No Annual Fee Business Credit Cards: A Smarter Way to Manage Spend

Using a traditional business credit card in a Canadian startup or SMB can feel a bit like trying to launch a rocket with a flip phone. It’s simply a mismatched tool for modern spend management.

With annual fees, limited operational and financial controls, and rigid credit requirements, these legacy cards slow down teams that need to keep up with their competitors. That’s why no-fee business credit cards are gaining traction: they give startups and scaling teams the agility, transparency and flexibility they need—without lighting their budgets on fire.

In this article, we’ll explore why a no-annual-fee business card is the right way to go and how to select the best no-annual-fee business credit card for your needs.

What are no-annual-fee business credit cards?

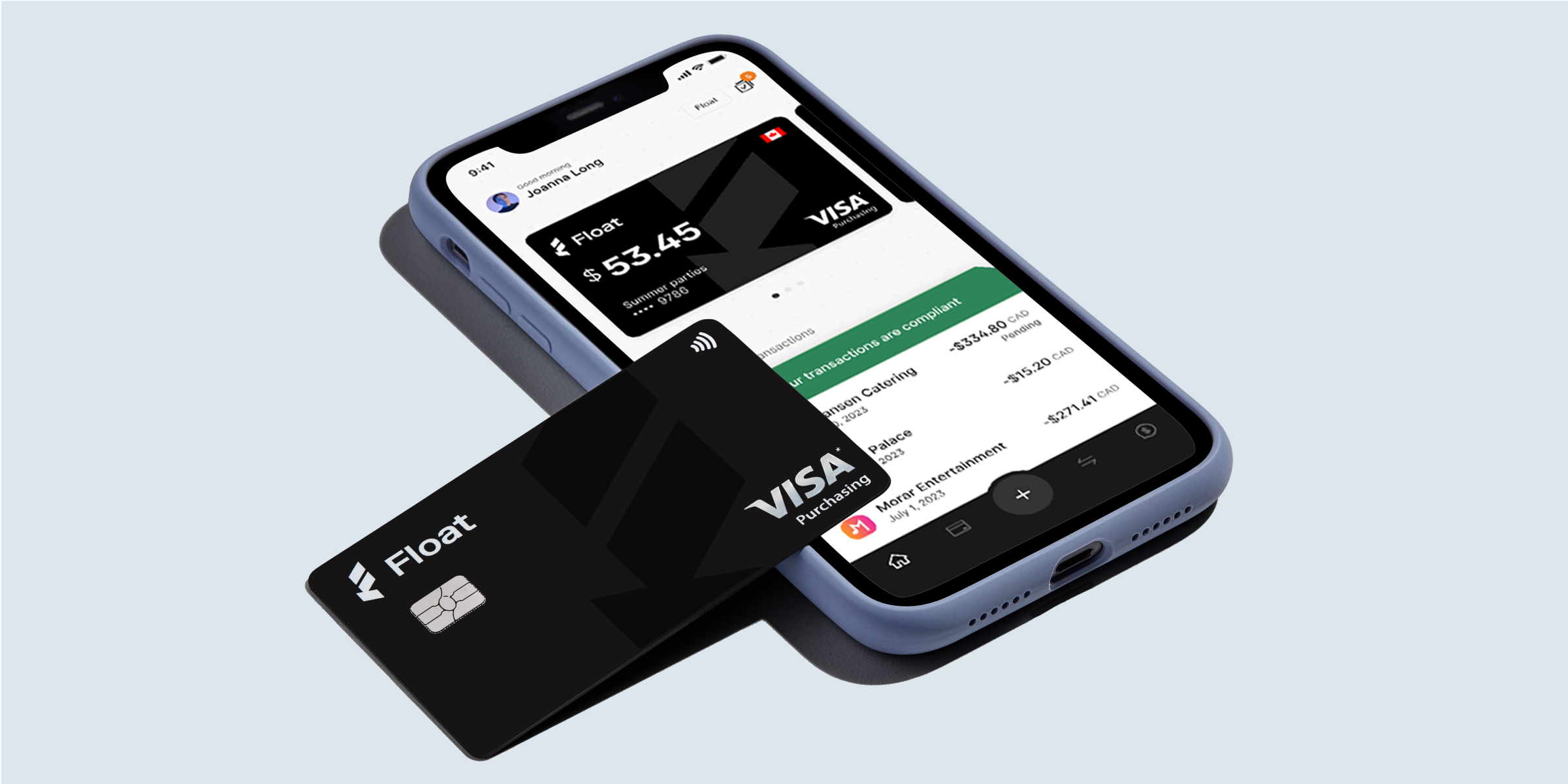

A no-fee business credit card, charge card or corporate card is a credit card that does not carry an annual cost. Issued in the business’s name—as opposed to the business owner or an individual’s name—no-fee business credit cards are available through banks, credit unions and fintech platforms like Float.

