Month-end close for controllers is a pressure point where speed and accuracy are expected to coexist perfectly. Leadership wants faster reporting. Auditors want precision. And finance teams are left to navigate manual reconciliations, scattered data and a narrowing window to deliver reliable numbers.

The issue isn’t effort—it’s the process. Spreadsheets, disconnected systems and reactive workflows create friction, costing teams valuable time tracking receipts, matching transactions and resolving discrepancies that could have been handled earlier in the month.

Accounting automation and real-time financial data can reshape month-end for controllers. By turning it from a last-minute scramble into a continuous, streamlined process, controllers get cleaner data, faster close cycles and more time for analysis rather than administrative work. Let’s talk about how automating month-end close helps controllers move faster without sacrificing accuracy, and what the best financial close processes can look like.

Why month-end close is a pain point for controllers

Month-end close squeezes some of the most critical finance work into a very tight timeline. Controllers are expected to hit deadlines, deliver accurate reporting and still keep the business moving, often with processes that were never designed for speed.

A significant part of the strain comes from manual data entry and reconciliation. When transactions live across bank portals, card statements and spreadsheets, finance teams spend hours matching numbers instead of analyzing them. Every manual touchpoint also introduces risk, whether that’s a missed receipt, a coding error or an incorrect entry that needs to be tracked down later.

Delayed spend visibility creates its own challenges. When expenses only become clear at the end of the month, reporting slows down, accuracy suffers and working capital is harder for controllers to assess. Teams are forced to work with incomplete information or wait for last-minute data to arrive, creating bottlenecks that stretch close timelines even further.

Add in disconnected systems and the process becomes even more fragmented. Data needs to be exported, reformatted and manually uploaded just to get a 2D view. This makes it harder to maintain consistency, verify accuracy and confidently sign off on the numbers.

The result is a close process that feels reactive rather than controlled. Instead of using month-end to interpret performance and guide future decisions, controllers are often focused on just getting through it, which is exactly where automation can create the most meaningful shift.

What a best-in-class month-end close process looks like for controllers

When your workflows, data, and team are aligned, the month-end close becomes a streamlined, repeatable process that keeps your entire finance function running smoothly.

Here’s what it looks like when it all comes together.

A continuous accounting mindset

A best-in-class close does not begin on the last day of the month. It runs continuously in the background, capturing, coding and reviewing transactions in real time. This reduces the end-of-month pileup and replaces the scramble with a steady rhythm that feels more controlled and more predictable.

Centralized real-time financial data

Financial data is always up to date and accessible. Controllers can see spending, approvals and outstanding items without relying on outdated exports or manual updates. This instant visibility creates confidence in the numbers and removes much of the guesswork that slows traditional close cycles.

Automated matching and reconciliation

Transactions and receipts are matched automatically as they flow in. This reduces manual entry, minimizes errors and shortens reconciliation timelines. Instead of tracking down missing documentation, finance teams can focus on validating the data that matters most.

Clear approval workflows and documentation trails

Every transaction follows a structured path. Approvals are consistent, audit trails are clear and documentation is complete. This ensures compliance readiness without adding complexity or slowing the process.

A shift from data entry to data interpretation

With the mechanics handled through automation, controllers can move their focus toward reviewing material transactions, analyzing performance and communicating results to leadership. The close becomes less about tracking down numbers and more about understanding what those numbers mean, which after all, is the job of a controller!

Key areas controllers can automate in the month-end close

To support an automated financial close, controllers should focus on month-end processes where automation reduces manual effort. These are the points in the workflow where small changes can have the biggest impact on speed, accuracy and oversight to streamline financial processes.

What does that automation look like?

