When finance flows, business grows

Business accounts, corporate cards, payments and spend management. Built for Canadian companies.

TRUSTED BY 7,000+ COMPANIES

.avif)

float product suite

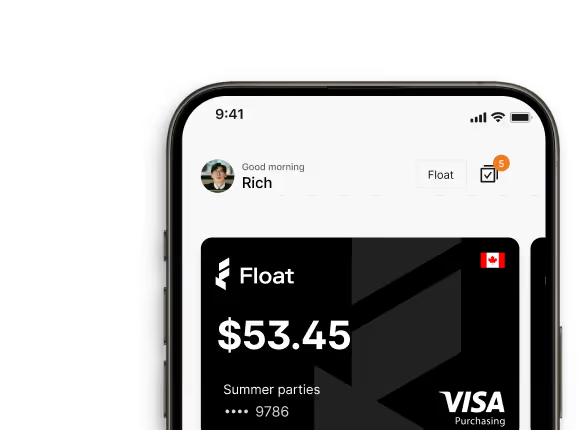

More than a corporate card

Manage all your financial operations in one place and help your business spend smart, save more and grow faster.

DISCOVER FLOAT

See Float in action

Hold, spend and optimize your business’s cash flow and operations, all in one place. Here's how it works.

Float takes the friction out

Everything your business needs to move faster and spend smarter.

