Cash Flow Optimization

How to Make Cross-Border ACH Payments: Complete 2026 Guide for Canadian Businesses

A practical guide for Canadian finance teams paying US vendors. Learn how cross-border payments work, where ACH fits, what can go wrong and how to do it faster, cheaper and with fewer surprises.

May 20, 2026

Paying US vendors or employees as a Canadian business can be more complicated than it should be. With unfamiliar payment terms, unclear timelines, FX surprises and opaque bank processes, even experienced finance teams may hesitate to send cross-border payments.

This guide is designed to change that. We’ll walk through how Canadian businesses pay US recipients via ACH, what happens behind the scenes when money moves across the border and how to avoid the most common delays, errors and cost pitfalls. You’ll learn when ACH makes sense, how long payments really take, what information you need upfront and what to watch for as volumes grow.

What is an ACH payment?

An ACH (Automated Clearing House) payment is an electronic bank-to-bank transfer that runs on the US payment network and is regulated by the US Federal Reserve. It’s the standard way money moves digitally between US bank accounts, similar in structure to how EFT works in Canada. ACH payments are processed in batches, follow predictable settlement windows and are commonly used for vendor payments, payroll and recurring transactions within the US

When should Canadian businesses use ACH?

Canadian businesses typically use ACH to pay US-based vendors, contractors or employees. ACH is not used for domestic Canadian payments—those processed through Canadian EFT rails—but it becomes essential when money needs to move into a US bank account. For cross-border payments, ACH is often faster and significantly more cost-effective than wire transfers, making it the preferred method for Canadian companies operating or scaling in the US

ACH payment setup for Canadian businesses

Before sending your first ACH payment, Canadian businesses need to make sure a few foundational pieces are in place. These steps help ensure cross-border payments move smoothly and are recorded correctly from day one.

Step 1: Confirm you can send ACH payments to US bank accounts

Not all Canadian banks or platforms support ACH payments by default. Start by confirming that your provider allows Canadian businesses to send payments to US bank accounts using ACH. This typically requires additional cross-border payment permissions and, in some cases, a connected or supported US dollar account.

Step 2: Complete cross-border onboarding and verification

Most providers require extra setup for ACH payments, including business verification and compliance checks specific to cross-border transactions. This is a one-time process, but it can take time, so it’s best to complete onboarding before ACH becomes business-critical.

Step 3: Collect the right recipient banking information

ACH payments rely on precise banking details. You’ll need the recipient’s US routing number, account number, legal name and account type (checking or savings). Even small errors can cause delays or failed payments, so accuracy is essential.

Step 4: Align your accounting and FX configuration

Once you start paying US vendors or employees, your accounting system needs to correctly recognize USD transactions. This includes proper currency settings, FX treatment and reconciliation workflows. Misconfigured systems can mistakenly treat USD payments as CAD or apply incorrect exchange rates, creating reporting headaches later.

How to make a cross-border ACH payment (quick checklist)

Once your ACH setup is complete, sending a cross-border payment to a US vendor or employee is straightforward. Most payments follow the same basic flow:

- Log in to your bank or payment platform that supports ACH for Canadian businesses

- Select ACH as the payment method and enter the payment amount in USD

- Add or select the US recipient, including their routing number, account number and legal name

- Choose the payment date, keeping processing timelines in mind

- Review and approve the payment using your organization’s security or approval process

- Monitor the payment status until it settles in the recipient’s US bank account

ACH payments typically settle within 1 to 3 business days, depending on cut-off times and your payment provider. Scheduling payments in advance helps avoid delays and ensures vendors are paid on time.

Common ACH payment challenges (and how to avoid them)

ACH payments are a reliable way to pay US vendors, but most issues don’t come from the payment rail itself. They come from setup, timing and visibility gaps. Here are the most common challenges Canadian businesses run into, and how to stay ahead of them.

