Filing small business taxes for the first time in Canada can feel like stepping into a maze—full of rules, forms and deadlines. If you’re a new entrepreneur trying to figure it all out, you’re not alone, and you’re definitely not the first to Google, “how to file business taxes in Canada.”

In this guide, we’ll walk you through everything you need to know to file your business taxes in Canada for the first time—from key dates to tax rates, to the tools that make it easier. With the right information and a step-by-step approach, you can file your small business taxes confidently, avoid costly mistakes and maybe even spot a few ways to save.

Important dates for filing small business taxes in Canada

When it comes to taxes, timing matters. Missing a deadline can lead to penalties, interest charges or unnecessary stress. Here are the key tax dates every small business owner in Canada should keep in mind:

Personal tax deadline (for sole proprietors and partnerships)

Due: April 30

If you operate as a sole proprietor or in a partnership, your business income is reported on your personal tax return. That means your return is due by April 30.

You technically have until June 15 to file, but any taxes owed must still be paid by April 30. Filing late, even if you don’t owe anything, can trigger interest charges if payment is delayed.

Corporate tax deadline (for incorporated small businesses)

Due: Six months after your fiscal year-end

If your business is incorporated, your T2 corporate income tax return is due six months after your fiscal year-end. For example, if your fiscal year ends on December 31, your filing deadline is June 30.

Keep in mind: For any Canadian-controlled private corporation (CCPC), any taxes owed are still due three months after your fiscal year-end, regardless of your filing deadline. Late payments may result in interest and penalties. If you’re not a CCPC, the timeline shortens to two months.

Sophie Dillon is a co-founder at Orbit Accountants, an accounting firm specializing in bookkeeping, tax, payroll, and fractional CFO services for SMEs. “If you owe more than $3,000 in corporate income tax, the CRA may require you to start making installment payments the following year,” says Sophie. “These prepayments help spread out your tax burden and avoid interest charges.”

GST/HST filing deadlines

If your revenue exceeds $30,000 in a 12-month period, you’re required to register for a GST/HST number and begin collecting and remitting sales tax.

Your GST/HST return deadline depends on how frequently you file:

- Annually: three months after your fiscal year-end

- Quarterly: one month after each quarter-end

- Monthly: one month after each month-end

If you’re just filing for the first time, you will file GST/HST at the end of your first fiscal year.

Understanding your business structure and tax obligations

Before you can file your taxes, you need to understand how your business structure affects what you owe and how you file. In Canada, there are three main types of business structures:

Sole proprietorship

This is the simplest business structure and the most common for first-time entrepreneurs. You and your business are considered the same legal entity, which means:

- You report business income on your personal tax return (T1) using Form T2125

- You pay tax at your personal income tax rate

- You may also need to pay Canada Pension Plan (CPP) contributions on your net self-employment income

Partnership

A partnership is similar to a sole proprietorship but involves two or more people. Each partner reports their share of the business income or loss on their personal tax return. You’ll need to:

- File a Partnership Information Return (T5013) if the partnership meets certain criteria (like having more than $2 million in assets or revenue)

- Report your share of income using Form T2125

- Pay taxes at your personal income tax rate

Corporation

A corporation is a separate legal entity from its owner(s), which means it files its own tax return (T2) and pays taxes at corporate rates. If you’re incorporated, you’ll need to:

- File a T2 Corporate Income Tax Return annually

- Pay tax at the small business tax rate in Canada if you qualify for the small business deduction (more on that in the next section)

- File and remit payroll taxes, GST/HST, and possibly T4s for any employees or shareholders

“Even if you’re the 100% shareholder, your corporation is a separate legal entity in the eyes of the CRA. That means filing a T2 return for the business, on top of your personal taxes,” says Sophie.

Your structure impacts not just how much you pay in taxes, but also how you manage cash flow, pay yourself, and take advantage of deductions. Choosing the right one from the start (and understanding what it means at tax time) sets you up for success.

Step-by-step guide to filing small business taxes in Canada (for corporations)

If you’re running an incorporated small business, your tax responsibilities are more involved than those of a sole proprietor—but with the right process, they’re totally manageable.