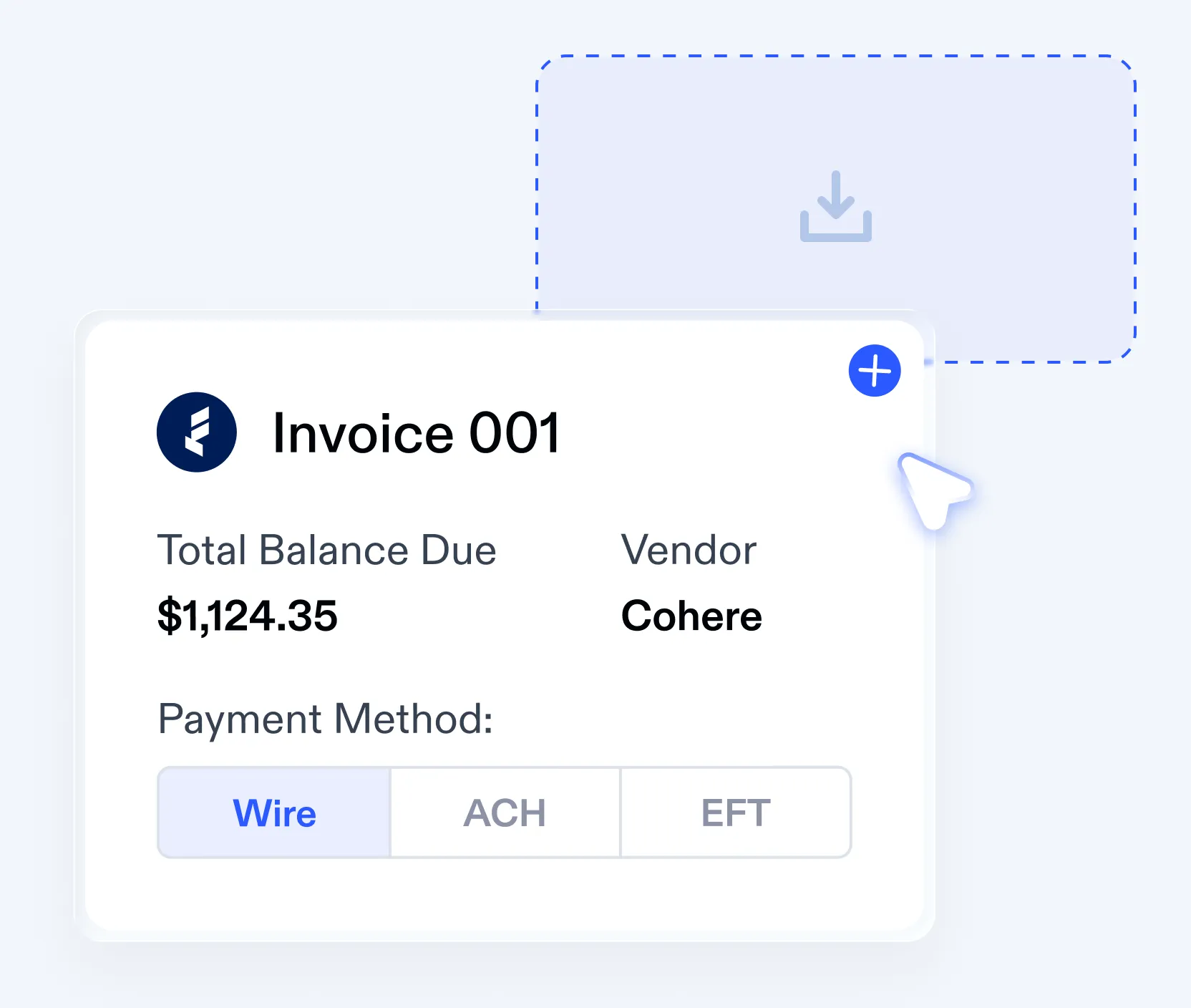

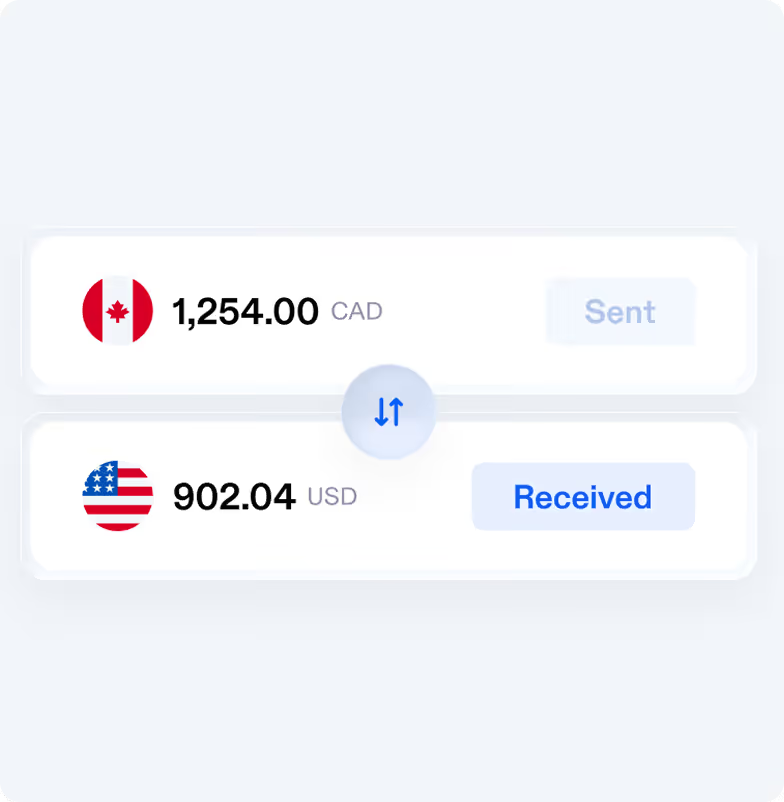

Move money instantly

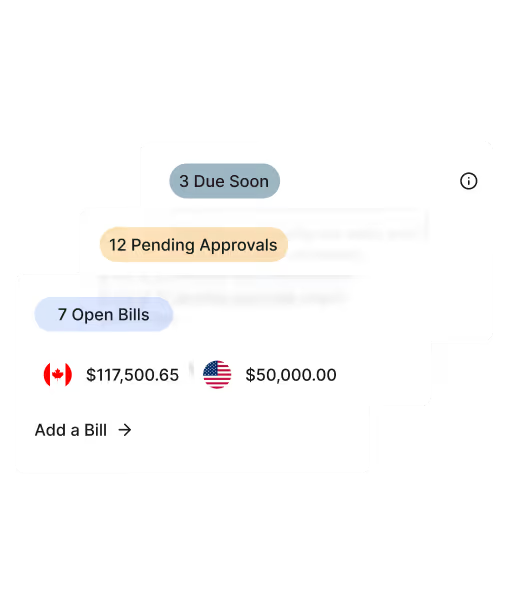

Fund your account and start spending right away. Convert between CAD and USD. Pay bills and vendors directly from Float.

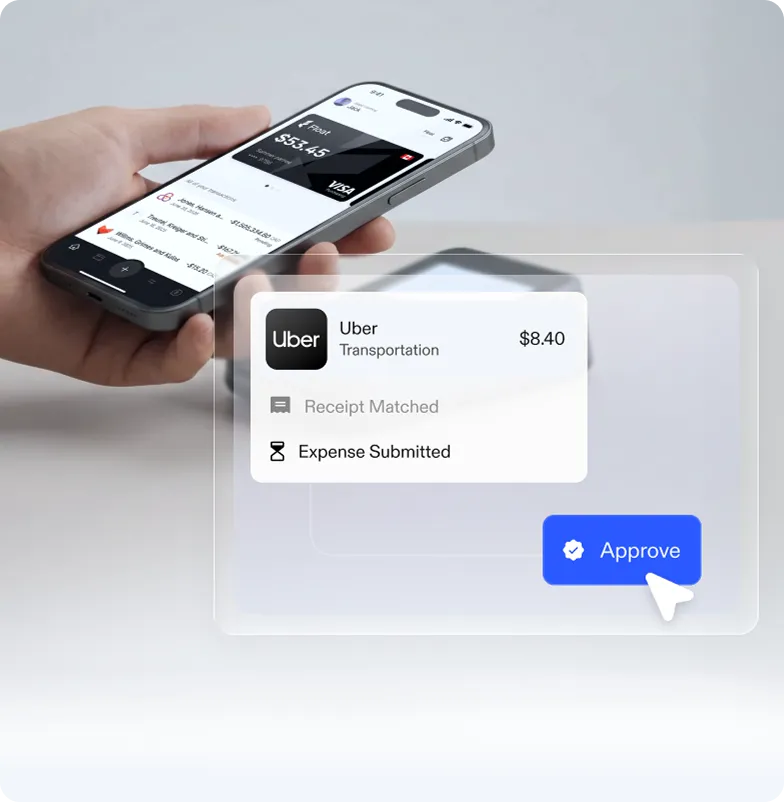

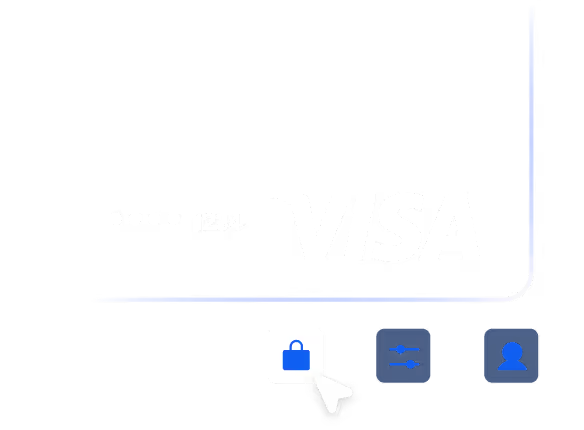

Issue cards with built-in controls

Access interest-free, unsecured credit with Float Charge or pre-fund cards directly from your Float balance. Create unlimited physical or virtual cards in seconds. Set rules and approval workflows before spend happens.