1. Delays caused by cut-off times

ACH payments are processed in batches, and missing the daily cutoff can delay settlement by a full business day or more. Scheduling payments in advance and understanding your provider’s cut-off times helps avoid last-minute surprises.

2. Incorrect or incomplete banking details

ACH payments rely on precise routing and account information. Even small errors—like an incorrect routing number or account type—can cause payments to fail or be returned. Verifying recipient details upfront is one of the easiest ways to prevent delays.

3. Unexpected FX costs or currency confusion

Cross-border payments introduce foreign exchange considerations. If your systems aren’t configured correctly, USD payments may be misclassified as CAD, or FX conversions may be applied inconsistently. Clear currency handling and transparent FX rates are important as your company’s payment volume grows.

4. Limited visibility into payment status

Many traditional bank workflows offer little insight into where an ACH payment is once it’s been sent. Without real-time status updates or clear confirmation, finance teams are often left to manually respond to vendor follow-ups. Using an intelligent bill pay platform that provides clear tracking, confirmation and centralized payment history helps reduce uncertainty and support faster issue resolution.

5. Payment limits and compliance holds

Some providers impose per-payment caps or flag larger ACH transactions for additional review, which can slow down time-sensitive payments. Understanding these limits in advance helps avoid unexpected interruptions.

ACH payments vs. wire transfers: cost and speed comparison

When paying US vendors, Canadian businesses typically choose between ACH payments and wire transfers. Both move money across the border, but they behave very differently in practice.

Cost

ACH payments are generally far more cost-effective. They come with low, predictable fees and favourable FX treatment, making them well-suited for recurring or operational payments. Wire transfers often involve higher bank fees, intermediary charges and less transparent FX costs—especially for frequent or lower-value payments.

Speed and predictability

ACH payments usually settle within 1 to 3 business days, with consistent timelines once cut-off times are understood. Some providers can process ACH payments the same day if submitted early enough. Wire transfers can be faster in theory, but in reality they’re often subject to manual processing, bank holds and intermediary delays that make timing less predictable.

Operational effort

ACH payments are designed for repeatability. Once recipient details are set up, payments can be scheduled and tracked with minimal manual work. Wire transfers tend to require more hands-on effort, re-entry of details and follow-up, particularly when issues arise.

When wire transfers still make sense

Wire transfers can be appropriate for large, one-off, time-sensitive payments where immediacy matters more than cost. But for most ongoing cross-border payments, ACH offers a better balance of efficiency, visibility and control.