Here’s a step-by-step breakdown of how to file small business taxes in Canada as a corporation:

Step 1: Know your fiscal year-end

Your corporation’s fiscal year can be any 12-month period, but most small businesses align it with the calendar year (ending December 31). This date determines your tax deadlines, including when your T2 return and payments are due.

Step 2: Gather your financial records

Before you can file, you’ll need accurate, up-to-date financial records. This includes:

- Profit and loss statements

- Balance sheets

- Payroll records

- Receipts for expenses

- Bank and credit card statements

- Records of dividends or shareholder payments

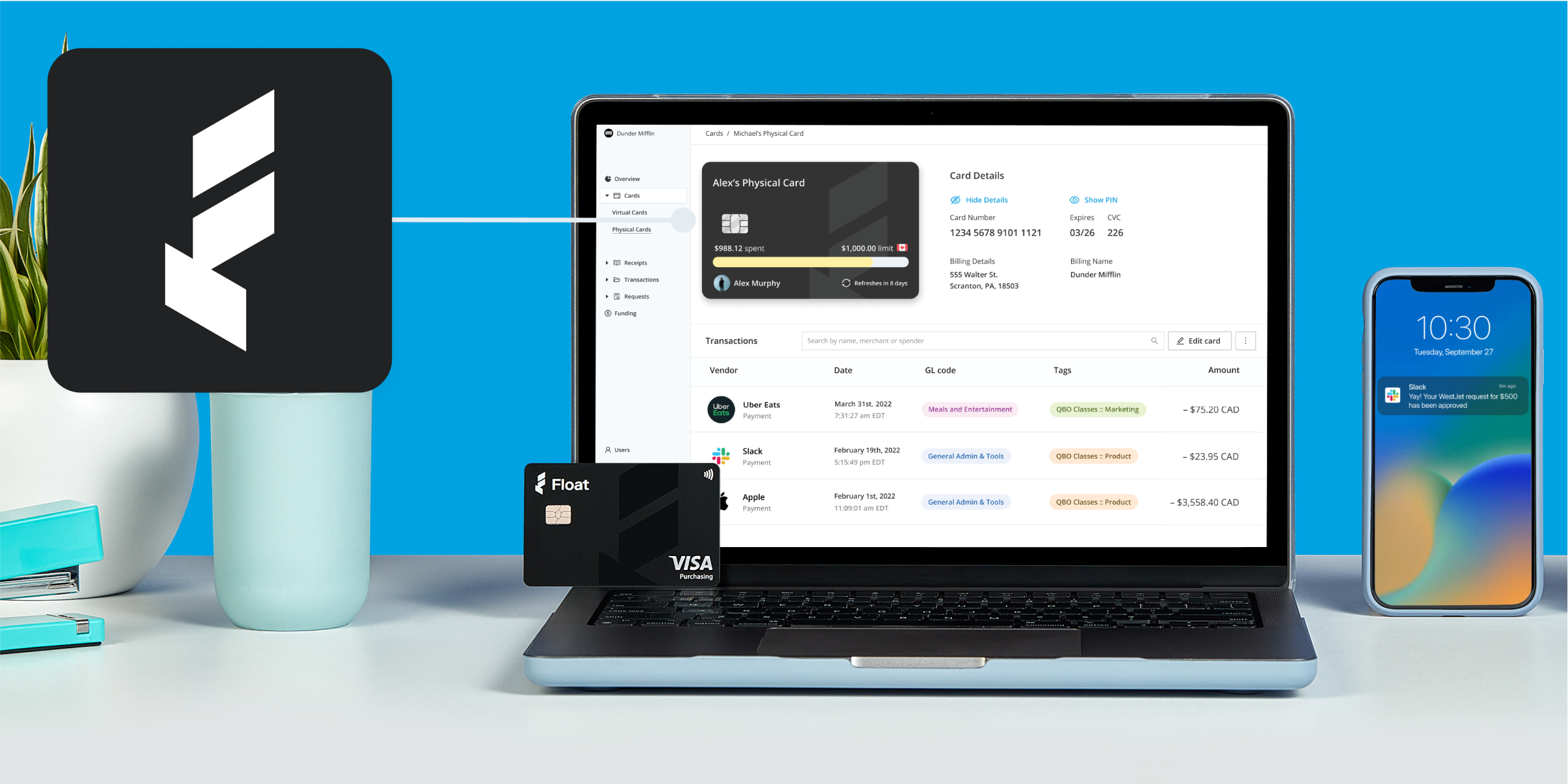

If you’re using accounting software, or an integrated platform like Float to manage expenses and receipts, this step is a lot easier.

Step 3: Prepare your T2 corporate tax return

The T2 return is the form all corporations in Canada must file. It includes detailed financial information, business activities and tax calculations. Even if your business doesn’t owe any tax, you still have to file a return. Most businesses also need to complete a General Index of Financial Information (GIFI) to report financial data.

Unless you’re a tax expert or your business is very simple, most incorporated businesses work with an accountant to file their T2 accurately.

Step 4: Claim your deductions and tax credits

Corporations can deduct eligible business expenses—everything from salaries to office supplies—to reduce taxable income. Depending on your industry and situation, you may also be eligible for federal or provincial tax credits.

Your accountant can help identify what you qualify for, but common deductions include:

- Business-related travel and meals

- Salaries and wages

- Utilities and rent

- Software subscriptions

- Professional services (legal, accounting, etc.)

Step 5: File electronically through CRA

Corporations are required to file their T2 return electronically using CRA-approved tax software. Most accountants and tax professionals handle this for you, but it’s important to confirm the return has been submitted on time.

Step 6: Pay any taxes owed

Even if you’re not filing your return right away, corporate income taxes are due within three months of your fiscal year-end. Payments can be made through your financial institution, via your CRA My Business Account, or using pre-authorized debit.

If you expect to owe more than $3,000 in taxes annually, you may need to make monthly or quarterly installment payments the following year.

Understanding small business tax rates in Canada