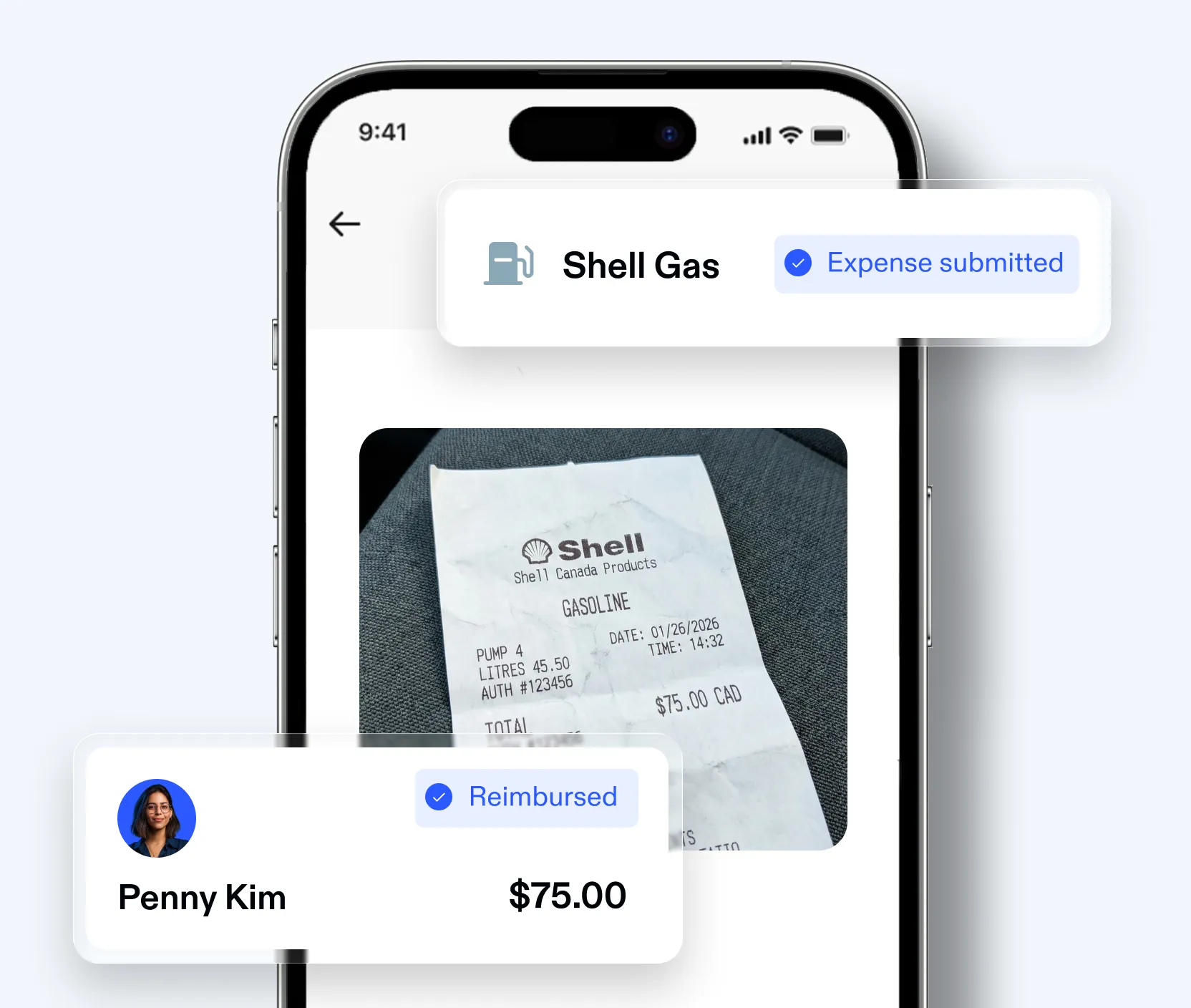

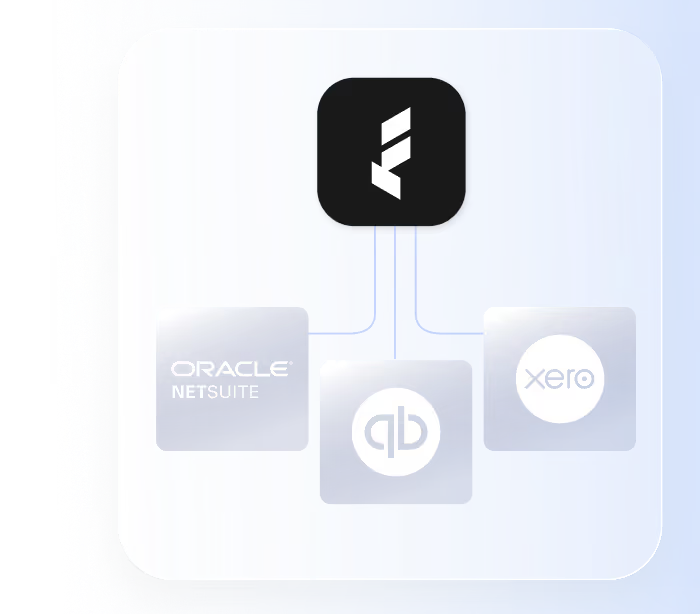

AI-powered software to close books up to 8x faster

No more chasing employees. Get automatic receipt reminders and Canadian-trained AI coding for transactions. Plus, export transactions directly to QBO, Xero or NetSuite.