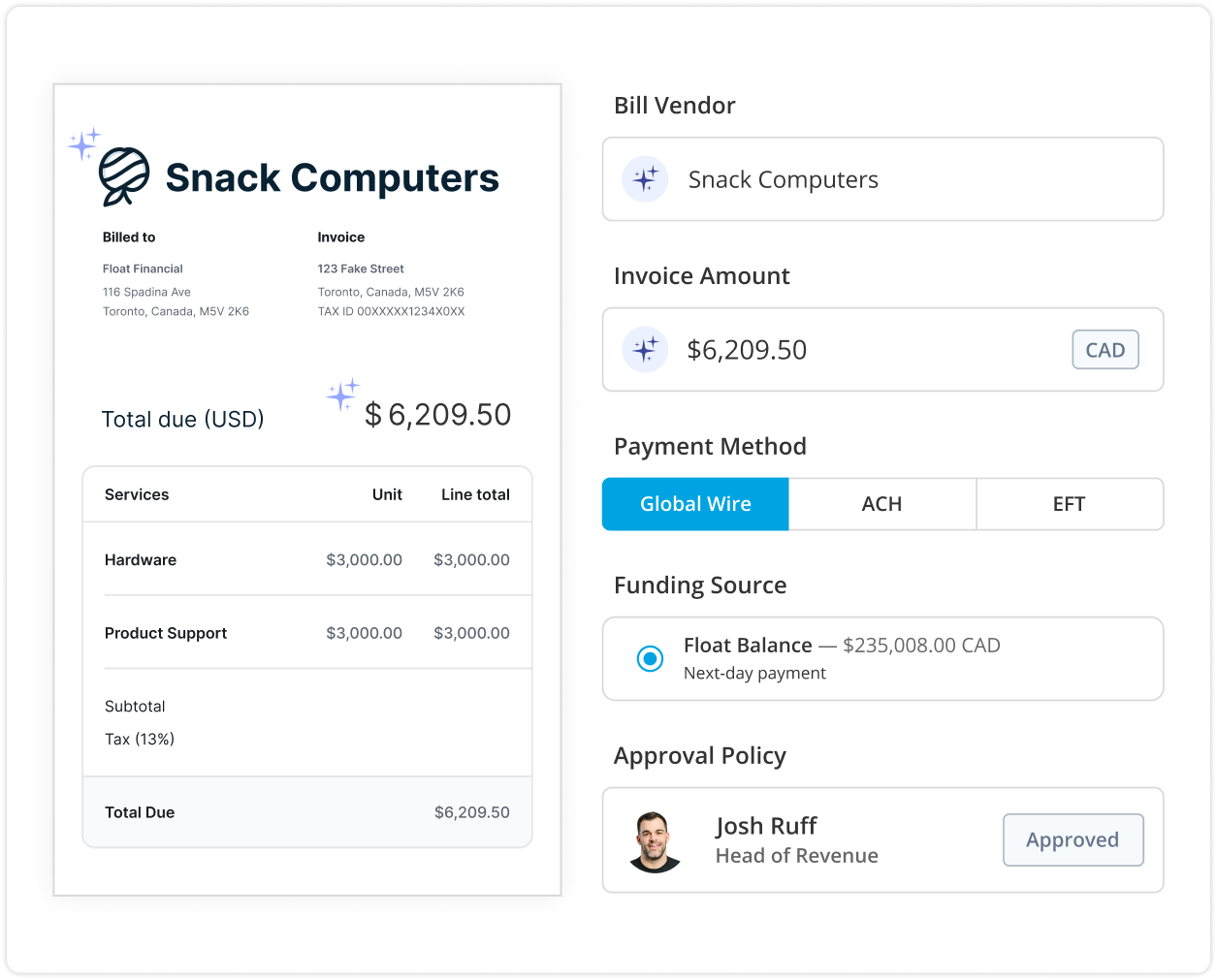

How Float simplifies cross-border ACH payments

ACH is one of the most cost-effective ways for Canadian businesses to pay US vendors, but how you access ACH matters just as much as the payment rail itself. Traditional banks often add friction, hidden FX costs and delays that quietly erase ACH’s advantages.

Float is designed to make cross-border ACH work the way finance teams expect it to: fast, predictable and cost-efficient, without forcing you to manage multiple banks, currencies or workflows. Here’s how.

