Corporate Cards

Physical vs. Virtual Corporate Cards: Pros, Cons & Best Use Cases

Let’s break down the pros, cons and best use cases for virtual and physical corporate cards so you can take advantage of corporate card benefits.

May 27, 2025

As businesses grow and spend becomes more decentralized, the way teams manage expenses has to grow with it. One of the biggest shifts? Moving from plastic in your wallet to virtual numbers in your phone.

Virtual corporate cards are now a go-to for many finance teams, offering speed, security and control. But these aren’t entirely replacing physical cards! Those still have their place, especially for travel-heavy teams or in-person transactions.

So, which should your business be using and when?

Let’s break down the pros, cons and best use cases for virtual and physical corporate cards so you can take advantage of corporate card benefits.

What are corporate cards?

Corporate cards are company-issued payment cards that employees use for work-related purchases, from client dinners to SaaS tools and everything in between. Instead of reimbursing staff, corporate cards let teams pay upfront, giving finance teams visibility and control over spending.

Great expense management solutions use corporate cards as part of a bigger system that:

- Increases operational efficiency by reducing the time spent chasing receipts

- Improves accuracy by minimizing manual entry and error-prone spreadsheets

- Encourages responsible spending through clear budgets and rules

Today’s corporate cards typically include spend limits, transaction tracking and fraud protection. Some also offer extra features like instant card issuance and cashback rewards.

Virtual vs Physical Corporate Cards

There are two main types: virtual cards and physical cards. Let’s look at how each works.

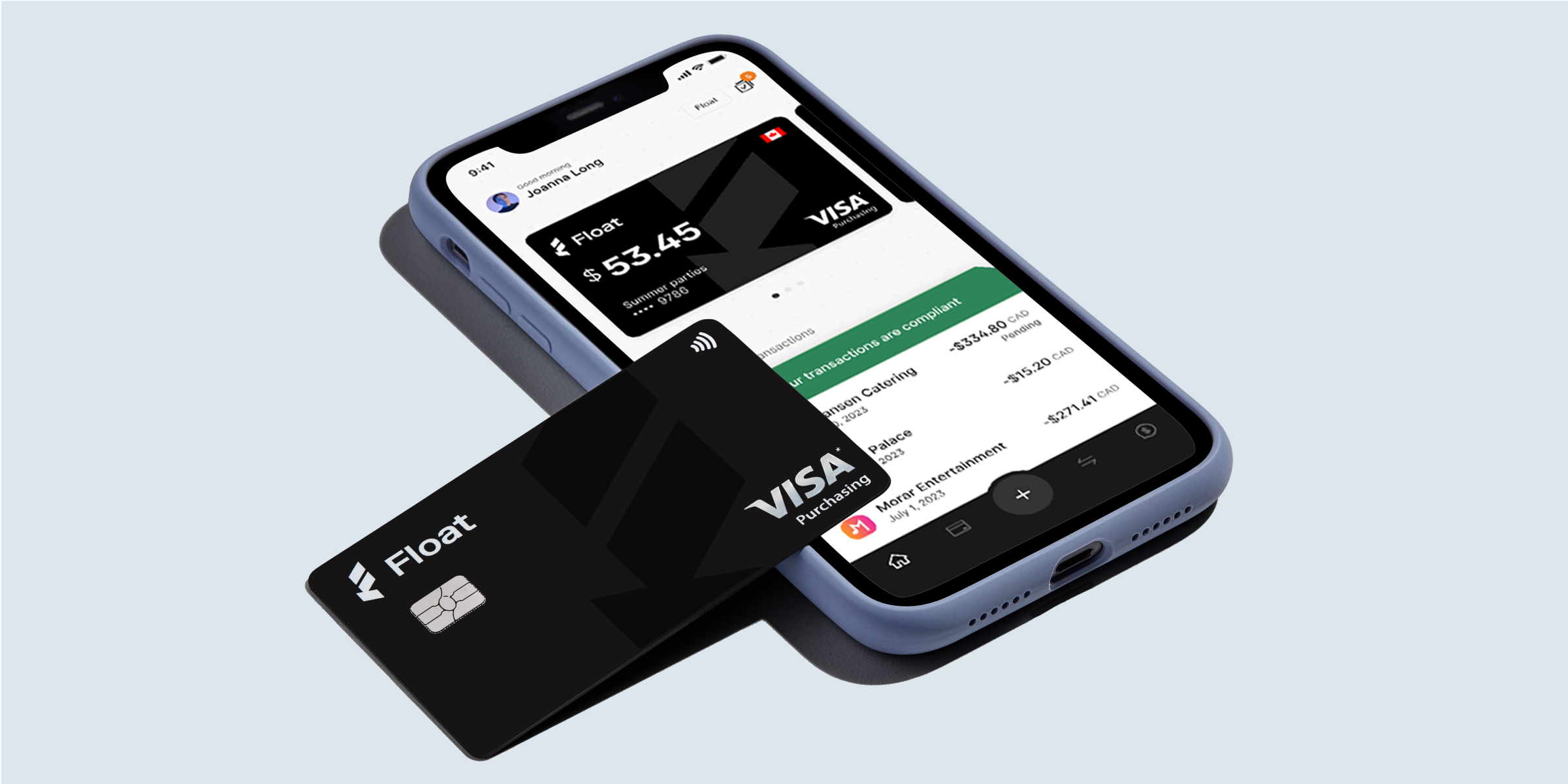

Virtual corporate cards

A virtual corporate card is a digital-only card that exists online. It has a card number, expiry date and CVV, just like a physical card, but there’s no plastic involved. You can generate one instantly, assign it to an employee or a vendor and start spending right away.