One of the benefits of incorporating in Canada is access to lower corporate tax rates, especially if your business qualifies as a CCPC. But understanding how those rates actually work is key to managing cash flow and staying compliant.

The small business deduction

Most incorporated small businesses in Canada qualify for the small business deduction (SBD), which reduces the amount of tax you pay on your first $500,000 of active business income. To qualify, your business must be:

- A Canadian-controlled private corporation (CCPC)

- Earning active business income (not investment income or capital gains)

- Operating primarily in Canada

With the SBD, your combined federal and provincial tax rate on the first $500,000 of income can be as low as 9% to 15%, depending on your province or territory.

General corporate tax rate

Once your income exceeds the $500,000 threshold, or if you don’t qualify for the SBD, you’ll pay the general corporate tax rate, which is higher. Federally, that rate is 15%, plus a provincial portion that varies. Combined, you’re looking at rates between 25% and 31% for most regions.

Passive income and investment income

Keep in mind that passive income (like rental income or interest from investments) is taxed at a much higher rate for corporations—often 38% or more. If your corporation earns significant passive income, it may also reduce your eligibility for the small business deduction.

Understanding which tax rates apply and how to stay within the lower brackets can have a huge impact on your bottom line. That’s where planning ahead with your accountant or tax advisor pays off.

Common mistakes to avoid when filing business taxes

Filing small business taxes for the first time in Canada comes with a learning curve. Here are some of the most common issues to watch out for, and how to avoid them.

Missing deadlines

Late filings or payments can result in penalties and interest charges. Remember:

- Your T2 return is due six months after your fiscal year-end

- Your payment is due three months after year-end

- GST/HST and payroll remittances have their own filing schedules

“One thing that trips up a lot of first-time filers is the difference between when your return is due and when your payment is due,” says Sophie. “Your T2 corporate return is due six months after your fiscal year-end, but any taxes you owe must be paid within three months if you are a CCPC with taxable income under $500,000. If you wait until the filing deadline and haven’t paid, you could already be late. It’s an easy detail to miss, but an important one.”