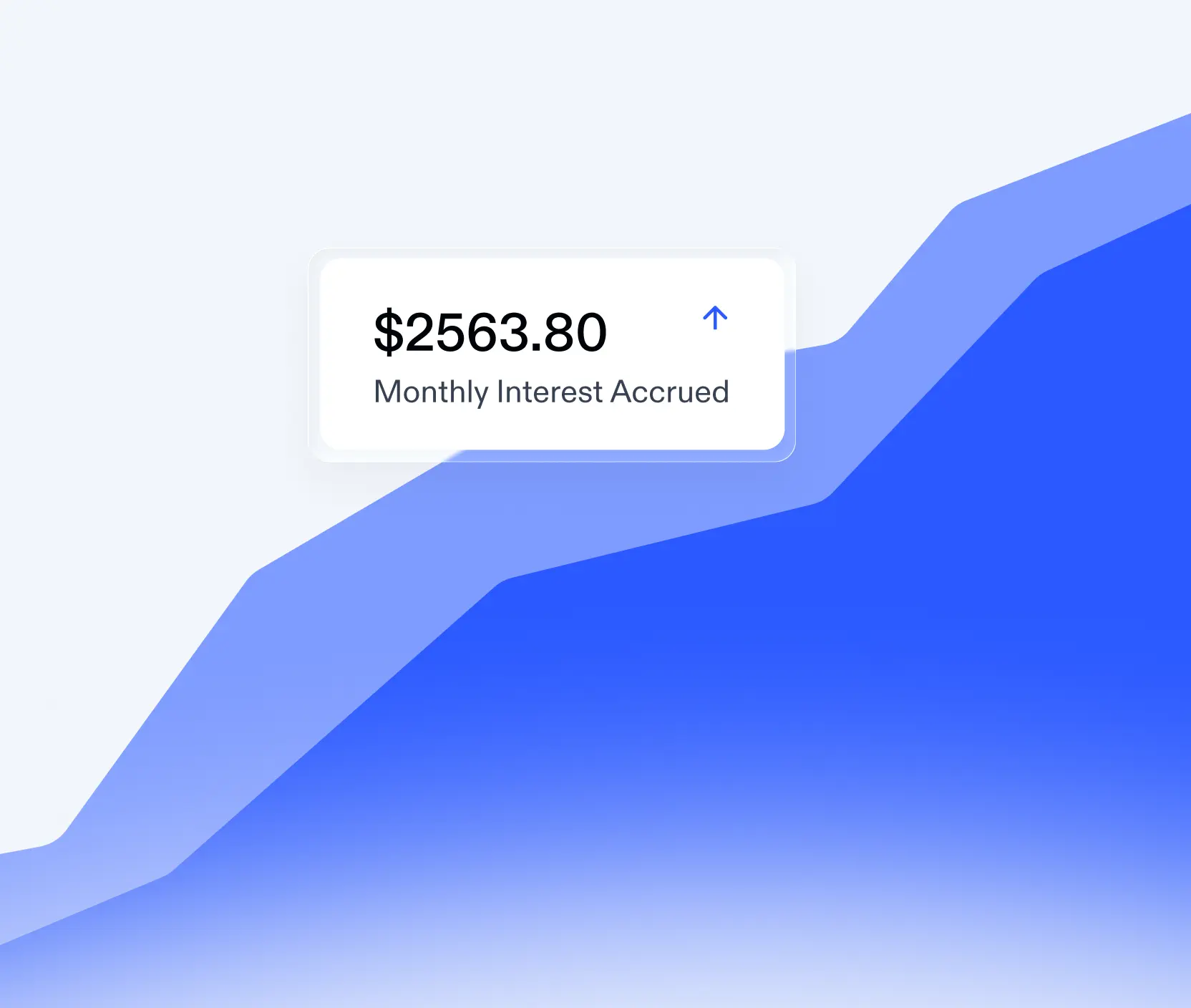

Earn more on every dollar

Get up to 1% cashback on every purchase. Earn up to 3.5% interest on your balance. Watch your money work harder, while keeping it within reach.

*Rates are variable and subject to change. Terms, eligibility criteria and caps apply.

Built for the way Canadians do business.

Most finance platforms were built for the US. That means manual workarounds for Canadian taxes, currencies and regulations. More time. More headaches.

Purpose-built right here, Float gives you world-class tools designed exactly for the way you operate. That means high-interest on CAD and USD, fast bill payments and AI features that actually understand Canadian transactions. No retrofitting required.

All built in, not bolted on.

How to Float in 30 days

- Load funds and start earning up to 3.5% interest

- Issue virtual cards for your team in minutes

- Set controls so spending starts clean from day one

- Pay bills on autopilot and centralize spend in one platform

- Convert CAD to USD at market-leading rates

- Collect receipts instantly, without chasing

- Export transactions seamlessly to your accounting software

- Close your books 8x faster

- Save up to 7% across total spend

Hear it right from our customers

Join thousands of Canada’s leading companies already on Float.

Float by the numbers

A look at the platform thousands of Canadian teams trust to power their financial operations.

Fast, flexible and fully protected