Lower FX costs by paying from the right account

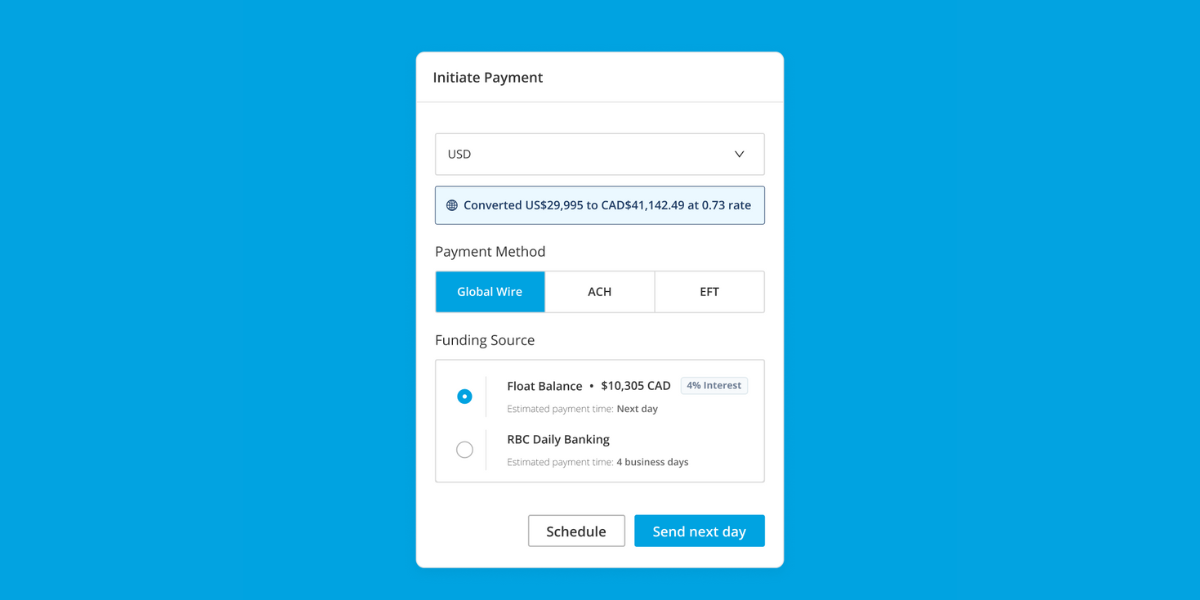

Many businesses run into trouble when paying USD invoices directly from CAD bank accounts. In those cases, banks often apply FX markups of 2-4% and route payments via wire rather than ACH. With Float, businesses can hold and pay in USD, access transparent FX rates starting at 0.25% and avoid unnecessary wire fees.

Faster, more predictable ACH delivery

Float supports ACH payments that can settle as quickly as same-day, when cutoff times and network conditions are met. This is significantly faster than many traditional banks, which often take 2 to 3 business days for ACH payments. More importantly, timelines are consistent and visible, so finance teams don’t need to pad payment dates “just in case.”

Automatic payment routing with built-in optionality

Instead of forcing teams to think about payment rails, Float automatically selects the appropriate method based on currency:

- CAD bills are paid via EFT

- USD bills are paid via ACH

- Wire transfers remain available by manual selection when they’re genuinely required

This automation reduces errors while still giving finance teams control when exceptions arise.

Fewer limits, fewer interruptions

Some payment providers impose strict per-payment ACH caps or trigger frequent compliance reviews for mid-sized payments, causing delays at the worst possible time. Float is built to support growing payment volumes while minimizing unnecessary reviews and interruptions common with traditional bank workflows.

Centralized visibility, approvals, and tracking

All ACH payments flow through a single approval and tracking system. Finance teams can see when payments are scheduled, sent and settled, reducing vendor follow-ups, internal guesswork and manual reconciliation.

Paying US vendors with ACH via Float vs. a traditional bank

For Canadian businesses, the biggest cost and complexity issues in cross-border payments usually come from currency conversion, not the ACH payment itself. When USD invoices are paid from CAD bank accounts, traditional banks often apply FX markups and may route payments via wire rather than ACH. Using ACH effectively depends on paying from the right account and having the right routing in place.

| Traditional bank setup | Float | |

| USD account requirement | Often requires setting up and managing a separate USD or US-based account to reliably use ACH | Includes built-in USD holding and payment capabilities, removing the need to set up and manage a separate bank relationship solely for ACH |

| Ensuring ACH is used | Requires manual configuration and confirmation to avoid wire routing | ACH is automatically selected for US payments |

| Risk of defaulting to wires | Higher if paying from CAD accounts or misconfigured USD workflows | Low—ACH routing is built directly into the workflow |

| FX handling | FX markups of 2-4% are common when CAD is converted to USD | FX conversion as low as 0.25%, with no separate ACH transaction fee |

| Payment speed | Can be 2-3+ business days, varies by bank and setup | Same day or next business day when cut-offs are met |

| Operational effort | High with multiple portals, checks, and follow-ups | Low with a single, centralized workflow |

| Visibility and control | Limited and fragmented | Centralized tracking and approvals |

| Optionality | Wires often become the default | ACH by default, with wires available when needed |

Actual requirements, FX rates and timelines vary by provider and account configuration. This reflects common experiences for Canadian businesses paying US vendors.