Mark these deadlines clearly, and consider setting calendar reminders or using software that helps automate due-date tracking.

Mixing personal and business expenses

If you’re not keeping business and personal spending separate, it’s harder to track deductions, and it could raise red flags with the CRA.

- Use a separate business bank account and credit card

- Keep detailed records and receipts for all expenses

- Don’t claim personal expenses as business write-offs

Tools like Float can help your team manage spending in real time and categorize expenses correctly from the start.

Not claiming all eligible deductions

Many small business owners underclaim because they’re unsure what qualifies. Commonly missed deductions include:

- Home office expenses (if you work from home)

- Using your vehicle for business purposes

- Software subscriptions and professional development

- Meals and travel for client-related activities

A good accountant can help you find legitimate deductions and stay within CRA guidelines.

Forgetting to track GST/HST

If you’re collecting GST/HST, you’re responsible for tracking it properly and remitting it on time. Mistakes like forgetting to remit, underreporting or claiming input tax credits incorrectly can lead to audits or penalties.

Not sure if you need to register yet?

Here’s how to know when it’s time to register for a HST number.

Filing manually or without support

In Canada, 44% of SMBs struggle with inefficient financial reporting processes. Mix in the fact that filing a T2 return is more complex than a personal tax return, trying to do it all manually—or without professional support—can lead to errors or missed opportunities. Save yourself the headache by investing in expert help or software that’s built for Canadian corporations.

Tools and resources to simplify tax filing

Accounting software

Digital accounting platforms are like a trusty sidekick when it comes to tracking income, expenses, and generating the reports you’ll need to complete your corporate tax return. Most allow you to automate repetitive tasks, categorize transactions, and share real-time financial data with your accountant or bookkeeper. Look for a system that fits your business size and integrates well with your other financial tools.

If you’re already using Float, our platform integrates seamlessly with these popular accounting platforms, so your financial data can stay accurate and up to date:

- QuickBooks Online – Ideal for small businesses managing day-to-day bookkeeping and cash flow.

- Xero – A go-to for startups and growing teams that need simple, collaborative accounting.

- NetSuite – Built for mid-market and enterprise companies with more complex financial operations.

CRA’s My Business Account

The Canada Revenue Agency’s My Business Account is your online hub for managing federal tax obligations. Through this portal, you can:

- File corporate income tax and GST/HST returns

- View account balances and notices of assessment

- Make payments or set up instalments

- Manage payroll accounts

- Authorize a representative (such as your accountant)

Registering for this portal early on gives you full visibility and makes it easier to stay compliant.

Receipt and expense tracking tools

Keeping accurate records is so important—not just at tax time, but all year round.

“One of the biggest mistakes we see is business owners scrambling at year-end to remember what expenses they had ten months ago or trying to chase down receipts. Tracking as you go makes a huge difference,” says Sophie.

Expense management tools can help your business:

- Capture and store receipts digitally

- Monitor spending in real time

- Categorize purchases for easier bookkeeping

- Create clear audit trails for deductions

The more automated and centralized your system, the easier it will be to prepare for filing and support your claims if you’re ever audited.

Professional support

Hiring a qualified bookkeeper or accountant is a worthwhile investment. They can help ensure your tax return is accurate, maximize deductions and guide you through installment payments or tax planning strategies. You’ll be thankful you did it in the long run!

How Float can help

Tax season might come once a year, but the systems you put in place today can make the process smoother every time. At Float, we help small businesses across Canada simplify financial operations and stay tax-ready all year round. With Float, you can:

- Eliminate the paper chase at tax time

- Keep business purchases organized and categorized

- Improve accuracy in your bookkeeping

- Make month-end and year-end processes faster and easier

- Support your accountant with the data they need, when they need it

Ready to make tax season stress-free? Book a demo or get started with Float to take control of your business spending today.

Learn more about Float

Get a 10-minute guided tour through our platform.

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. Every business is unique, and tax rules can change or vary depending on your specific circumstances. We recommend consulting a qualified accountant or tax professional to ensure you’re making the right decisions for your business.