Some no-fee business credit cards require a personal credit check and guarantee, acting as an extension of personal credit for the business owner. Others don’t require any personal guarantees and come with higher spending limits and more automated controls. These types of cards are issued based on the company’s financial health.

Why go with a no-fee credit card?

There are plenty of business and corporate credit card options on the market, so why choose one with no annual fees? Here are just a few reasons:

- Keep your margins healthy: Recurring annual credit card fees, ranging from tens to hundreds of dollars, can eat into your margins. These savings matter for lean teams or those who are keeping a close eye on their budget.

- Only pay for what you need: Business credit cards with annual fees typically offer a lot of bells and whistles—many of which go unused, like access to specific airport lounges. Why pay for something you’ll never take advantage of?

- See the ROI: For most small and medium businesses, the return on investment rarely offsets the fee of the credit card. Instead of choosing a legacy corporate card with a hefty fee, opt for a modern solution like Float’s corporate card which has a $0 base cost. Float is one of the best no annual fee business credit cards in Canada because it doesn’t require a personal guarantee, doesn’t have interest charges and offers full built-in automation (all for $0 annually).

Best business credit cards

Compare top options, fees and benefits for

Canadian companies.

No-fee business credit card options

Several types of small business credit card options don’t charge an annual fee, many of which benefit startups and SMBs directly:

- Charge and prepaid cards: For Canadian businesses that want to give employees spending power without traditional debt, a charge or prepaid no-annual-fee business card is the way to go. Float’s corporate cards for small Canadian businesses offer a charge or prepaid funding model to provide a balance of flexibility and control.

- Cashback cards: If your business frequently purchases office supplies, software subscriptions, gas and other operational expenses, you might benefit from a corporate cashback card like the BMO CashBack Business Mastercard, TD Business Select RateTM Visa* Card or the TD Business Cash Back Visa* Card. Float’s corporate card also offers cashback rewards. These types of cards give you back a percentage of your spending (on certain items).

- Rewards cards: If you travel frequently for business, you can earn business credit card rewards like travel points and lounge access from rewards-based cards like the BMO AIR MILES® No-Fee Business Mastercard® or the RBC Visa CreditLine for Small Business.

- Combination business credit card and expense tools: Solutions like Float not only offer a no-fee business card that has cashback rewards, but also a number of consolidated services such as expense management tools and low foreign exchange fees.

Key no-annual-fee business credit card features to prioritize

Evaluating no annual fee business cards can feel like an overwhelming task, especially if you’re not sure what to consider. Here are the key features we recommend Canadian businesses pay attention to:

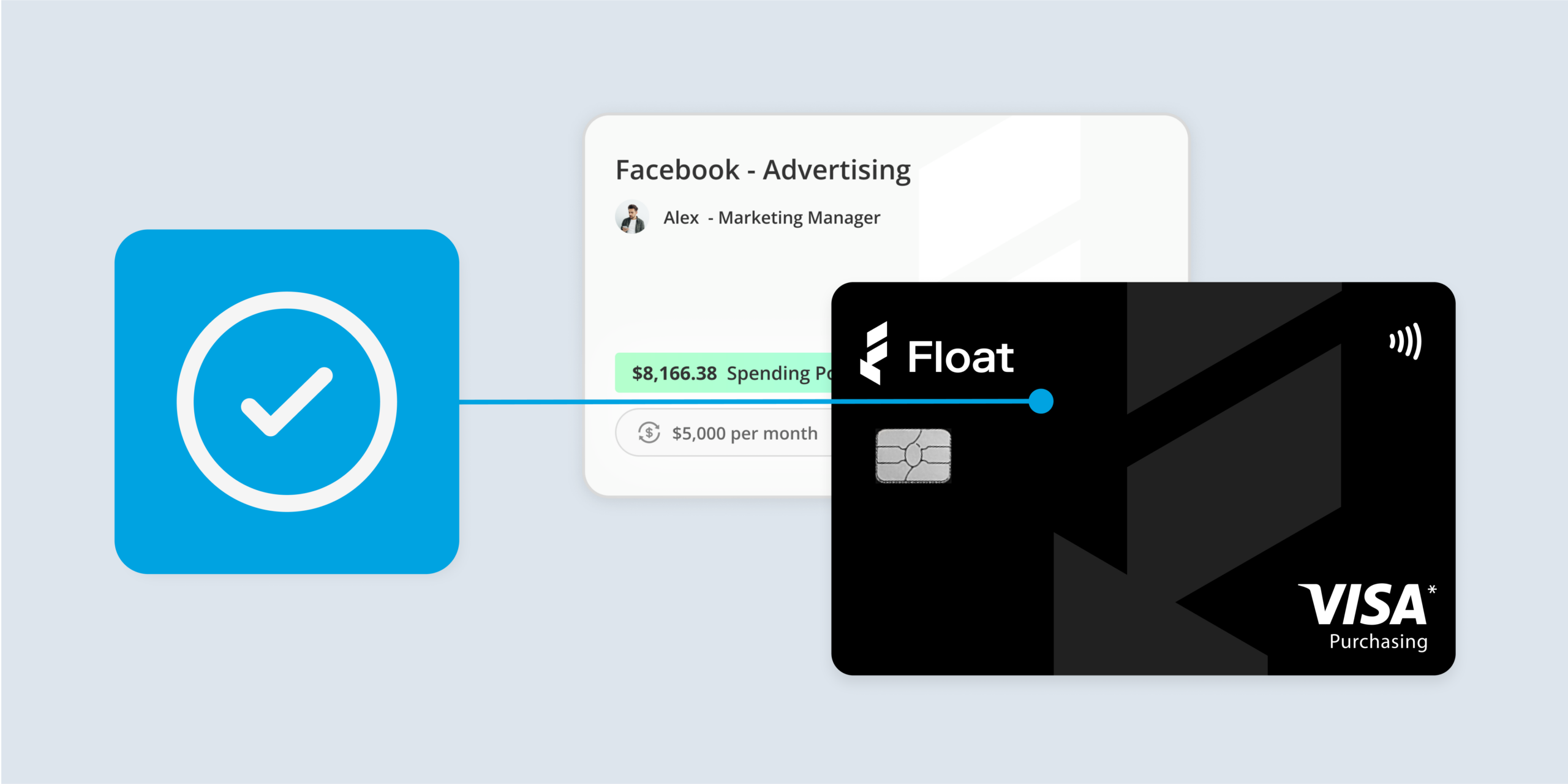

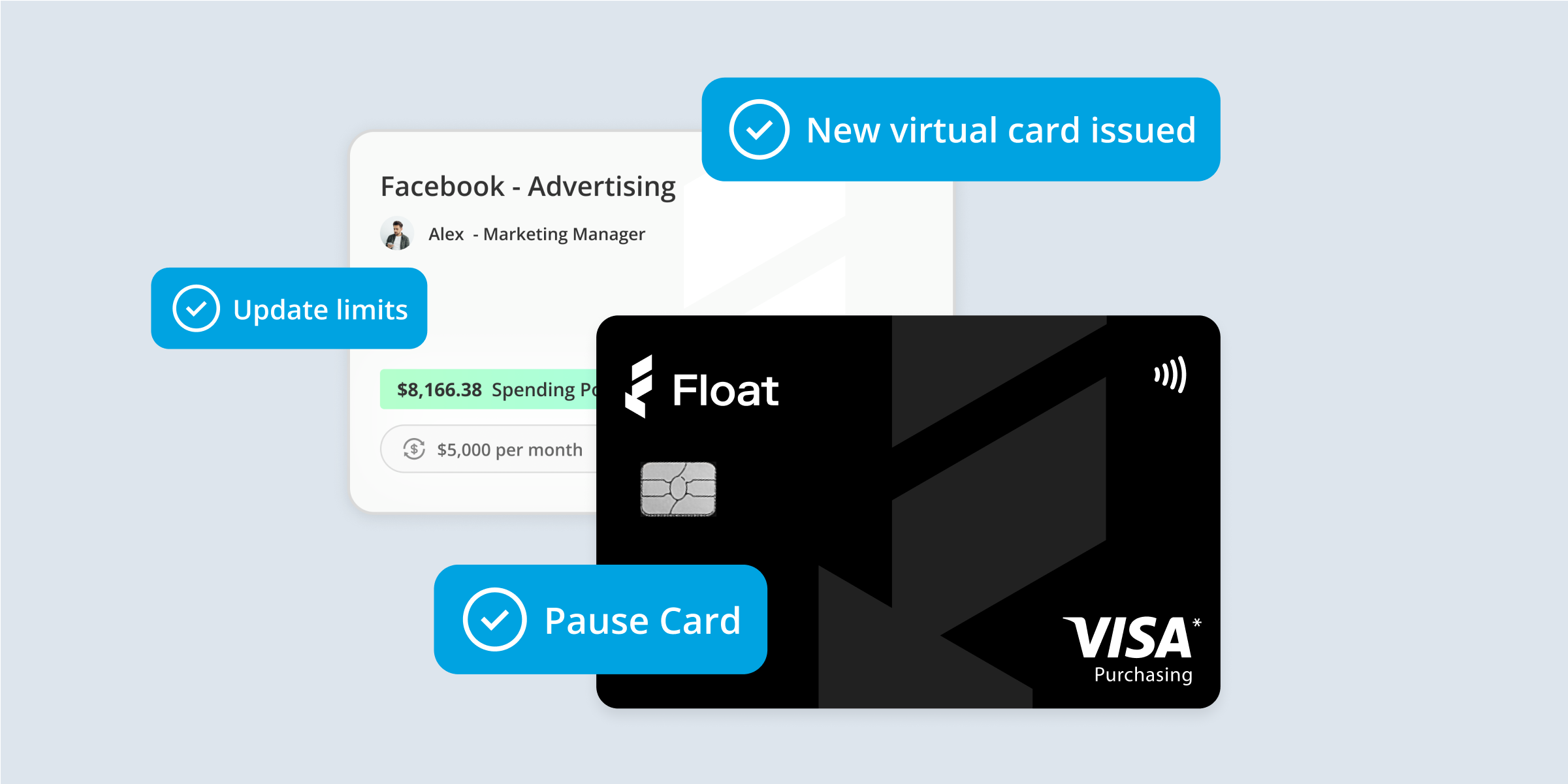

- Business card eligibility: Traditional no-fee credit cards require strong credit, personal guarantees and multi-step applications. Modern solutions like Float are your best option if you want startup business credit cards with no credit checks. Just connect your business bank account, verify your company and issue physical or virtual cards—often on the same-day.

- Real-time spend tracking: For those with lean budgets, seeing exactly how much your business is spending, when and where is key to staying on track. For some business cards, you have to wait 24 hours to see your transactions.