ACH payment compliance for Canadian businesses in 2026

ACH payments are a standard, compliant way for Canadian businesses to pay US vendors and employees. The key is making sure a few cross-border basics are handled correctly:

- Follow US ACH rules: ACH payments run on US payment rails, so transactions must be properly authorized and traceable, just like any other regulated bank transfer.

- Maintain clear payment records: Keep confirmation details, recipient information and payment amounts for reconciliation, audits and tax reporting.

- Handle currency correctly: Ensure USD payments are clearly recorded as USD and FX rates are applied consistently to avoid reporting or reconciliation issues.

- Use built-in controls and approvals: Platforms with approval workflows, audit trails and centralized visibility help reduce compliance risk without slowing payments down.

For most Canadian businesses, ACH compliance isn’t complicated if you have the right setup and visibility as cross-border payments scale.

Float: The best way to manage cross-border payments

Using our bill pay solutions and accounts payable platform, Canadian businesses can streamline their ACH payment processes, reduce errors and ensure timely payments. Our platform offers seamless integration with your existing financial systems, making it easier to manage accounts payable and stay on top of your business finances.

When you’re ready to simplify how you manage ACH payments alongside the rest of your accounts payable, Float is here to help you do it with confidence. Get started for free today.

Frequently asked questions

What are the steps to make an ACH payment as a Canadian business?

At a high level, Canadian businesses need to ensure they can send ACH payments to US bank accounts, collect accurate recipient banking details, initiate the payment in USD and track settlement. The most important step is proper setup, so that payments are routed via ACH rather than defaulting to a wire.

Is ACH used for domestic payments in Canada?

No. ACH is a US payment system used to send funds between US bank accounts. Canadian businesses use ACH primarily for cross-border payments to US vendors or employees. Domestic Canadian payments are processed through EFT systems instead.

Are there compliance considerations for Canadian businesses using ACH?

Yes, but they’re straightforward. While ACH payments follow US payment rules, Canadian businesses must ensure payments are properly authorized, recorded and reported for accounting and tax purposes. Clear documentation, correct currency handling and approval controls are the main compliance considerations.

Do Canadian businesses need a US bank account to use ACH?

Often, yes—when using traditional banks, businesses typically need to set up and manage a separate USD or US-based account to reliably access ACH and avoid unnecessary FX costs. Modern platforms like Float include USD accounts, making it easier to pay US vendors via ACH without additional bank setup.

How does Float help reduce the cost and complexity of ACH payments?

Float simplifies cross-border ACH by automatically routing USD payments via ACH, offering transparent FX rates as low as 0.25% and centralizing approvals, tracking and reporting in one workflow. This helps finance teams avoid wire fees, reduce FX surprises and pay US vendors with greater speed and predictability.

Written by

All the resources

Cash Flow Optimization

How to Make EFT Payments in Canada: Complete 2026 Guide

Learn how to make an EFT payment in Canada, avoid extra fees and move money faster in 2026 with modern

Read More

Expense Management

Expense Management System Implementation Guide for Canadian Businesses

Are manual expense processes getting you down? It might be time for an expense management system.

Read More

Corporate Cards

Procurement Cards vs. Corporate Cards: Which is Right for Your Business?

Let's break down how procurement cards and corporate cards work, where each one shines and how Float offers the flexibility

Read MoreSpend time and money

where it counts

Earn up to 3.5% interest on your cash balance and simplify business spending with corporate cards, accounts payable and expense management software.