Modern finance tools built on a foundation you can trust. Get everything your business needs in one place.

Same-day card issuance

No personal guarantee. No physical paperwork. No branch visit.

CDIC insurance

Funds safeguarded in trust accounts, with CDIC coverage on eligible deposits.

Free Essentials plan

The $0 solution for spend control and payments

Direct integrations with QuickBooks, Netsuite, Xero and more

Accounting, HR, productivity and a custom API for seamless workflow

Zero liability fraud protection

Plus added prevention software to detect fraud patterns and send alerts

World-class support

Fast, friendly and completely Canadian-based

Mobile app

Capture receipts, request reimbursements and manage spend on the go

Financial solutions for every stage of growth

Whether you’re handling the books for a small business or leading an in-house finance team, Float’s got you covered with the tools you need to manage operations faster and easier.

Start-ups

Get up and running fast with corporate cards, automated expenses and built-in controls to help you automate bookkeeping as you scale.

Small businesses

Keep spending organized and cash flow visible with smart cards, bill pay and reimbursements. And get it all in the platform built for Canadian businesses.

Mid-sized companies

Expand with confidence using advanced approvals, multi-entity visibility, dual-currency cards and direct accounting integrations for control and speed.

Elevate your financial operations

Join 7,000+ Canadian businesses using Float