It’s custom to each controller’s month-end close routine, but below are some areas you can automate to inspire you.

| Area to automate | What automation replaces | Impact on controllers |

| Transaction reconciliation | Manual line-by-line matching across bank accounts, corporate cards and AP systems | Faster reconciliation, fewer errors and significantly less time spent cleaning up data at month-end |

| Receipt collection and matching | Chasing employees for missing receipts and manually attaching documentation | Real-time receipt capture keeps transactions audit-ready and removes one of the biggest close bottlenecks |

| Spend approvals and policy enforcement | Email-based approvals or informal sign-offs that slow reporting | Pre-set rules and approval routing surface exceptions early and keep compliant transactions moving without friction |

| Vendor payment scheduling | Last-minute payments triggered under time pressure or incurring interest due to missed or delayed payments | Payment optimization creates predictable timing and clearer visibility into outstanding liabilities before reporting begins |

| Reporting and reconciliation workflows | Manual exports and spreadsheet manipulation | Faster access to accurate summaries, variance analysis and financial reports ready for review |

By automating these areas, month-end close becomes less about chasing data and more about validating it. Controllers gain cleaner numbers, smoother workflows, and the ability to focus on analysis and insight rather than repetitive administrative work.

Best practices for controllers to improve month-end close efficiency

A faster month-end close doesn’t come from working harder at the end of the month! It comes from building better habits and systems throughout it. These best practices help controllers reduce pressure, improve accuracy and create a smoother close every cycle:

Shift to continuous close workflows

Move as much work as possible out of the final days of the month. Capturing, coding, and reconciling transactions in real time prevents end-of-month pileups and keeps data close-ready at all times.

Standardize approval processes

Clear, consistent approval workflows reduce last-minute delays and confusion. When everyone follows the same process, transactions move faster and documentation stays complete.

Automate wherever possible

Use automation for receipt collection, transaction matching and coding to reduce manual entry and eliminate repetitive tasks that slow the team down.

Identify and review bottlenecks regularly

Take time each quarter to review where close slows down most, whether it’s missing receipts, slow approvals or delayed exports. Addressing these gaps early keeps the process improving over time.

Train teams on expectations and timing

Ensure employees understand when to submit receipts, how to code transactions and what documentation is required. Clear guidance reduces follow-ups and improves data quality.

Prioritize review over data entry

Structure the close so controllers and finance teams spend more time analyzing high-value transactions and less time preparing them.

All of these together and controllers can expect better control of their cash flow and make month-end even easier.

5 ways real-time financial data accelerates month-end close

To get to the dream state above, one of the biggest unlocks for controllers is access to real-time financial data.

After all, one of the greatest frustrations during month-end is working in the dark. When spend only fully reveals itself at the end of the month, controllers are left piecing together the story under tight deadlines. Real-time financial data, when managed through a solid financial close software, changes the experience entirely. Here’s how.

1. Fewer surprises when it matters most

With live visibility into transactions, controllers always know what’s already committed and what’s still outstanding. Say goodbye to last-minute scramble for missing information or unexpected expenses suddenly appearing during the close week.

2. Faster reconciliation with less friction

When data is current and continuously updated, reconciliation feels far less like detective work. Transactions are matched against accurate information, reducing the time spent correcting mismatches and hunting down details after the fact.

3. Issues surfaced before they become problems

Real-time insight makes it easier to spot missing receipts, unusual activity or out-of-pattern spend early. Instead of firefighting at the end of the month, controllers can course-correct as they go.

4. Clearer, more confident reporting

With reliable data throughout the month, preliminary reporting becomes far more accurate. Controllers can share updates with leadership knowing the final numbers won’t dramatically shift once close is complete.

5. More control under tight timelines

When close windows are short, having real-time data offers reassurance. Controllers can make informed estimates and move forward with confidence because spend is visible as it happens.

Float’s automation advantage: A faster, more controlled month-end close for controllers

Float supports a faster and more controlled month-end close for controllers by embedding automation directly into day-to-day finance workflows. Rather than waiting until the end of the month to reconcile scattered data, controllers can rely on a system that keeps transactions organized, coded and ready for review as they happen.

And although it can help with an automated financial close, Float is much more than financial close software. With Float, controllers gain access to practical automation that directly impacts their day-to-day.