Virtual cards are especially useful because of how easy they are to control. You can create a single-use card for a vendor, set daily or monthly limits, block specific merchant categories or have the card auto-expire after a specific time period. If the card is compromised, you can freeze or delete it in seconds. You also generate a virtual replacement just as fast—no waiting weeks for cards to arrive in the mail.

Benefits of virtual corporate cards:

- Instant issuance and assignment

- Custom spend limits and expiration rules

- Better tracking by employee, team or vendor

- Higher virtual card security with less exposure to fraud

- No physical card to lose, steal or forget at home

“I only use physical card[s] for ATMs, and virtual for every other payment, unless I have absolutely no other choice. It’s safer, because I can block and create a new one any time in case something happens.” — Reddit user

Drawbacks to consider:

- Not accepted by all merchants for in-person purchases

- Can’t be used at ATMs

- Some employees may prefer the familiarity of a physical card

Virtual cards are ideal for managing online subscriptions, assigning budget-specific cards to marketing campaigns or vendors, and giving employees limited-use cards for purchases like software, training or equipment. They’re ideal for startups and digital-first teams that want scalable ways to control company spend.

Best business credit cards

Compare top options, fees and benefits for

Canadian companies.

Physical corporate cards

Physical corporate cards are the traditional plastic cards most are familiar with. They’re chip-enabled, tap-to-pay ready and can be swiped or inserted anywhere credit cards are accepted.

They’re ideal when a virtual card won’t cut it, like when employees need to travel, withdraw cash or pay at locations that don’t support digital wallets.

Benefits of physical corporate cards:

- More wide acceptance at stores, restaurants, hotels and ATMs

- Convenient for travel and day-to-day business spending

- Easy to use, especially for employees who prefer traditional options

- Some cards offer rewards like travel perks or cashback (though some virtual cards do too—like Float’s 1% cashback)

Common drawbacks:

- Cards can be lost, stolen or cloned

- Replacements take time to ship

- Without proper controls, they’re harder to monitor or restrict

That said, physical cards can offer great control when paired with platforms that let you set spend limits, block categories or track transactions in real time. With the right tools, you can get the best of both worlds: flexibility for your team and oversight for your finance team.

How to compare virtual and physical cards

Here’s a quick comparison of how the two card types stack up:

| Feature | Virtual cards | Physical cards |

| Format | Digital-only | Physical plastic |

| Use case | Online purchases, subscriptions, vendor payments | Travel, meals, and in-store purchases |

| Setup | Instant and self-serve | Requires shipping and activation |

| Security | Easy to control, freeze or delete | Higher risk if lost or stolen |

| ATM access | Not available | Available |

| Spend limits | Fully customizable | Depends on software integration |

| Ideal for | Digital teams, controlled budgets | Client-facing teams, travel-heavy roles, everyday spend |

Best use cases for each

The best setup isn’t always either-or. Depending on the situation, many companies benefit from using both card types.

Use virtual cards for:

- SaaS tools and cloud software

- Digital ad platforms

- Freelancer or vendor payments

- Employee-specific budgets (e.g. onboarding, training, home office)

Use physical cards when:

- Team travel, meals and conferences

- In-person client purchases or hospitality

- Office supply runs and vendor pickups

- Situations where ATMs or swipe terminals are required

For example, your marketing manager might have a virtual card for ads and a physical card for travel. This separation adds clarity and control for finance without slowing down the team.

By mixing card types and clearly defining usage rules, you can increase security, reduce confusion and streamline reconciliation.

How to choose the right corporate card solution

When building or upgrading your company’s business card usage, here are some tips to consider:

- Choose a provider that offers both virtual and physical cards

- Look for tools that allow you to set spend limits, restrict merchants and monitor usage in real time

- Make sure the cards connect with your accounting, ERP and HR systems

- The system should be simple for your team to understand and adopt

- Whether you’re onboarding one person or one hundred, it should take minutes, not weeks

Training also plays a key role. Make sure employees know which card to use and when, what expenses are covered and how to submit receipts or notes if needed. A quick guide or short onboarding video can go a long way.

A well-managed card program can unlock smarter budgets, faster processes and better decision-making across your business. All it takes is the right setup and the right tools to support it. Explore Float’s corporate card solutions today.

Try Float for free

Business finance tools and software made

by Canadians, for Canadian Businesses.

Written by

All the resources

Cash Flow Optimization

How to Make EFT Payments in Canada: Complete 2026 Guide

Learn how to make an EFT payment in Canada, avoid extra fees and move money faster in 2026 with modern

Read More

Expense Management

Expense Management System Implementation Guide for Canadian Businesses

Are manual expense processes getting you down? It might be time for an expense management system.

Read More

Corporate Cards

Procurement Cards vs. Corporate Cards: Which is Right for Your Business?

Let's break down how procurement cards and corporate cards work, where each one shines and how Float offers the flexibility

Read MoreSpend time and money

where it counts

Earn up to 3.5% interest on your cash balance and simplify business spending with corporate cards, accounts payable and expense management software.