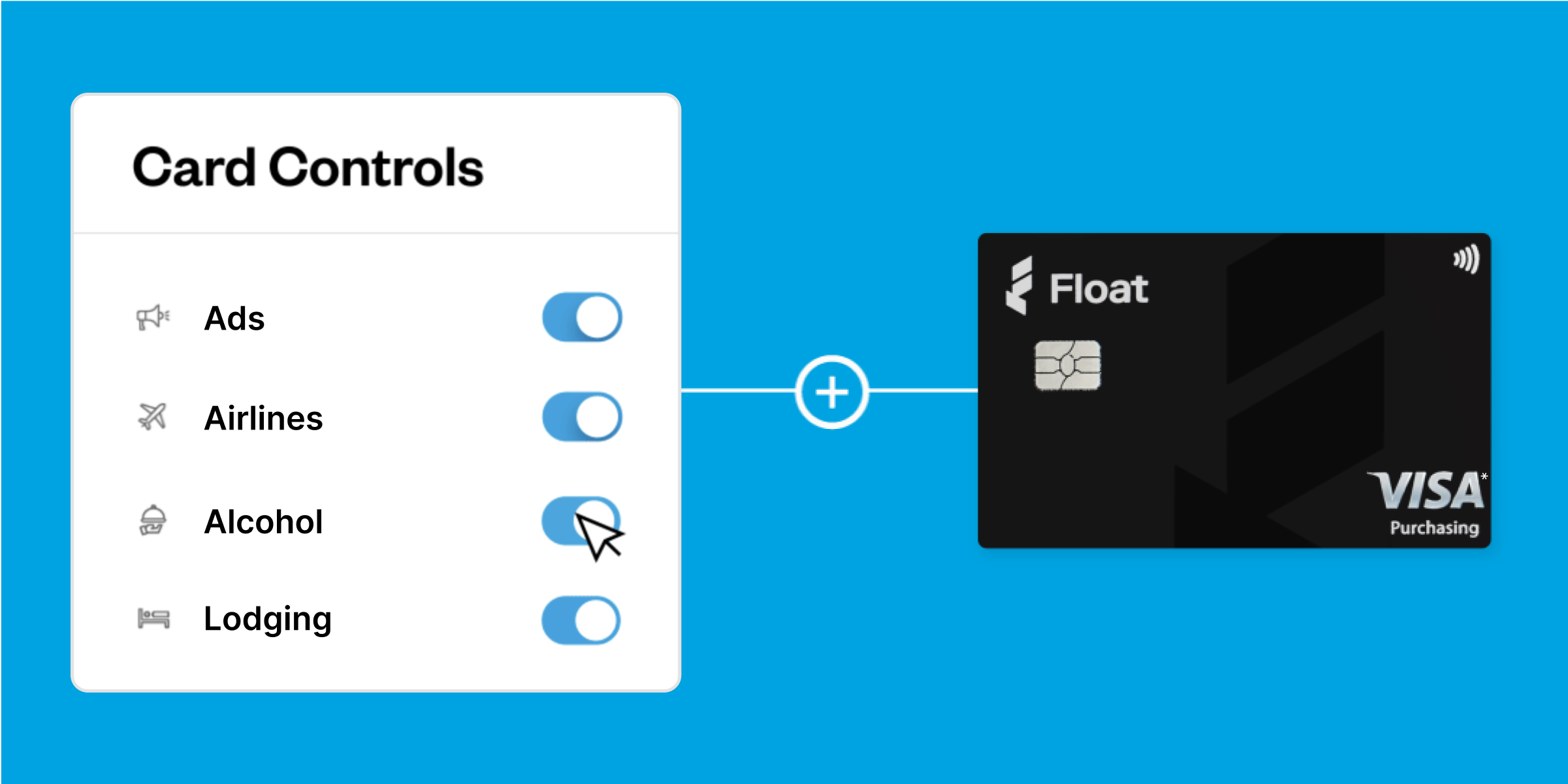

- Virtual and physical card options: Everyone offers physical business cards, but only some no-fee card providers, like Float, offer virtual options. A virtual card is ideal for recurring subscription payments, one-off employee expenses and digital purchases. Virtual cards can also be added to Apple and Android Wallets, adding convenience.

- Custom spending limits and approval flows: Your spending limits should be able to scale as your team evolves. With Float, you can easily customize spending limits and set unique approval flows to manage business spending better.

- Integrations with accounting software: Expense management can’t possibly get any more frustrating. With seamless integrations to your accounting software like QuickBooks, Xero and NetSuite, you can save hours when closing the books at month end.

- Automated receipt capture: Speaking of faster close cycles, Float offers automated receipt capture, enabling your team to manage expenses quickly and without headaches.

Float vs. traditional no-fee business credit cards

Looking for a business credit card with no annual fee and no foreign transaction fee? You’ll find it (and so much more) with Float. While the features a card offers are important, it’s also wise to consider how easy it is to use—and how easy the card provider makes expense management and month-end. Float is more than a cost-effective card; it’s a tool that helps you manage your company’s spending without overpaying or losing control.

Take a look at this comparison between Float and traditional no-fee business credit cards.

| Annual fees | Real-time visibility and control | Accounting-ready data | Approval workflows | Key rewards | |

| Float Corporate Card | $0 | Real-time visibility and extensive customized controls | Automatically available accounting-ready data | Built-in and highly customizable approval workflows | 1.5%* cashback |

| BMO CashBack Business Mastercard | $0 | Real-time visibility | Available through manual download | N/A | 0.75-1.75% cashback |

| TD Business Cash Back Visa* Card | $0 | Real-time visibility and some controls | Available through TD Card Management Tool | N/A | 0.5%-2% in Cash Back Dollars |

| BMO® AIR MILES® Business Mastercard® | $0 for first year; $120 for subsequent years | Real-time visibility | Available through manual integration with accounting tools | N/A | Earn 1 Mile for every $12 you spend |

| RBC Visa CreditLine for Small Business | $0 | Real-time visibility | Available through manual download to accounting tools | N/A | Easy access to credit and earn 1 Avion Rewards point for every $2 spent in net purchases |

| TD Business Select RateTM Visa* Card | $0 (Option to pay annual fee to lower interest rate) | Real-time visibility and some controls | Available through TD Card Management Tool | N/A | Hundreds of cashback offers 21-day interest-free grace period |

Consider Float for your no-annual-fee business card

No annual fee business cards are a smart move for lean Canadian startups, scaling small-to-medium businesses and strategic finance teams. While traditional options help you avoid recurring annual fees, modern platforms like Float take things a step further to launch your success.

With Float’s corporate card, you can not only save money but also streamline expense management, gain real-time visibility and control, and still get cash back rewards. That’s a significant step up from the outdated, legacy cards your business is used to.

Learn more about Float’s corporate cards and make your money count.

Try Float for free

Business finance tools and software made

by Canadians, for Canadian Businesses.