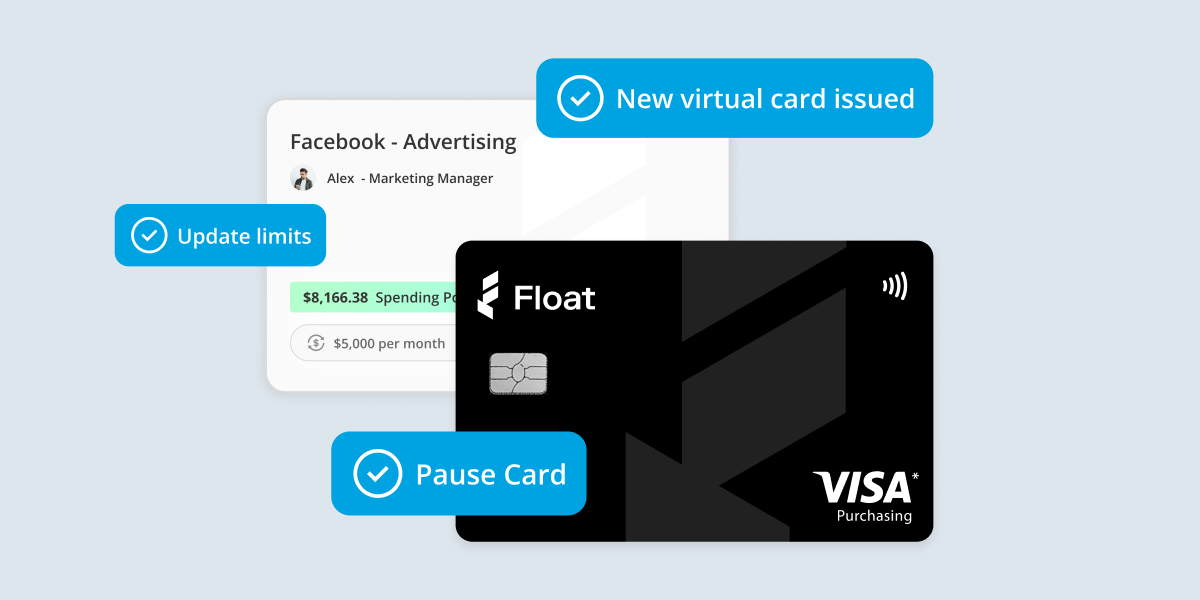

Live visibility into company spend

Having the right corporate card program is a game-changer for visibility. Every corporate card transaction and bill paid through Float appears in real time, giving controllers an up-to-date view of what has already been spent and what is still pending before month-end even begins.

Automatic receipt collection and attachment

Employees upload receipts directly in the Float app as soon as a purchase is made, with built-in prompts and reminders. For off-platform purchases, reimbursements can be submitted through Float with receipts and details captured in the same workflow. Each receipt is automatically linked to its corresponding transaction, removing the need to track people down during close.

Smart transaction coding

With intelligent accounting automations, Float suggests coding rules based on past behaviour and applies GL codes and tax categories automatically once those rules are set. This reduces manual data entry and ensures transactions are already categorized when exported to the accounting system.

Direct export to accounting software

Transactions that are already coded and matched with receipts are exported directly to accounts platforms like QuickBooks Online, Xero or NetSuite, eliminating the need for manual re-entry or custom spreadsheet uploads.

Preventive spend controls

Custom limits and approval policies ensure transactions stay within budget and policy. This prevents errors and misallocations from ever reaching the ledger in the first place.

By the time the close window arrives, the heavy lifting has already been done. Controllers can focus on reviewing higher-value items, validating financial performance and preparing reporting and insights for the leadership team.

Make expense management even easier

Streamline your business spending with automation tools built right into Float.

Turn month-end close into a strategic advantage

There’s a light at the end of the tunnel of month-end stress. With accounting automation, real-time visibility and continuous close practices in place, controllers can move from reactive clean-up to confident oversight. And Float helps you get there.

For controllers ready to modernize their month-end close, Float offers a practical path toward greater efficiency, accuracy and oversight. Because transactions are already approved, coded, and documented before month-end, close becomes a review and validation process, not a cleanup exercise.