creating friction when it’s time to submit their report.

Reimbursement procedures

This is a step-by-step outline explaining the process employees need to follow when submitting expense reports. This section also includes information on required forms or software systems.

Non-reimbursable expenses

This component clearly details expenses that are not eligible for reimbursement—for instance, personal expenses, fines or alcohol. (That “team building” round of margaritas won’t be going on the company tab).

Travel and accommodation guidelines

Like many employers, your business may have preferred provider arrangements with flight companies, hotels, rental cars and more. These guidelines provide these details, plus any additional travel-related policies that may impact reimbursement.

Expense audit and compliance

This section explains how expense reports are audited, and explains what can (or will) happen if expenses or reports do not comply with the expense policy.

How to write a company expense policy

Now that you understand the basics of company expense policies, here’s a step-by-step process (with real-world expense policy examples) you can follow to build one of your own.

Once you’ve had time to think through all the components you want to include in your expense policy, we’ve got you covered with our free Expense Policy Template.

Step 1: Gather information

Good expense policies are carefully designed to meet the needs of a company’s culture, industry, and existing processes. That means before you begin building your policy, you’ll need to do a baseline assessment. Take time to consider:

How your budget will impact your expense policy and vice versa

Whether or not there are any specific stipulations you’d like to add to support your mission, values and culture

The needs and desires of your employees (Do they need quick reimbursements? Flexible travel options?)

Remember to include other stakeholders in these considerations. Talk to your company’s financial experts and the employees who are most likely to use this policy to gain a more holistic understanding of how to meet everyone’s needs—and any barriers that might be in the way.

Example:You run a tech start-up where employees travel frequently for networking events. In this scenario, you may want to streamline the expense process by allowing staff to book economy flights without pre-approvals, or fast-tracking reimbursements with automated reimbursement solutions.

Step 2: Define eligible expenses